UK is only country in G7 where household budgets have not recovered to pre-pandemic levels

Families would be £750 a year better off if real disposable income had grown in line with other leading economies

Working people are being made poorer by Conservative failure, union body says

The UK is suffering the worst decline in living standards of any G7 country – according to new TUC analysis published this week.

The analysis shows the UK is only G7 economy where real household disposable income per head hasn’t recovered to its pre-pandemic levels:

Real household disposable incomes in the UK were 1.2% lower in the second quarter of 2023 than at the end of 2019.

But over the same period they grew by 3.5%, on average, across the G7.

The TUC estimates that if real disposable income in the UK had risen in line with the G7 average UK families would be £750 a year better off.

More pain ahead

The union body warned that the contraction in UK household budgets is going to get worse – despite falling inflation.

The Office for Budget Responsibility (OBR) forecasts that real house disposable income per head in Britain will fall by an additional 3.4% by the end of the first quarter of 2024.

And according to the same forecasts household budgets won’t even recover to their pre-pandemic levels until the end of 2026.

The OBR said in November that UK households are suffering the worst period for living standards since modern records began in the 1950s.

Households in debt

The TUC says the Conservatives’ failure to grow the economy and deliver healthy wage growth has pushed many households further into debt.

Analysis published by the union body at the end of December revealed that unsecured debt (credit cards, loans, hire purchase agreements) is set to rise by £1,400 per household, in real terms, this year.

The TUC says working people have been left brutally exposed to rising costs after years of pay stagnation.

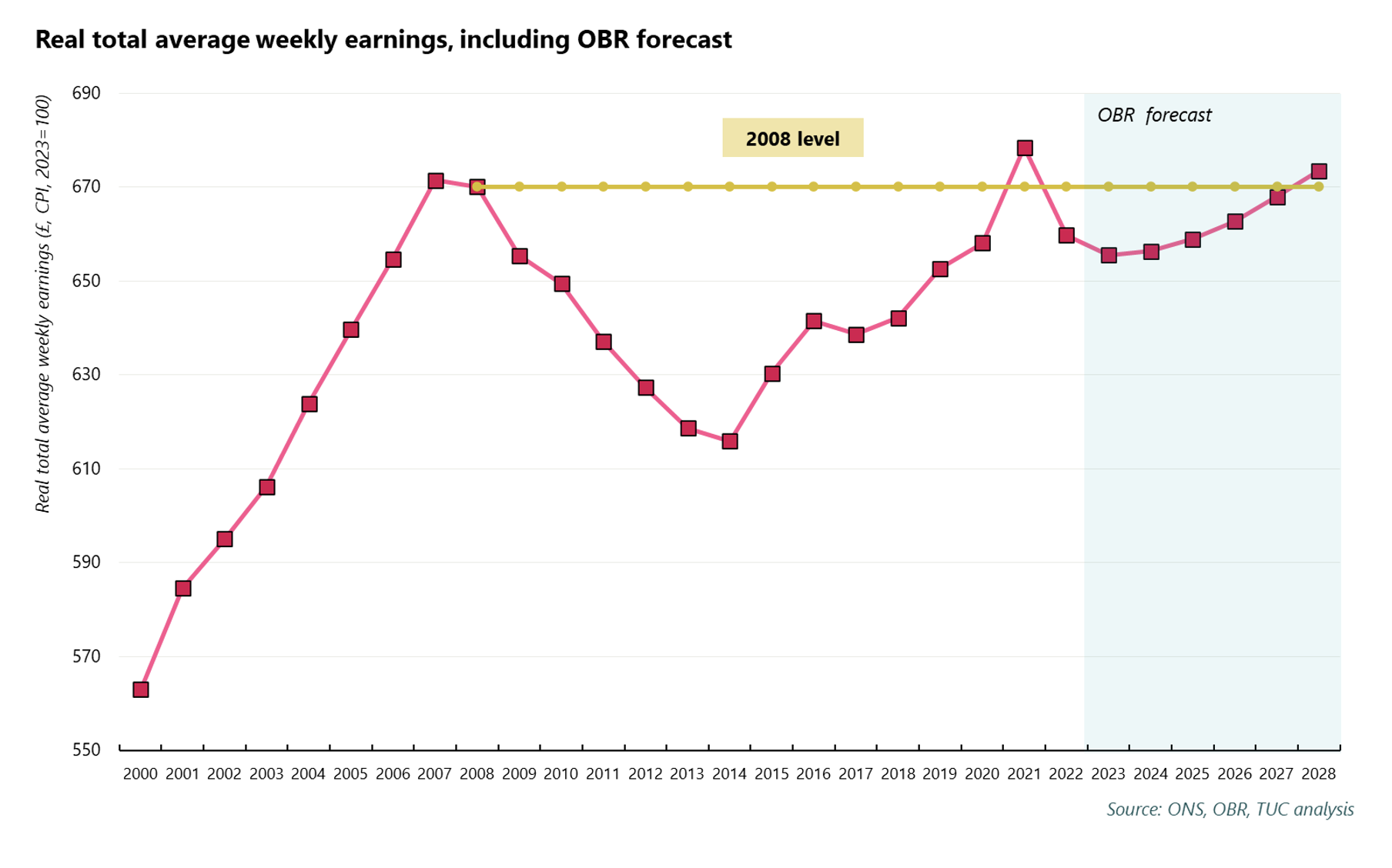

UK workers are on course for two decades of lost living standards with real wages not forecast to recover to their 2008 level until 2028.

The TUC estimates that the average worker has lost £14,800 since 2008 as a result of their pay not keeping up with pre-global financial crisis real wage trends.

TUC General Secretary Paul Nowak said: “The UK is the only G7 nation where living standards are worse than before the pandemic.

“While families in other countries have seen their incomes recover – household budgets here continue to shrink.

“This is a damning indictment on the Conservatives’ economic record.

“Their failure to deliver decent growth and living standards over the last 13 years has left millions exposed to skyrocketing bills – and is pushing many deeper into debt.

“We can’t go on like this. Britain cannot afford the Tories for a day longer.”

Growth in real disposable household income in the G7

Country

change 2019Q4 to 2023Q2

United Kingdom

-1.2

Italy

0.1

Germany

0.2

Japan *

0.5

France

2.4

Canada

3.0

G7

3.5

United States

6.0

source: OECD; * Japan to 2022Q1

– The analysis is based on OECD figures for real household disposable income per head, which extend to 2023Q2 (except for Japan, which go to 2022Q1). Looking forward, UK figures are based on Office for Budget Responsibility projections in the November 2023 Economic and Fiscal Outlook. As with the ONS outturns and OBR projections, cash figures are in 2019 prices.

– The OBR measure living standards as real household disposable income (RDHI) per person.

The proposals in the UK Government’s Back to Work Plan contain a confusing mixture of devolved and reserved responsibilities, which leave us slightly mystified as to exactly how this is all going to work in practice (writes Fraser of Allander Institute’s MAIRI SPOWAGE):

In his speech, the Chancellor said: “… last week I announced our Back to Work Plan. We will reform the Fit Note process so that treatment rather than time off work becomes the default.

“We will reform the Work Capability Assessment to reflect greater flexibility and availability of home working after the pandemic. And we will spend £1.3 billion over the next five years to help nearly 700,000 people with health conditions find jobs.

“Over 180,000 more people will be helped through the Universal Support Programme and nearly 500,000 more people will be offered treatment for mental health conditions and employment support.

“Over the forecast period, the OBR judge these measures will more than halve the net flow of people who are signed off work with no work search requirements. At the same time, we will provide a further £1.3 billion of funding to offer extra help to the 300,000 people who have been unemployed for over a year without having sickness or a disability.

“But we will ask for something in return. If after 18 months of intensive support jobseekers have not found a job, we will roll out a programme requiring them to take part in a mandatory work placement to increase their skills and improve their employability. And if they choose not to engage with the work search process for six months, we will close their case and stop their benefits.”

These changes have the potential to impact recipients of Universal Credit. The complication is that UC is reserved, while many elements of employment support – the “extra help” that the Chancellor talks about – is, on the whole, devolved.

Because of this, many of the support mechanisms to help people avoid sanctions in England (& Wales in most cases) generated Barnett consequentials, including:

Restart: expand eligibility and extend the scheme for two years

Mandatory Work Placements: phased rollout

Universal Support: increase to 100,000 starts per year

Talking Therapies: expand access and increase provision

Individual Placement and Support (IPS): expand access

Sanctions: closing claims for disengaged claimants & end of scheme review

Fit Note Reform trial

So, in summary, it looks like the sanctions could be applied in a reserved benefit, following support that may or may not be provided by the Scottish devolved employability system as the Scottish Government could choose to spend the money on something else.

We wait for more details from both the UK & Scottish Governments about how this is going to work in practice.

• The real pay crisis is intensified and now expected to last 20 years. • The politically charged National Insurance cut makes the smallest dent in the worse squeeze on household incomes since the 1950s. • While the Chancellor has enjoyed higher revenues, he has chosen to play austerity politics rather than back public services on the brink – £20 billion has been taken from public services to fund the meagre tax cut. • An ‘Autumn Budget for growth’ has meant the reduced growth in almost every year of the forecast. • ‘Full expensing’ of capital expenditure is a seriously inefficient way to boost the economy. • In spite of all the claims to the contrary, the Tories are still presiding over worst deterioration in public finances for more than 100 years.

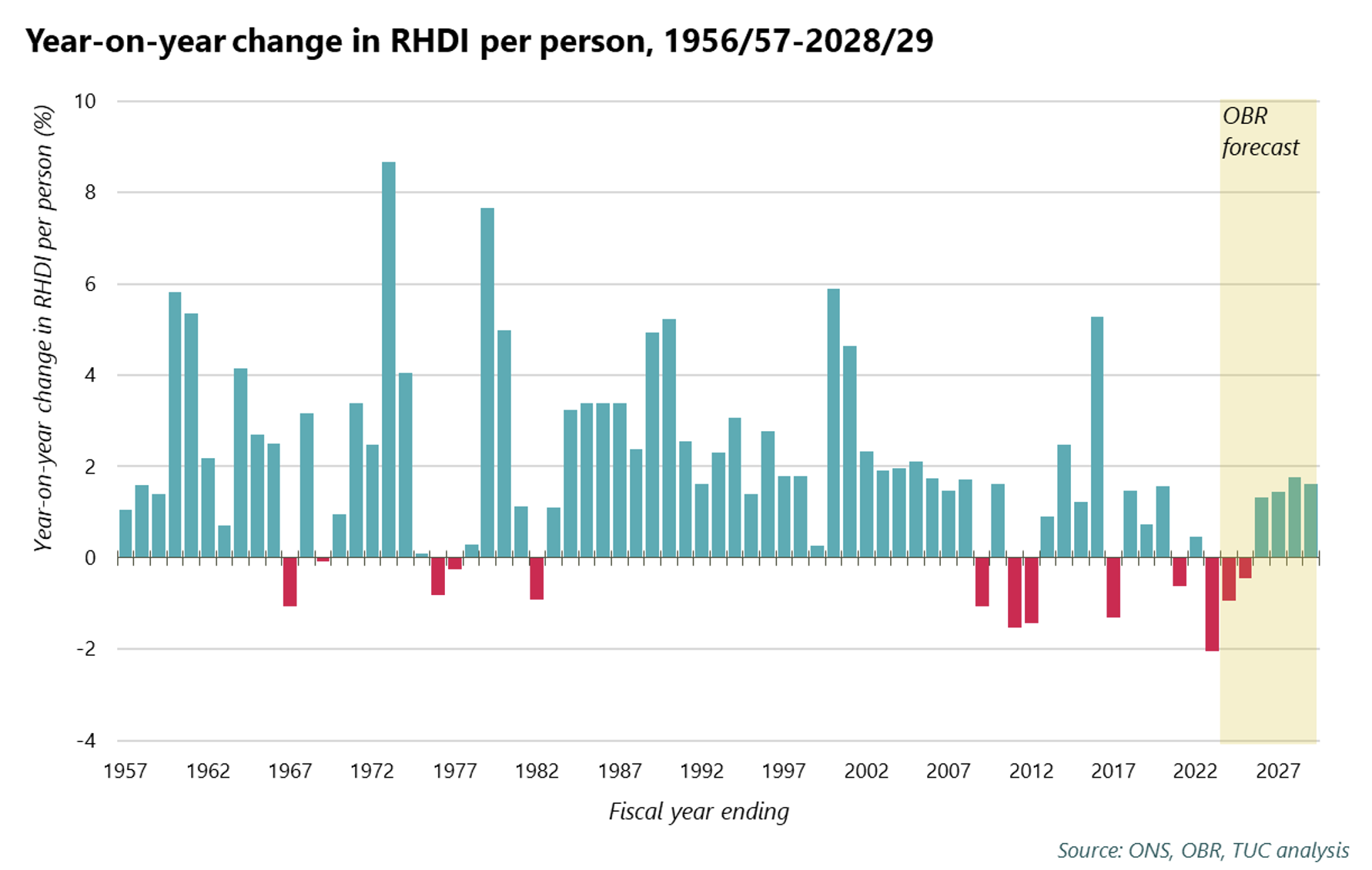

Real wage and household disposable income crisis unended

The forecasts published alongside the statement by the Office for Budget Responsibility (OBR) contained alarming news on real wages. According to the OBR forecasts, real wages are now not set to return to 2008 levels until 2028. The current pay squeeze will hit two decades.

This is a significant downgrade on the March forecast, when wages were returning to 2008 levels by 2026 – two years sooner than it now expects.

The forecast for broader living standards (as measured by real household disposable income per person) remains dire. After already declining in both the 2020/21 and 2022/23 financial years, further falls are expected over the next two.

While in fact a less bad forecast than March, the OBR stress that living standards “are forecast to be 3½ per cent lower in 2024-25 than their pre-pandemic level … this … represents the largest reduction in real living standards since ONS [Office for National Statistics] records began in the 1950s”.

The OBR also put into perspective the 2 per cent cut in National Insurance, reckoning it will boost living standards by around 0.5 per cent at the end of the forecast. This is a minor dent in an immense collapse, and of course as everybody has pointed out only reverses in a small way tax increases at past statements – even on their own terms the government are failing.

Minimum wage

Specifically for those on the minimum wage, the Chancellor has accepted the recommendations of the Low Pay Commission (LPC). This takes the wage floor to £11.44 an hour and extends coverage to everyone aged 21+. This is badly needed and follows pressure from unions and low-pay campaigners. But with prices sky high, and the OBR increasing its inflation forecasts, the minimum wage must be raised to £15 as soon as possible, and extended to all adult workers.

The Low Pay Commission’s recommendations take the minimum wage to 66% of median wages. This is an internationally recognised measure of relative low pay. However, the Chancellor’s claims that he has eliminated low pay should be taken with a pinch of salt. This is a measure of pay distribution which looks at how close low-paid workers are to the median worker. The floor has risen since 2010 but the middle has had no real pay rise over 13 years. The bottom has been catching up, in part, because wages are stagnant for everyone else. The government should set the LPC’s next minimum wage target at 75% of median wages, and this should be delivered alongside a plan for real wage growth for all workers.

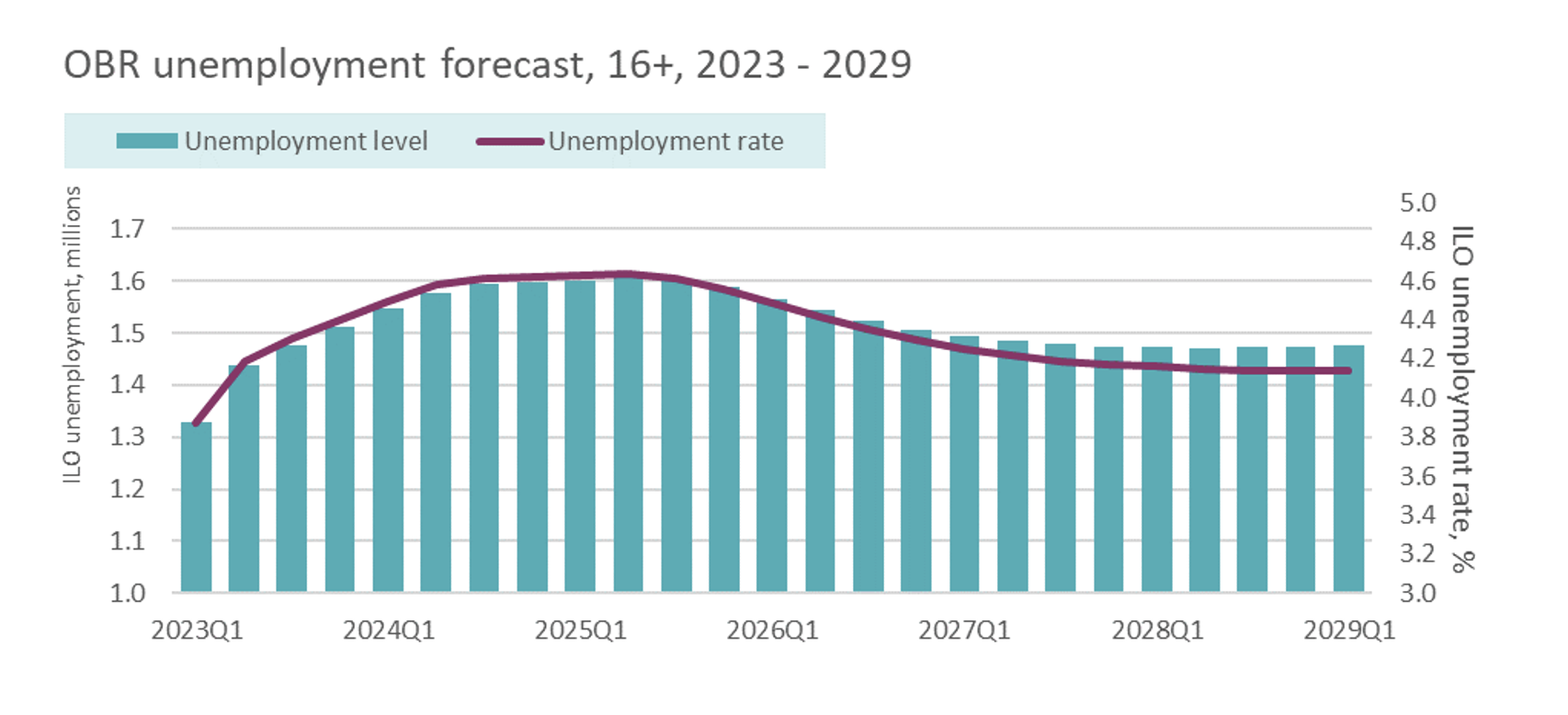

Unemployment rise

The OBR has also predicted that unemployment will steadily rise from now until midway through 2025, estimating there will be 275,000 more people in unemployment than at the start of this year. At no point in the OBR forecasts do they predict unemployment will fall below the level at the start of the year.

It is unfair to put it mildly to penalise individuals for an economic climate which is out of their control. The Chancellor decided to support compulsory work placements, but analysis show this punitive policy does not result in an improved employment outcome.

Skills

The Government plans focus largely on reforms coming in for 16-18 year olds, overlooking the skills gap faced by those already in the labour market. On apprenticeships £50m for a 2-year pilot widely misses the mark. In 2021/22, there were approximately 349,200 apprenticeship starts in England – a 31% decline from the pre-Apprenticeship Levy figures of 509,400 starts in 2015/16 (Source: CIPD). The funds are largely directed at male-dominated sectors, according to the Women’s Budget Group. Other measures are recycled and/or small – though the increase to the pitifully low apprenticeship minimum wage is be welcomed.

Little has been done to reverse cuts to adult and further education budgets since 2010, with spending still significantly below where it was when the government took office. Celebrating an uptick in Level 4 apprenticeships just repeats the ‘virtuous cycle’ where those with the highest levels of qualification receive the most investment in their training. Graduates get most of the training as working adults, and almost half of adults from the lowest socio-economic group receive no training at all after leaving school.

Social security

It is a low bar for this Government when they boast that benefits are being uprated in line with September’s rate of inflation, which is standard practice. Though they have severed the link between inflation and the uprating of benefits numerous times since 2010 – which has slashed vital financial support for families.

And while the Local Housing Allowance has been restored to the 30th percentile after it was last frozen in 2020, it will be frozen again and support reduced for ever-increasing rental prices.

There were also significant cuts to benefit entitlements for some people with long term health conditions. They are expected to lose £400 a month compared to current system, and face the threat of sanctions to enter employment.

The rate at which prices are increasing may have slowed, but families are still struggling with the essentials. Over the last two years the cost of energy has increased by 49 percent while food prices have increased by 28 percent.

Energy prices

And energy bills are a glaring omission from this Autumn Statement.

Household energy bills remain 50% higher than they were in the winter of 2021-2022 (approximately £600 higher for an average household). This means that an estimated 6.3 million households are in fuel poverty (spending more than 10% of their income on energy), and more than 1 million households are in extreme fuel poverty (spending 20% or more of their income on energy). (Estimate by Friends of the Earth and National Energy Action as government data are not yet available.)

Energy prices are expected to remain high or increase. Ofgem today raised the domestic energy price cap by 5%, based on wholesale price volatility.

Many employers will also struggle with rising and volatile energy bills. The UK consistently has some of the highest electricity prices for business in Europe, affecting the ability of UK manufacturers to compete internationally. Unions representing manufacturing workers have consistently campaigned alongside employer bodies for measures to rein in excessive and volatile wholesale energy prices – but these issues seem to be far from the list of priorities of the current Government.

Public services and public finances crises continue

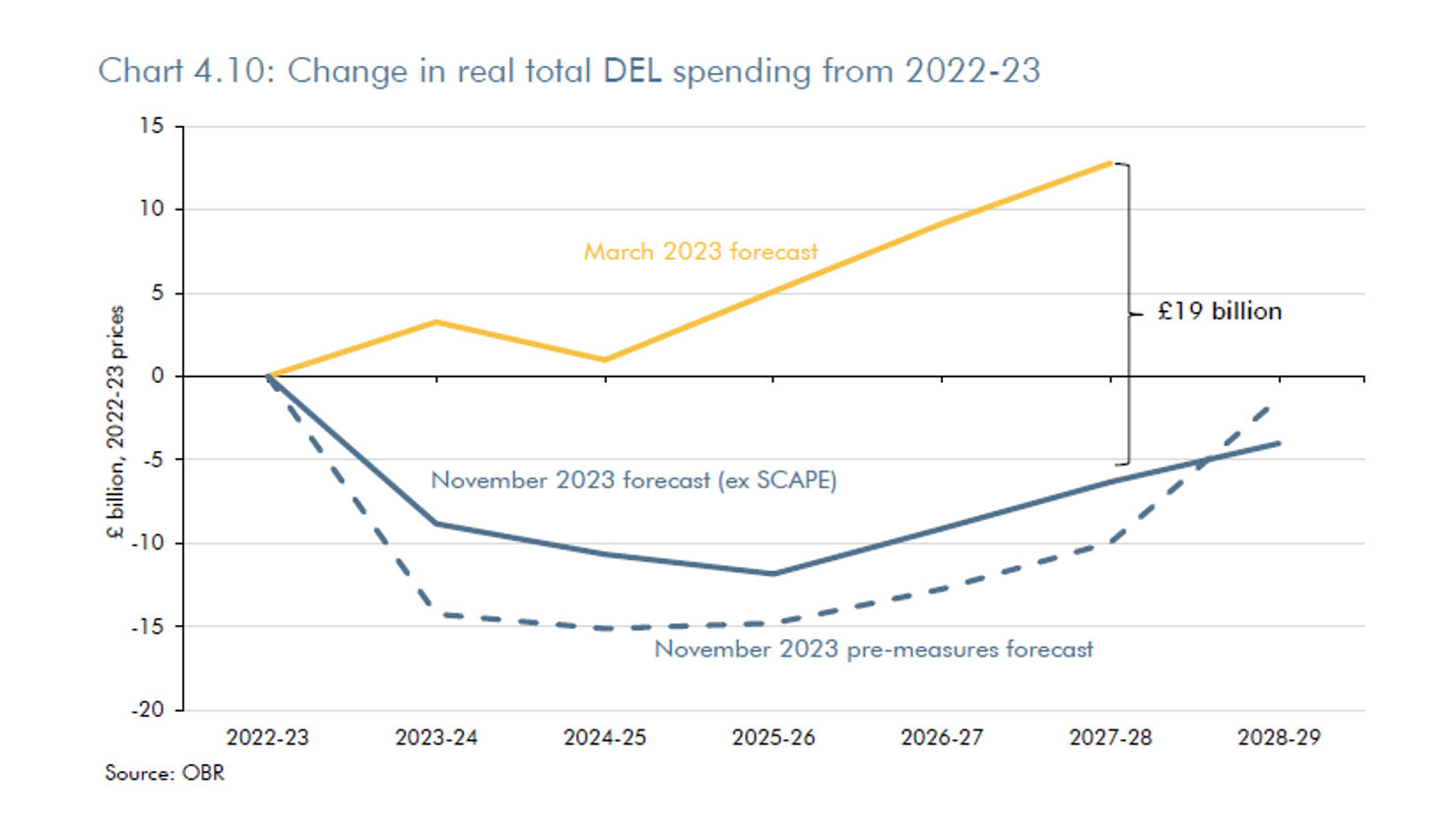

As the OBR gently warn, “it is worth dwelling for a moment on something the Chancellor didn’t announce in his Autumn Statement – which is any major change to departmental spending plans despite significantly higher inflation”.

The government has added “just” £5 billion a year in cash terms to departmental budgets, and this means that “the real spending power of these budgets is eroded by around £19 billion” relative to the previous forecast (as on their chart below).

In 2023-24 the increased budget is allocated for public sector pay increases (£3.9 billion for the NHS in 2023-24, and £0.4 and £1.4 billion for other departments in 2023-24 and 2024-25, respectively). Overall, the OBR have departmental spending growing by 0.9 per cent a year in real terms, down from 1.1 per cent at the March Budget.

Given the government’s political priorities on spending, the OBR stress that unprotected departmental spending is projected to fall by between 2.3 and 4.1 per cent a year in real terms from 2025-26. They wryly observe this (austerity) would “present challenges” and cite the Institute for Government’s recent report finding that “performance in eight out of nine major public services has declined since 2010”. Plainly there is no intention to resolve the crisis in public services and public service recruitment. And ultimately

The public finances overall

For the public finances as a whole, the government has enjoyed a momentary windfall – with less bad than expected growth outturn and higher inflation meaning tax gains (especially with tax thresholds not being uprated) outweighing higher interest and other costs. This has been spent on the NI cut and expensing.

But the Chancellor has made hollow boasts about the improved condition of the public finances. The overall management of the economy for 13 years has meant a disastrous failure for them. Immediately less bad GDP outcomes (next section) have meant marginally improved ratios for this statement. But overall the Conservatives have presided over a huge increase in debt from 65 per cent of GDP in 2009-10 to 98 per cent of GDP in the current financial year. This is an unprecedented deterioration relative to all economic cycles for more than a century.

Growth crisis unended

At the end of his speech the chancellor proclaimed an “Autumn Statement for Growth”. But nothing announced yesterday changed the bottom line. While the forecasts reflected ONS revisions to GDP data and a less bad than expected 2022, growth over the next two years is revised steeply down. And on a medium term view the OBR warn:

“we have revised DOWN our estimate of the medium-term potential GROWTH rate of the economy to 1.6 per cent, from 1.8 per cent in March” (our emphasis)

Of the onslaught in policy measures, the most prominent was making permanent the full expensing of business capital investment. The Chancellor chose to disregard OBR analysis showing both precursor measures (the super-deduction and temporary full expensing in the March 2021 and March 2023 Budgets) had a lower impact on investment levels than predicted (see OBR, Economic and Fiscal Outlook, November 2023, pp 33 – 34).

Introducing full expensing is forecast by the OBR to lead to an increase in business investment of £14 billion between now and 2028-29 and to cost £29.5 bn over the same period. This would appear then to be an extremely inefficient means of increasing business investment, reflecting huge ‘deadweight’ effects, whereby businesses gain generous tax relief on investment that would (likely) have taken place anyway.

The OBR estimates that the measure will raise the capital stock by 0.2 per cent by 2028-29 – a positive, but small, and very costly impact.

Pension saving

The chancellor also had high hopes for the role workers’ £2.5tn of pension savings could play in boosting our flagging economy. But while there were some welcome steps such as setting up a new growth fund through the British Business Bank the plans rely mostly on merging pension schemes in ways that are unlikely to be in the interests of their members, and leaning on funds to put more money into global private equity. These measures were also over shadowed by a poorly thought through proposal to upend the workplace pension system. See our fuller commentary here.

Industrial strategy?

As the Chancellor noted, the lack of long-term certainty over policy decisions (including industrial strategy, taxes, and climate commitments) is a drawback to business decisions to invest. But there was no reassurance in the Autumn Statement that the Government would provide that certainty. While reannouncements of investment commitments to support the automotive, advanced manufacturing, and energy sectors – amounting to £4.5 billion are welcome, this represents only a small proportion of the investment requirements of the Biden-style industrial strategy that the UK needs.

Ending the failure

The failure – as Labour have repeatedly identified – is still a failure of growth. The government need to invest in a stronger economy where growth and fairness go hand in hand, where decent pay means workers spend and businesses produce to meet that spending. A virtuous cycle comes when businesses invest in the face of expansion and optimism, and stronger public services re-enforce the upward dynamic. Fairer and sustainable growth will then support the public finances.

Yet the government continues to take us in the wrong direction. Yesterday’s Autumn Statement showed more strongly than ever why it is time for a change.

Autumn Statement ‘ushers in new era of welfare reform’

A ‘bold new vision for welfare’ backed by nearly £30 billion has been set out by Work and Pensions Secretary Mel Stride

Millions of people will benefit from next generation of welfare reforms and extra support for those most in need, announced at Autumn Statement

Benefits increased by 6.7% and pensions by 8.5%, maintaining commitment to seeing the country through cost of living pressures

DWP Secretary Mel Stride heralds new era offering a “brighter future for millions”

The plans offer unprecedented employment and health support to help over a million people, while protecting those in most need from cost of living pressures – including raising pensions and benefits and increasing help with housing costs.

Long term decisions to provide unprecedented help for people to move off welfare and into work were at the heart of the Government’s plan for growth set out at the Autumn Statement.

While unemployment has been almost halved since 2010, the £2.5bn Back to Work plan will help thousands of people with disabilities, long-term health conditions and the long-term unemployed, to move into jobs. This comes alongside new guarantees for those on the highest tier of health benefits around keeping benefit support to cushion those who try work.

The transformative employment programme comes as the Government continues to protect the most vulnerable, delivering a Triple Lock-protected boost for pensioners and raising benefits in line with inflation next year, worth £20bn taken together.

The changes mean the full rate of the new State Pension will go up by £17.35 per week, while families on Universal Credit will be on average £470 better off next year.

Around 1.6 million households will also benefit from an increase to the Local Housing Allowance – and will be around £800 a year better off on average. Worth more than £7bn over five years, this commitment will support low-income families in the private rented sector with rent costs and help prevent homelessness.

Secretary of State for Work and Pensions, Mel Stride MP said: “Work changes lives. With the next generation of welfare reforms, we will help thousands of people to realise their aspirations and move off benefits into work, while continuing to support the most in need.

“We are taking long term decisions that will build a brighter future for millions, offering unprecedented support to open up opportunity and grow the economy, building on our record that has seen almost four million more people in work since 2010.

“Our reforms will remove the barriers to work that we know some people still face, while we’re boosting benefits and pensions to help with cost of living pressures.”

Welfare reforms announced at the Autumn Statement include:

Uprating working age benefits in line with September’s CPI index figure of 6.7%.

Uprating state pensions in line with September’s earnings figure of 8.5%.

Increasing the Local Housing Allowance to cover the 30TH percentile – worth an average of £830 per year.

Expanded jobcentre support including intensive help for those on Universal Credit

Introducing the Chance to Work Guarantee, which will tear down barriers to work for millions of claimants to try work with no fear of reassessment or losing their health benefit top-ups.

Increasing mental health support for jobseekers by expanding NHS Talking Therapies treatment and the Individual Placement and Support programme, supporting almost 500,000 over five years.

Matching 100,000 people per year with existing vacancies and supporting them in that role through Universal Support.

Rolling out WorkWell to support people at risk of falling into long-term unemployment due to sickness or disability.

Reforming the Work Capability Assessment for new health benefit claimants to better reflect the opportunities available in the modern world of work.

Stricter sanctions for people who should be looking for work but aren’t engaging with jobcentre support.

Building on the Mansion House reforms with further steps to improve private pension returns and grow the economy.

Introducing new Government powers to request data from organisations such as banks when accounts are showing signals of fraud and error.

The Government’s ‘radical new plan’ will stem the flow people falling out of work and onto inactivity benefits due to physical or mental health problems, as it takes the long-term decisions to help people realise their dreams to find a job and build a better life.

With this unprecedented level of employment support comes tougher enforcement of sanctions for fit and able people who should be looking for work but aren’t.

Work coaches will use tools to track people’s attendance at jobs fairs and interviews, and close benefit claims of those able to work who have been sanctioned and no longer receiving money after six months.

Taken together, the package will make sure those who are vulnerable or on the lowest incomes are protected, with intensive support to get them back into work, while ensuring fairness to the taxpayer.

A study to gather vital data on COVID-19 this winter has been launched by the UK Health Security Agency (UKHSA) and the Office for National Statistics (ONS).

The Winter COVID-19 Infection Study (WCIS) will run from November 2023 to March 2024, involving up to 200,000 participants.

UKHSA previously commissioned the Coronavirus Infection Survey (CIS), carried out by the ONS during the pandemic, in partnership with scientific study leads Oxford University.

Recognised globally as the gold standard for surveillance of the virus, CIS gathered and analysed more than 11.5 million swab tests and 3 million blood tests from April 2020 to March 2023.

The new WCIS is a different study and will involve up to 32,000 lateral flow tests being carried out each week, providing key insight into the levels of COVID-19 circulating across the wider community. This sample will be broadly representative of the population according to key characteristics.

While widespread vaccination has allowed us to live with COVID-19, some people remain more vulnerable to severe illness, and this in turn can lead to increased pressures on the NHS over the winter months.

That is why UKHSA is urging eligible adults to book their flu and COVID-19 vaccines online via the NHS website, by downloading the NHS App, or by calling 119 for free, to give themselves the best protection against severe illness and hospitalisation.

UKHSA’s existing surveillance systems already provide up-to-date information on hospital and intensive care unit (ICU) admission rates, but the introduction of this study will allow us to detect changes in the infection hospitalisation rate (IHR), which requires accurate measurement of infection levels in the community.

Calculating the IHR will enable UKHSA to assess the potential for increased demand on health services due to changes in the way the virus is spreading, which could be driven by the arrival of any new variants.

Professor Steven Riley, Director General of Data, Analytics and Surveillance at UKHSA, said: “The data we collected alongside the ONS during the pandemic provided us with a huge amount of valuable insight, so I am delighted that we are able to work together again to keep policymakers and the wider public informed in the coming months.

“UKHSA continues to lead the way internationally on COVID-19 surveillance and by re-introducing a study of positivity in the community, we can better detect changes in the behaviour of the virus.”

The study will use lateral flow devices (LFDs) supplied by UKHSA.

The latest UKHSA technical briefing, published on 22 September, included initial findings of tests performed in the laboratory at Porton Down to examine the effectiveness of LFDs in detecting BA.2.86, and found no reduction in sensitivity compared to previous variants.

The model and scale of this study could also be converted into a programme that captures data on different respiratory viruses, should that be required in future.

Deputy National Statistician Emma Rourke at the ONS said: “ONS is committed to building on the experience of standing up the gold standard CIS. Our resources and statistical expertise are here for the public good, and we are delighted to be delivering this study in partnership with UKHSA.

“There remains a need for robust data to help us continue to understand the virus and its effects during the winter months.

“As well as working to provide UKHSA with regular rates of positivity, we will also be looking at analysis of symptoms, risk factors and the impact of respiratory infections, including long COVID, as part of this important surveillance.”

The first results of the Scottish Census which took place in March 2022 have been released today, which show that the Scottish population has increased by 2.7% since the last Census in 2011 (write Fraser of Allander Institute’s MAIRI SPOWAGE and JOAO SOUSA).

Digging underneath this, there were 585,000 births and 634,800 deaths since the 2011 Census. So, without migration, the Scottish population would have decreased by 49,800. Net migration of +191,000 people is the reason that we have seen this population growth in Scotland.

The Census shows that the population in Scotland grew less quickly than England and Wales (+6.3%) and Northern Ireland (+5.1%).

The main story is of an ageing population

The numbers show a significant increase in the share of the population that is over the age of 65. 1 in 5 people were aged 65 or over in 2022; it was only 1 in 8 in 1971 and 1 in 6 in 2011.

The larger share of older people is largely a good news story, reflecting the success in increasing life expectancy over the long run. But fewer children are also being born.

So not only is today’s share of the population over the age 65 larger than ever before, it will continue to grow in the coming decades (even with the levels of inward net migration seen over the last decade or so).

Chart: Dependency ratios at successive Scottish Census

Source: National Records of Scotland, FAI calculations

This means that the working age population – which produces most economic output and pays the largest share of the taxes that fund public services – will need to support a larger share of the population than in previous decades.

Older people generally also need to rely on health and social care more, which increases funding pressures on public services, and increases the number of people entitled to claim state pension – bringing into focus the cost over the long term of policies such as the triple lock.

This is not a Scottish-specific issue, or even a UK-specific one, but it is one the country will need to grapple with. As the Office for Budget Responsibility and the Scottish Fiscal Commission’s recent analysis showed, if these spending pressures were to be accommodated, it would mean an unsustainable path for the public finances, which would have to be addressed by either tax increases, spending reductions, or (most likely) a combination of the two.

The population is also moving within Scotland

The published results also provide an up-to-date picture of population counts and structure across council areas – and the 2.7% increase in national population has not been equal across the board.

Areas around Edinburgh showed the strongest increases, with Midlothian (16.1%), East Lothian (12.6%) and Edinburgh City itself (7.6%) topping the list. At the other end of the scale, Na h-Eileanan Siar (-5.5%), Inverclyde (-3.8%) and Dumfries and Galloway (-3.6%) showed the sharpest declines. In total, 22 of the 32 council areas showed an increase in population.

These changes in population have also led to changes in the structure of the population in different council areas. The four areas with the largest proportional increase in the share of over 65s (Shetland, Aberdeenshire, Clackmannanshire, Highland) are all lower population density than the national average, which itself is a long way below that of the large urban centres. All four also saw falls in the share of the working age population of 5% or more.

By contrast, Glasgow City saw its share of the working age population increase by 0.6%, and Edinburgh City’s decreased by only 1.6%, well under the average decline across Scotland of 3.7%.

These results serve as an illustration of the difficulties faced by more rural areas of Scotland in attracting people of working age relative to large urban areas, and the disparate effects of an ageing population on different areas of the country.

Are the Census results reliable?

There has been considerable coverage of the approach to the Scottish Census given the challenges that were faced in ensuring a good return rate in order to have as good quality as possible.

National Records of Scotland had to extend the deadline to allow households more time to get the forms in, and ended up with a return rate of 90%, compared to the 94% that they achieved in the 2011 Census. This also compares rather unfavourably to the (admittedly very good) response rate in England and Wales in 2021 of 97% (in 2011, the E&W return rate was also 94%).

So why was the return rate lower than it had been in the past?

For anyone who doesn’t remember, in July 2020, about 9 months before the Scottish Census originally scheduled for 2021 was supposed to take place, National Records of Scotland decided that they would delay the Scottish Census for a year due to “the impact of the Covid pandemic”.

The ONS and NISRA, who are responsible for the Census in England and Wales and Northern Ireland respectively, took a different view and proceeded with their census on the original planned date.

At the time, there was concern about the impact that this delay could have on the coherence of the census data across the UK, and the potential (for ever more) for this incoherence to weaken the power that the Census has to provide a snapshot of the UK population. This is particularly true for the groups that are only really reached well in a full population census – small and underrepresented groups, for example.

However, there is no doubt that this delay had an impact on the return rate for the Scottish Census, perhaps due to the lack of benefit that would have been accrued from the coverage and publicity of the UK-wide census going on at the same time.

Having said that, use of a coverage survey and the additional data sources used to supplement the gaps caused by non-returns is not unusual. Even at 94% coverage, these techniques would be used to ensure that the whole population is reflected in the counts. This is not, in itself, a reason to question the validity of the Census results.

However, the lower response rate does mean more of this is required from these results. And in some places in the country with particularly low return rates, such as Glasgow, it does make the results more uncertain.

National Records of Scotland have assessed the overall margins of error at the Scotland level is similar to 2011: but no doubt will be doing more assessment over the next year(s) on how the lower return rate could affect particular groups or geographies.

TUC General Secretary Paul Nowak declares “now is the time to start a national conversation about taxing wealth”

The TUC has called for a national conversation on taxing wealth, as it publishes new analysis which shows a modest wealth tax on the richest 140,000 individuals – which is around 0.3% of the UK population – could deliver a £10.4 bn boost for the public purse.

The analysis sets out options for taxing the small number of individuals with wealth over £3 million, £5 million and £10 million, excluding pensions.

The TUC says these options are illustrative examples of what a wealth tax could look like, using Spain’s existing policy as a potential model.

“It’s time for a national conversation”

The TUC says it is publishing the analysis to “kickstart a conversation” about tax – with the TUC general secretary Paul Nowak declaring “now is the time to start a national conversation about taxing wealth”.

According to analysis commissioned by the TUC, conducted by Landman Economics, a cumulative one-off wealth tax (excluding pensions wealth) on:

A wealth threshold of £3 million with a marginal tax rate of 1.7% would yield £2.7 billion (with the tax payable on wealth above £3 million by 142,000 individuals or 0.27% of adults in the UK)

A further wealth threshold of £5 million with a marginal tax rate of 2.1% would yield an additional £3.2 billion (with the tax payable on wealth above £5 million by 48,000 individuals or 0.09% of adults in the UK)

A further wealth threshold of £10 million with a marginal tax rate of 3.5 % would yield an additional £4.6 billion (with the tax payable on wealth above £10 million by 17,000 individuals or 0.02% of adults in the UK).

Together this could raise more than £10 billion for the exchequer.

The tax would apply as a marginal rate on wealth and assets above each threshold – in the same way income tax works. For example:

Someone with £3 million wealth would pay nothing.

Someone with £4m wealth would pay tax on £1m of their wealth – paying £17,000.

Someone with £9m would pay tax on £6m of their wealth – paying £118,000

Analysis reveals that of those with wealth over £3 million (excluding pensions), three quarters derives from wealth other than their primary residence, and over half comes from financial wealth:

Net financial (non-pension) wealth: 53.3%

Primary residence: 23.6%

Other residences: 18.7%

Physical wealth: 4.4%

The TUC says further debate is needed on what type of wealth is included in this kind of tax.

The union body has already called on the government to equalise capital gains tax with income tax which could raise around £14 billion.

The union body says it is inherently “unfair and unjust” that people who get income from assets or property get off more lightly than someone who relies on work.

Tale of two Britains

The TUC says increasing wealth inequality is resulting in a “tale of two Britains”.

While working people have been “hit by a pay loss of historic proportions” after the longest wage squeeze in modern history, the wealth of multimillionaires and billionaires has boomed.

Financial wealth over the decade from 2008-10 to 2018-20 increased by around £0.9tn (80 per cent) from £1.1tn to £1.9tn.

TUC General Secretary Paul Nowak said: “It’s time to start a national conversation about how we tax wealth in this country.

“It is absurd that a nurse pays a bigger share of their income in tax than a city trader does on profits from their investment portfolio.

“That’s not only fundamentally unfair and unjust – it’s bad for our economy too.

“Our broken tax system means those at the top are hoarding wealth and getting richer and richer, while working people struggle to get by.

“That is starving our economy of spending – as it’s working people who spend their money on our high streets – and it’s starving our public services of much-needed funds.

“This research sets out potential options for getting those with the broadest shoulders to pay a fairer share.

“This is a debate we should not be afraid of having. The Chancellor should use his autumn statement to make sure the wealthiest pay their fair share of tax.”

Commenting on widening inequality over the past decade, Paul added: “Widening wealth inequality means we are seeing a tale of two Britains.

“While working people are suffering the longest pay squeeze in modern history, the super-rich are coining it in.

“Porsche sales are at record highs, bankers’ bonuses are at eyewatering levels, and CEO pay is surging.

“Enough is enough. We need an economy that rewards work – not just wealth.

“Fair tax must play a central role in rewiring our economy to work for working people.”

Renewed downturn in permanent placements during October

Permanent placements fall amid growing economic uncertainty

Temp billings decline for first time in 26 months

Pay pressures soften, but remain strong overall

Hiring activity across Scotland fell into decline during October, with both permanent staff appointments and temporary billings contracting, according to the latest Royal Bank of Scotland Report on Jobs survey.

Permanent placements have now fallen in two of the past three months, while the downturn in temp billings was the first seen since August 2020. Moreover, the rates of contraction were strong overall amid reports of growing economic uncertainty, softening demand conditions and the deepening cost of living crisis.

October data also revealed further increases in starting salaries and temp wages. However, rates of inflation continued to ease, signalling a mild waning of pressure on pay.

Permanent staff placements fall solidly

October data highlighted a fall in permanent staff placements across Scotland. After a month of growth in September, the respective seasonally adjusted index reverted below the neutral 50.0 threshold to signal the second reduction in three months.

The rate of contraction was the fastest seen in nearly two years and solid, with recruiters often linking the fall to growing economic uncertainty and the cost of living crisis.

At the UK level, a fall in permanent staff hires was also noted, with the rate of decline similar to that seen in Scotland.

Scottish recruitment consultancies signalled a reduction in temp billings during October, thereby ending a 25-month run of expansion. The rate of contraction was the quickest seen since July 2020 during the initial wave of the pandemic and strong overall. According to panellists, the latest fall was driven by reduced activity at clients.

Across the UK as a whole, temp billings were broadly stagnant after rising in each of the prior 26 months.

Downturn in permanent staff supply fastest in three months

Recruiters across Scotland noted a twenty-first successive monthly fall in permanent candidate availability during October. The pace of decline quickened on the month and was marked overall. Panellists generally linked the latest downturn to skill shortages and increased hesitancy to seek out new roles due to rising economic uncertainty.

The pace of reduction across Scotland was more rapid than that recorded for the UK as a whole.

The supply of temp labour across Scotland fell again during October. Despite being severe overall, the rate of decline was the second-slowest in seven months (after September). Recruiters highlighted a lack of European workers and ongoing skill shortages as factors constraining supply.

As has been the case for the last seven months, the rate of contraction in temp staff availability in Scotland was sharper than that seen at the UK level.

Starting salary inflation softens further in October

Latest survey data indicated that average starting salaries for permanent staff in Scotland increased at the slowest pace since June 2021 during October. That said, the pace of wage inflation remained elevated in comparison to the historical average. According to anecdotal evidence, skill and candidate shortages continued to drive up rates of pay.

Data for the UK as a whole also signalled a softer rise in starting salaries during October. Moreover, the pace of inflation was softer than that seen for Scotland for the first time in four months.

As has been the case for the past 23 months, temp wages rose across Scotland during October. While the respective seasonally adjusted index hit an 18-month low, it signalled a sharp rise overall. Greater competition for scarce candidates was cited as a key driver of the latest increase in temp pay.

At the national level, wages also increased at a much slower rate during October. However, the rate of inflation was quicker than that registered in Scotland.

Demand for permanent staff expands at slowest pace in 20 months

Demand for permanent staff grew sharply during October, thereby extending the current period of expansion to 21 months. However, the respective seasonally adjusted index fell for the sixth month running, with the latest reading edging down to a 20-month low.

Across the monitored job categories, IT & Computing registered the steepest rate of expansion, followed by Nursing/Medical/Care.

Recruiters across Scotland noted a twenty-fifth successive monthly rise in temp staff demand during October. While the rate of growth was the weakest since February 2021, it was quicker than that seen across the UK as a whole.

At the sector level, IT & Computing saw the quickest growth in short-term vacancies, followed by Accounts & Financial.

Sebastian Burnside, Chief Economist at Royal Bank of Scotland, commented: “Labour market conditions across Scotland deteriorated in October, as for the first time since August 2020, both permanent placements and temporary billings contracted.

“At the same time, rates of vacancy growth for both permanent and short-term staff continued to ease. Candidate and skill shortages meanwhile stretched the supply of labour thin, with recruiters also noting that increased economic uncertainty had impacted candidate numbers. Though it does seem that market imbalances are becoming less pronounced, the effect on pay remains strong.

“The data therefore suggest that growing uncertainty about the economy and the cost of living crisis are already affecting the labour market, and could weigh further on hiring decisions for the remainder of the final quarter of 2022.”

In his Spring Statement, the Chancellor promised to support families through the cost of living crisis today, and to cut their taxes in the future. But his failure to deliver on both of these means that absolute poverty is expected to rise by 1.3 million people next year, while only one-in-eight workers will see actually see their tax bills fall by the end of the parliament, according to the Resolution Foundation’s overnight analysis of Spring Statement 2022 today.

Inflation Nation shows that faced with an unprecedented squeeze on family’s household finances and a significant boost to the public finances, the Chancellor opted for a big but poorly targeted policy package focused on partially offsetting some of the big tax rises he’d previously announced, rather than on supporting those families hit hardest by the cost of living crisis.

Key findings from the overnight analysis include:

Families face £1,100 income losses. The scale of the cost of living squeeze is such that typical working-age household incomes are to set to fall by 4 per cent in real-terms next year (2022-23), a loss of £1,100, while the largest falls will be among the poorest quarter of households where incomes are set to fall by 6 per cent.

Absolute poverty rises by 1.3 million. The scale and distribution of the cost of living squeeze, coupled with the lack of support for low-income families, means that a further 1.3 million people are set to fall into absolute poverty next year, including 500,000 children – the first time Britain has seen such a rise outside of recessions.

Tax rises for seven-in-eight workers. Considering all income tax changes to thresholds and rates announced by Rishi Sunak, only those earning between £49,100 and £50,300 will actually pay less income tax in 2024-25, and only those earning between £11,000 and £13,500 will pay less tax and National Insurance (NI). Of the 31 million people in work, around 27 million (seven-in-eight workers) will pay more in income tax and NI in 2024-25.

A £11,500 wage loss. With real wages in the midst of a third major fall in a little over a decade, average weekly earnings are on course to rise by just £18 a week between 2008 and 2027, compared to £240 a week had they continued on their pre-financial crisis path. This lost growth is equivalent to a £11,500 annual wage loss for the average worker.

A parliament of pain. Typical household incomes are forecast to fall by 2 per cent across the parliament as a whole (2019-20 to 2024-25), making this parliament the worst on record for living standards, beating the 1 per cent income fall over the course of the 2005-05 to 2010-11 parliament.

Rapid fiscal consolidation. The decision to bank much of the borrowing windfall set out by the OBR sees borrowing set to fall rapidly from 14.8 per cent of GDP in 2020-21 to 1.3 per cent of GDP in 2024-25 – lower than it was expected to reach pre-pandemic. This increases the Chancellor’s fiscal headroom at the end of the parliament from £18 billion to £28 billion, the equivalent of a further 4 to 5p cut in the basic rate of income tax.

Torsten Bell, Chief Executive of the Resolution Foundation, said:“In the face of a cost of living crisis that looks set to make this Parliament the worst on record for household incomes, the Chancellor came to the dispatch box yesterday promising support with the cost of living today, and tax cuts tomorrow. Significant measures were announced on both counts, but the policies do not measure up to the rhetoric.

“The decision not to target support at those hardest hit by rising prices will leave low-and-middle income households painfully exposed, with 1.3 million people, including half a million children, set to fall below the poverty line this coming year.

“And despite the eye-catching 1p cut to income tax, the reality is that the Chancellor’s tax changes mean that seven-in-eight workers will see their tax bills rise. Those tax rises mean the Chancellor is able to point to a swift fiscal consolidation and significant headroom against his fiscal rules.

“The big picture is that Rishi Sunak has prioritised rebuilding his tax-cutting credentials over supporting the low-to-middle income households who will be hardest hit from the surging cost of living, while also leaving himself fiscal flexibility in the years ahead. Whether that will be sustainable in the face of huge income falls to come remains to be seen.”

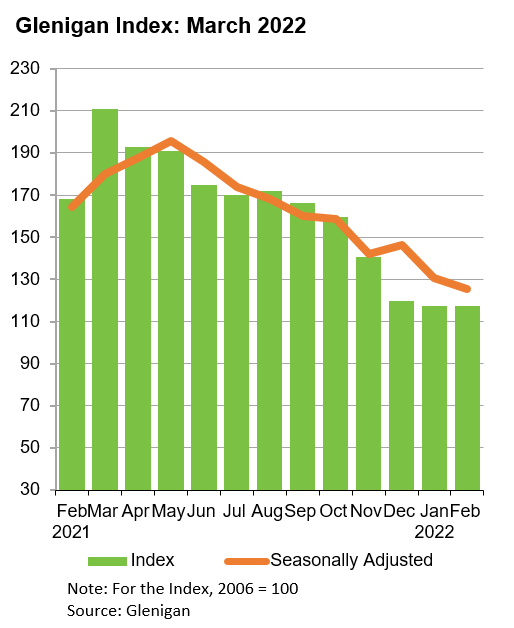

Planning approvals and main contract awards rally, indicating future recovery

Value of underlying work starting on-site (less than £100 million) during the three months to February fell 12% against the preceding three months, down 30% compared with the previous year

Residential project-starts performed poorly, with the value declining 21% against the preceding three-month period to stand 46% lower than a year ago.

Non-residential work starting on-site increased 1% against the preceding three months but fell 2% compared with a year ago

Civil engineering-starts slip back 17% against the preceding three-month period to stand 34% lower than the previous year.

Glenigan, the construction industry’s insight expert, has released the March 2022 edition of its Construction Index.

The Index focuses on February 2022, covering all projects with a total value of £100m or less (unless otherwise indicated), with all figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

Silver Linings

Although decline continued into February, making it the weakest on record, performance-wise since 2015, a strengthening pipeline of planning approvals and main contract awards indicates future, if not immediate, recovery.

This month’s Index shows that, the downward curve, which has persisted since spring 2021, is starting to soften. Supply chain issues might continue to bite, but are less aggressive in material terms.

However, socio-economic ructions caused by the Russia-Ukraine situation will no doubt have an effect as fuel and energy prices are likely to rocket in Q.2 and Q.3. However, the full impact is still too early to appreciate.

Sector Analysis – Residential

Private housing experienced one of the worst overall performances of any sector during this period, with the value of project starts declining by 23% against the preceding three months (to February 2022), standing 50% lower than a year ago.

Social housing fared little better, having remained relatively robust in the preceding months, falling 16% during the period and 26% compared with the previous year.

Looking at the sector overall, work commencing on site fell 21% during the three months to February, and were 46% lower than the previous year.

Sector Specific – Non-Residential

It was a mixed bag in the non-residential sector, however, a few trends are starting to emerge which indicate post-COVID resurgence.

Last month, the Index reported that hotel & leisure grew (23% on the preceding year, and 35% in the three months to January). Once more, the sector has increased performance-wise, standing 23% on the preceding the three months to February and 7% higher than a year ago.

Community & amenity was another March index high-riser, experiencing a spike in activity. Starts jumped 28% against the preceding 3 months and 38% compared with a year ago.

Industrial-starts, the consistent star performer in Index terms, declined 17% during the three-month period covered by the Index. However, the vertical remained steadfast, up 19% on the previous year.

Sprinting ahead, office construction-starts increased by nearly a fifth (17%) in the three months to end of February, but fell marginally short compared to 2021 levels (-6%)

Education and health-starts fell, reflecting a steady decline in both sectors, which will no doubt throw the Government’s levelling-up policy open to scrutiny.

Whilst infrastructure construction-starts indicated green shoots of recovery, increasing 2% during the three months to February, the value fell 27% compared to 2021.

Modest increases will be tempered by another sharp fall for civils work, down 17% against the preceding three months and 34% compared with a year ago. The utilities sector added further salt to the wound once again posting big losses in start terms, falling 43% against the preceding three months to February to stand 48% lower than a year ago.

Regional Analysis

The North East was the best performer during the three months to February, and the only one that experienced growth against this period and 2021 (+6%).

Inconsistency reigned supreme in the other regions. Scotland experienced the greatest increase in project starts against the preceding three months (+13%), but was down 36% on a year ago. Similarly, project starts in London declined by over a quarter (26%) compared to 2021, but increased during the three months to February. The South East was the only other region to experience growth against the preceding three months (+4%).

Unfortunately, all other regions returned poor performances. The value of project starts fell in the West Midlands by 41% during the three months to February, standing 54% lower compared to a year ago. Strong declines were also seen in the East Midlands, East of England, North West and South West on both the Index period covered and 2021.

Commenting on the Index’s findings, Glenigan’s Senior Economist, Rhys Gadsby says, “We urge readers of this Index to maintain a positive outlook. Whilst project starts remain low, the downward curve is softening and, as our most recent Forecast predicted, a gradual rise in the latter half of 2022 is likely.

“External events are skewing the market and no doubt current geopolitical events in Eastern Europe will create some challenges. However, the UK construction industry is incredibly resourceful, and the strong pipeline of planning approvals and contract wins is testament to this. In our view it’s very much a case of ‘keep calm and carry on’.”

Scotland demonstrates strong growth in the wake of pandemic and despite supply shortages

Scotland leads post-COVID industry recovery, growing 124% on the value of project-starts compared to last year

UK value of underlying work (less than £100 million in value) up 35% on 2020 figures but down 16% on preceding three months on a seasonally adjusted basis

Nationwide, retail proves a stand-out sector with 150% growth on project-starts, and residential project starts rise by over a third on previous year

Glenigan, the construction industry’s leading insight and intelligence experts, has released the August edition of its Construction Index.

This report provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals unique insight into results from the second quarter of 2021 and the last twelve months.

Strong growth for Scotland

Scotland has been leading the Covid-recovery, achieving strong growth of 124% on the value of project starts against the previous year, this is despite a 15% dip compared with the previous three months of this year.

UK-wide signs of increase

Despite a slight setback for underlying work (less than £100 million in value) in Q.2 of this year dropping 16% on Q.1, the construction industry is regaining its feet. A rise of 35% on figures in the same time period in 2020 show a sector on the way up.

Residential work on the rise

The value of residential work being carried out on-site is also on the rise, climbing 36% against the previous year. However, this fell 28% compared with the preceding three months (seasonally adjusted) and is down 33% on 2019 figures.

Private housing has also shown growth as one of the best-performing sectors, with the value of project-starts rising by over half (54%). Again, these figures are off the back of an initial dip, down 29% on the preceding three months of this year and 32% on 2019 levels.

Retail and offices provide boost

Retail was the stand-out sector during the period, with project-starts having increased 150% against the previous year up 34% compared with the same period in 2019. Retail-starts also increased 83% compared with the preceding three-month period.

Non-residential sectors also performed above 2020 figures, climbing 43% and increasing by 7% in Q.2 on three months previous.

Health projects show vitality

Despite a slight dip in health project starts in Q.2 of this year falling 12% on Q.1, the sector has seen a 7% rise on the previous year and a 43% increase on the same period in 2019.

Similarly, hotel and leisure project-starts have performed poorly in recent months, however, sector growth has nearly doubled against the previous year (94%) and increased 52% on Q.1 of 2021.

Improvement needed for infrastructure and civil project-starts

An area in need of improvement is underlying civil engineering project-starts which increased just 1% on 2020 but fell 41% on the preceding three months. This was also down 40% compared with the same period in 2019.

Infrastructure starts were also down 16% on the previous year and 49% compared with Q.1 of this year. The sector was also declined by 43% on the same period in 2019.

However, utilities starts show much more promise, increasing by nearly a half on 2020 (47%) but down 18% on the preceding three months of Q.1 of this year.

Strong regional performance

Yorkshire and the Humber also achieved three-digit growth on 2020 (110%) and project-starts in London climbed by over 50% against the previous year but was down 9% on Q.1

Project-starts in the East of England also rose by 58% against last year and were the only region to experience growth against the preceding three months (6%).

Rhys Gadsby, Glenigan’s Economic Analyst, commented on the latest figures: “The positive figures we’ve seen in Scotland serves as a strong indicator the construction sector recovery is not limited to London and the South East.

“However, they should be note of caution. While the value of project-starts remains substantially higher than the lockdown-affected previous year, the value has continued to decline in recent months.

“Material supply problems may have contributed to the fall; however, a decline was expected following a surge in activity, due to pent-up demand, during the first quarter.

“More positively, the speed of decline slowed during July. Main contract awards and detailed planning approval were high compared with previous years, so it is only a matter of time before this has a positive impact on project-starts.

“Furthermore, the successful vaccination roll-out, as well as the ending of restrictions on daily life, should give investors – particularly in non-residential sectors such as hotel & leisure – the confidence to progress projects to site.”

To find out more about Glenigan’s expert insight and leading market analysis click here

{kind=link}

{kind=link}

{kind=link}

{kind=link}