Scotland demonstrates strong growth in the wake of pandemic and despite supply shortages

- Scotland leads post-COVID industry recovery, growing 124% on the value of project-starts compared to last year

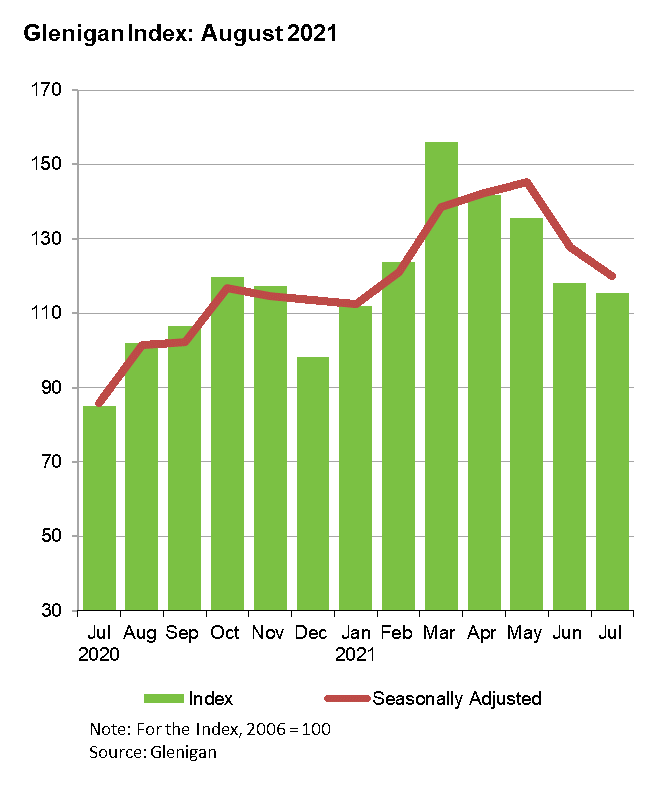

- UK value of underlying work (less than £100 million in value) up 35% on 2020 figures but down 16% on preceding three months on a seasonally adjusted basis

- Nationwide, retail proves a stand-out sector with 150% growth on project-starts, and residential project starts rise by over a third on previous year

Glenigan, the construction industry’s leading insight and intelligence experts, has released the August edition of its Construction Index.

This report provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals unique insight into results from the second quarter of 2021 and the last twelve months.

Strong growth for Scotland

Scotland has been leading the Covid-recovery, achieving strong growth of 124% on the value of project starts against the previous year, this is despite a 15% dip compared with the previous three months of this year.

UK-wide signs of increase

Despite a slight setback for underlying work (less than £100 million in value) in Q.2 of this year dropping 16% on Q.1, the construction industry is regaining its feet. A rise of 35% on figures in the same time period in 2020 show a sector on the way up.

Residential work on the rise

The value of residential work being carried out on-site is also on the rise, climbing 36% against the previous year. However, this fell 28% compared with the preceding three months (seasonally adjusted) and is down 33% on 2019 figures.

Private housing has also shown growth as one of the best-performing sectors, with the value of project-starts rising by over half (54%). Again, these figures are off the back of an initial dip, down 29% on the preceding three months of this year and 32% on 2019 levels.

Retail and offices provide boost

Retail was the stand-out sector during the period, with project-starts having increased 150% against the previous year up 34% compared with the same period in 2019. Retail-starts also increased 83% compared with the preceding three-month period.

Non-residential sectors also performed above 2020 figures, climbing 43% and increasing by 7% in Q.2 on three months previous.

Health projects show vitality

Despite a slight dip in health project starts in Q.2 of this year falling 12% on Q.1, the sector has seen a 7% rise on the previous year and a 43% increase on the same period in 2019.

Similarly, hotel and leisure project-starts have performed poorly in recent months, however, sector growth has nearly doubled against the previous year (94%) and increased 52% on Q.1 of 2021.

Improvement needed for infrastructure and civil project-starts

An area in need of improvement is underlying civil engineering project-starts which increased just 1% on 2020 but fell 41% on the preceding three months. This was also down 40% compared with the same period in 2019.

Infrastructure starts were also down 16% on the previous year and 49% compared with Q.1 of this year. The sector was also declined by 43% on the same period in 2019.

However, utilities starts show much more promise, increasing by nearly a half on 2020 (47%) but down 18% on the preceding three months of Q.1 of this year.

Strong regional performance

Yorkshire and the Humber also achieved three-digit growth on 2020 (110%) and project-starts in London climbed by over 50% against the previous year but was down 9% on Q.1

Project-starts in the East of England also rose by 58% against last year and were the only region to experience growth against the preceding three months (6%).

Rhys Gadsby, Glenigan’s Economic Analyst, commented on the latest figures: “The positive figures we’ve seen in Scotland serves as a strong indicator the construction sector recovery is not limited to London and the South East.

“However, they should be note of caution. While the value of project-starts remains substantially higher than the lockdown-affected previous year, the value has continued to decline in recent months.

“Material supply problems may have contributed to the fall; however, a decline was expected following a surge in activity, due to pent-up demand, during the first quarter.

“More positively, the speed of decline slowed during July. Main contract awards and detailed planning approval were high compared with previous years, so it is only a matter of time before this has a positive impact on project-starts.

“Furthermore, the successful vaccination roll-out, as well as the ending of restrictions on daily life, should give investors – particularly in non-residential sectors such as hotel & leisure – the confidence to progress projects to site.”

To find out more about Glenigan’s expert insight and leading market analysis click here