The outlook for the Scottish and UK economies has weakened, with growth now expected to remain sluggish through the rest of 2025.

In its latest quarterly Economic Commentary, the Institute has downgraded its forecasts for Scottish economic growth to 0.8% in 2025 and 1% in 2026.

This comes despite more upbeat projections from both the Scottish Fiscal Commission (SFC) and the Office for Budget Responsibility (OBR), which have recently upgraded their expectations for 2026 whilst similarly revising down their GDP forecasts for 2025.

Economic growth is now slowing compared to the start of the year and inflation has also edged up to 3.4%, after staying below 3% throughout 2024.

The business environment is also showing signs of strain, with companies reporting cutting back on activities in the first quarter compared to last year, plagued by rises in National Insurance Contributions, which took effect in April, alongside uncertainty surrounding President Trump’s trade tariffs. Indeed, pay growth and employee numbers are down, signalling potential weaknesses in the labour market.

The current state of the economy was not unexpected: Institute Director Professor Mairi Spowage warned of turbulent and uncertain conditions which could last throughout the year in the previous commentary.

Professor Spowage said: “After a strong start to the year, the Scottish economy has faltered in March and April and is essentially the same size in real terms as it was six months ago.

“Unfortunately, the wider business environment and global events are still taking a toll on businesses and consumers, which is having a dampening effect on spending and business investment.”

In addition to the latest economic analysis, the commentary provides an overview of Universal Credit and Legacy Benefits in Scotland, a key element of the nation’s social security system, and summarises key takeaways from June’s spending review and medium-term financial strategy.

Dr Joao Sousa, Deputy Director of the Institute, said: “The fiscal announcements by both governments suggest that there are significant economic challenges in the years and months to come for the UK and Scottish Governments.

“Particularly from 2027-28 onwards, the choices of Government look to become more difficult. Of course, this is the role of the Government in power: but the difficulties of the UK Government this week show that events can quickly derail its plans.”

February House Price Index from Walker Fraser Steele

January’s downturn in prices continues into February

Prices in 2023 experience the largest fall in fourteen years

East Renfrewshire is authority with highest average prices

Sales volumes are low in Jan & Feb – expect higher sales in March

Average Scottish House price now £220,702, down 0.9% on January, up 3% annually

Table 1. Average House Prices in Scotland for the period February 2022 – February 2023

(The prices are end-month smoothed over a 3 month period)

Note: The Walker Fraser Steele Acadata House Price Index (Scotland) provides the “average of all prices paid for houses”, including those made with cash.

Scott Jack, Regional Development Director at Walker Fraser Steele, comments:“Far from experiencing a storm, the Scottish housing market could be said to be navigating choppy waters.

“This is to be expected as January and February are typically slow months for house sales – in part because of the shorter days and extended holidays over the Christmas period. However, the seasonal lull in activity has been amplified by the rise in mortgage costs as a result of the ill-conceived Truss-Kwarteng mini budget.

“Amazingly, notwithstanding that onslaught, the current average house price still remains some £6,300, or 3.0%, above the average price of twelve months earlier. However, through a monthly lens, our index shows that in February 2023 prices continued their descent, falling by a further £2,000 in the month, on top of the £1,750 price decrease in January.

“If we take account of both the change in prices and the number of transactions involved – Edinburgh (17%); Aberdeenshire (9%); South Lanarkshire (9%); North Lanarkshire (7%); East Renfrewshire (6%); and Clackmannanshire (6%) in February accounted for 54% of the £6,300 increase in Scotland’s average house price over the year.

“Of note in Scotland is that many estate agents have noticed an increase in the number of rental properties coming to market. Landlords raised their concerns about the legislation in response to the cost-of-living crisis some time ago. This legislation has followed a sustained period of increased letting agent regulation, higher taxes for landlords and tight rent controls to protect tenants.

“As we emerge from February, we will watch transaction volumes carefully. In each of the last eight years, March transaction totals have always exceeded those of February. We should expect higher sales volumes in next month’s data.”

Commentary: John Tindale, Acadata Senior Housing Analyst

The February housing market

February 2023 continued the downward trend in average prices seen in January, with prices falling by a further £2,000 in the month, on top of the £1,750 price decrease in January. Prices in 2023 to the end of February have therefore dropped by £3,750. Ignoring the price movements associated with the introduction of the LBTT tax in April 2015 and the termination of the LBTT tax-holiday in April 2021, these price reductions represent the largest falls over two months since February/March 2009, some fourteen years ago.

During February 2023, it was the price of flats that again fell the most, down by -1.8% in the month.

So why the price falls? As discussed last month, January and February are typically the weakest months of the year in Scotland’s housing market in terms of transaction levels, which is in part to do with Christmas, when many estate agents remain closed over the holiday period.

When sales levels are low, minor trends – which might otherwise have been obscured by the larger number of sales in the other months of the year – can stand out. For example, estate agents have been reporting that the number of sales of properties which have previously been in the rental market are becoming more noticeable, with the government rent cap and future regulation changes deterring investors in this sector.

Even a small exodus of private investors in buy-to-let properties will have an impact on prices in the winter months. In Edinburgh, for example, the price of an average flat fell from £286k in December 2022 to £275k in February 2023, while in Glasgow average flat prices fell from £180k to £169k over the same period – with these two cities accounting for 38% of Scotland’s flat sales in February.

Despite reporting the largest monthly fall in prices of the last fourteen years, the current average house price still remains some £6,300, or 3.0%, above the average price of twelve months earlier.

Indeed, as can be seen from Figure 1 below, taking a view of price movements in Scotland over the last five years, the dip in prices in January and February 2023 is barely perceptible. The average house price in February 2018 was £178,175 compared to £220,702 in February 2023 – a £42,500, or 24% rise over the period – about which the adage that past performance is no guarantee of future performance is pertinent.

Figure 1. The average house price in Scotland over the five year period February 2018 to February 2023

Local Authority Analysis

Table 2. Average House Prices in Scotland, by local authority area, comparing February 2022, January 2023 and February 202

Table 2 above shows the average house price and percentage change (over the last month and year) by Local Authority Area for February 2022, as well as for January and February 2023, calculated on a seasonal- and mix-adjusted basis. The ranking in Table 2 is based on the local authority area’s average house price for February 2023. Local Authority areas shaded in blue experienced record average house prices in February 2023.

Annual change

The average house price in Scotland in February 2023 has increased by some £6,300 – or 3.0% – over the last twelve months. This annual rate of growth has decreased by -1.6% from January’s 4.6%, which is a slightly smaller fall than the -1.9% reduction seen in January.

However, in February 2023, 23 of the 32 local authority areas in Scotland were still seeing their average prices rise above the levels of twelve months earlier, three fewer than in January. The nine areas where values fell over the year were, in descending order (with newcomers this month marked by an asterisk):- Inverclyde* (-8.7%), Orkney Islands* (-3.0%); Fife (-2.9%), Aberdeen City (-2.1%), Na hEileanan Siar (-2.0%), Glasgow City* (-1.2%), Angus* (-1.2%), Scottish Borders (-0.4%) and Dundee City (-0.2%).

The area with the highest annual increase in average house prices in both January and February 2023 was Clackmannanshire, up by 25.0% and 29.3% respectively over the two months. However, there were only 27 transactions in Clackmannanshire in February 2023, with a small number of transactions frequently being associated with volatile movements in average prices.

On a weight-adjusted basis – which incorporates both the change in prices and the number of transactions involved – there were six local authority areas in February which accounted for 54% of the £6,300 increase in Scotland’s average house price over the year. The six areas in descending order of influence are: – Edinburgh (17%); Aberdeenshire (9%); South Lanarkshire (9%); North Lanarkshire (7%); East Renfrewshire (6%); and Clackmannanshire (6%).

Monthly change

In February 2023, Scotland’s average house price fell in the month by some -£2,000, or -0.9%. This is the largest fall in a single month since March 2009, some fourteen years ago, ignoring the rather artificial falls around the months relating to the introduction of the LBTT in April 2015, as well as the ending of the LBTT tax-holidays in April 2021.

In February 2023, Scotland’s average house price fell in the month by some -£2,000, or -0.9%. This is the largest fall in a single month since March 2009, some fourteen years ago, ignoring the rather artificial falls around the months relating to the introduction of the LBTT in April 2015, as well as the ending of the LBTT tax-holidays in April 2021.

On a weight-adjusted basis, there were four local authority areas in February which accounted for 51% of the -£2,000 decrease in Scotland’s average house price in the month. The four areas in descending order of influence are: – Glasgow (-18%); Edinburgh (-16%); Fife (-9%); and East Lothian (-8%). It is not surprising to find Glasgow and Edinburgh in this listing, given the fall in flat prices, as they are the two authorities with the highest percentage of flats being sold each month, at 67% and 63% of their respective transaction totals.

On a similar theme, Fife has the highest proportion of terraced sales of all the 32 local authorities in Scotland, at 27% – terraced properties also being popular among buy-to-let investors, who may have decided it is time to sell.

The highest increase in average prices in the month was in East Renfrewshire, where – with two detached properties selling for £1 million plus in Newton Mearns, one being a new-build on the Southfield Grange Development – the average price of detached properties in the area rose by £22k in the month.

Overall, in February, the average price in East Renfrewshire increased by 7.7%, causing Edinburgh with its downward movement in prices, to fall into second place in terms of having the highest-valued average house price in Scotland.

Peak Prices

Each month, in Table 2 above, the local authority areas which have reached a new record in their average house prices are highlighted in light blue. In February, there are 5 such authorities, up by one from 4 in January.

Scotland transactions of £750k or higher

Table 3. The number of transactions by month in Scotland greater than or equal to £750k, January 2015 – February 2023

Table 3 shows the number of transactions per month in Scotland which are equal to or greater than £750k. The threshold of £750k has been selected as it is the breakpoint at which the highest rate of LBTT becomes payable.

There were 37 such transactions recorded by RoS relating to February 2023. Currently, this is the fourth-highest February total recorded to date, but there is likely to be an increase to this figure next month, as RoS process additional sales.

According to the RoS data, the highest priced property sold in Scotland in February 2023 was a £1.6 million terraced property in Edinburgh. This contrasts with three properties sold in January at £3 million plus. Although the number of such sales is small, especially in the winter months, it is perhaps an early indication of a slight slowing in sales at the top-end of the market.

Transactions analysis

Figure 2 below shows the monthly transaction count for purchases during the period from January 2015 to January 2023, based on RoS (Registers of Scotland) figures for the Date of Entry.

The chart shows how transactions tend to dip in February from the January totals, which in turn are lower than the totals for the year’s preceding December. In six of the eight years displayed, the February sales total is the lowest of the year. The two occasions when this was not the case was in February 2020 and February 2021.

In February 2020 the Covid pandemic had yet to be identified, with the first lockdown beginning on 23rd March 2020, Phase 1 being introduced on 29th March 2020 and Phase 2 introduced on 19th June 2020. This resulted in an almost total lack of sales in April 2020 – a position clearly visible on the graph.

In 2021 the end of the LBTT tax-holiday was planned, and indeed, did end on 31st March. Consequently, sales of properties were higher than average in the final two months of the scheme – the brown line showing a peak in sales in March 2021. Sales did however slump in April 2021, as the tax-holiday came to an end. April was therefore the month with the lowest level of sales in 2021.

A close study of the eight years displayed in Figure 2 also reveals that each December is followed by a reduction in transactions in the following January, without exception.

Figure 2. The number of sales per month recorded by RoS based on entry date from 2015 – 2023

What we can also learn from Figure 2 is that one of the three months of June, July and August have seen the highest sales of the year in 4 of the 8 years displayed. Finally, in each of the eight years, March transaction totals have always exceeded those of February. One can therefore look forward to higher sales volumes with next month’s data

Heat Map

The heat map below shows the rate of house price growth for the 12 months ending February 2023. As reported above, 23 of the 32 local authority areas in Scotland have seen a rise in their average property values over the last year, the nine exceptions being :- Inverclyde, Orkney Islands, Fife, Aberdeen City, Na h-Eileanan Siar, Glasgow City, Angus, Scottish Borders and Dundee City.

The highest increase on the mainland over the twelve months to February 2023 was in Clackmannanshire at 29.3%, although this was based on a relatively small number of sales. In second place on the mainland was Moray at 14.3%. 4 of the 32 local authority areas had price growth of 10.0% or higher – one fewer than in January 2023.

Comparisons with Scotland

Figure 3. Scotland house prices, compared with England and Wales, North East and North West for the period January 2005-February 2023

Figure 4. A comparison of the annual change in house prices in Scotland, England and Wales, North East and North West for the period January 2020–February 2023

Scotland’s Eight Cities

Figure 5. Average house prices for Scotland’s eight cities from December 2021–February 2023

Figure 6. Average house prices for Scotland’s eight cities February 2023

According to the latest Royal Bank of Scotland Report on Jobs survey, hiring activity fell across Scotland again in November amid greater economic uncertainty and strong cost pressures.

For the second month running, both permanent staff hires and temp billings fell, with the former recording the quickest reduction since June 2020. While staff availability continued to deteriorate, demand for labour expanded at a softer, but still strong rate.

The ongoing imbalance of labour demand and supply led to further rises in both starting salaries and short-temp pay.

Downturn in permanent placements gathers pace

For the second successive month, permanent placements fell across Scotland in November. The rate of reduction quickened from October to the fastest since the initial phase of the pandemic in June 2020 and was sharp overall. Increased market uncertainty and candidate shortages were blamed for the latest drop in permanent staff appointments.

Permanent placements also fell across the UK as a whole for the second month in a row, albeit at a softer pace than that seen in Scotland.

November data highlighted a fall in temp billings across Scotland for the second consecutive month. Adjusted for seasonality, the respective index pointed to a slower and modest pace of decrease. According to anecdotal evidence, concerns about the outlook weighed on labour market activity.

In contrast to the trend seen for Scotland, temp billings expanded modestly at the UK level.

Supply of permanent staff falls steeply in November

As has been the case since February 2021, the supply of permanent staff across Scotland contracted during November. Furthermore, the rate of deterioration was the most severe since May and among the fastest on record. Recruiters stated that a combination of labour and skill shortages, Brexit and economic uncertainty reduced the supply of candidates.

Notably, the downturn in permanent staff supply across Scotland outstripped the UK average for the eighth month in a row.

A twenty-first successive monthly fall in temporary candidates across Scotland was recorded during November. The rate of reduction accelerated on the month, and was the sharpest since June. The decline also exceeded that seen across the UK as a whole. Recruiters blamed the fall on a stronger preference for permanent roles, candidate shortages and economic uncertainty.

Upward pressure on starting salaries intensifies in November

Latest survey data signalled a further rise in salaries awarded to permanent new joiners in Scotland for the twenty-fourth successive month in November. The rate of pay inflation ticked up from October’s 16-month low, and was rapid overall. The latest rise in salaries was attributed to competition for labour amid staff and skill shortages.

For the second month running, Scotland noted a quicker rise in starting salaries than recorded at the UK level.

Average hourly wages increased further across Scotland in November, thereby stretching the current sequence of inflation to two years. The rate of pay growth accelerated from October’s 18-month low and was sharp overall. Scottish recruiters commonly noted that acute skill and candidate shortages continued to exert upward pressure on wages.

Further slowdown in growth of demand for permanent staff in November

November data pointed to another monthly increase in the number of permanent vacancies across Scotland, extending the current run of expansion that began in February 2021. That said, while growth remained strong, the rate of increase weakened to the second-slowest in the aforementioned sequence.

Across the monitored job categories, Nursing/Medical/Care reported the quickest rise in vacancies. Executive & Professional and Hotel & Catering reported reduced demand for permanent staff.

Recruiters across Scotland signalled a twenty-sixth successive monthly rise in temporary vacancies during November. However, the rate of expansion cooled since the previous month and was the softest seen since February 2021.

IT & Computing registered the quickest upturn in short-term vacancies, followed by Accounts & Financial.

Sebastian Burnside, Chief Economist at Royal Bank of Scotland, commented: “Following the post-pandemic hiring boom, the latest Report on Jobs survey indicates that recruitment activity lost further momentum in November amid a slowdown across the economy.

“Greater uncertainty around the outlook and candidate shortages have taken a toll on staff hiring across Scotland. Latest data indicated a notably steeper contraction in permanent placements, while temp billings fell for the second consecutive month.

“At the same time, labour scarcity resulted in strong growth in pay, with both starting salaries and hourly wages rising at sharper rates during November.

“The steeper drop in candidate availability across Scotland, which was often blamed on a generally low unemployment rate, fewer foreign workers, worries over the economic climate and cost of living crisis, is likely to add further upwards pressure on pay in the months ahead, particularly if firms want to attract and secure the skilled workers they need.”

Renewed downturn in permanent placements during October

Permanent placements fall amid growing economic uncertainty

Temp billings decline for first time in 26 months

Pay pressures soften, but remain strong overall

Hiring activity across Scotland fell into decline during October, with both permanent staff appointments and temporary billings contracting, according to the latest Royal Bank of Scotland Report on Jobs survey.

Permanent placements have now fallen in two of the past three months, while the downturn in temp billings was the first seen since August 2020. Moreover, the rates of contraction were strong overall amid reports of growing economic uncertainty, softening demand conditions and the deepening cost of living crisis.

October data also revealed further increases in starting salaries and temp wages. However, rates of inflation continued to ease, signalling a mild waning of pressure on pay.

Permanent staff placements fall solidly

October data highlighted a fall in permanent staff placements across Scotland. After a month of growth in September, the respective seasonally adjusted index reverted below the neutral 50.0 threshold to signal the second reduction in three months.

The rate of contraction was the fastest seen in nearly two years and solid, with recruiters often linking the fall to growing economic uncertainty and the cost of living crisis.

At the UK level, a fall in permanent staff hires was also noted, with the rate of decline similar to that seen in Scotland.

Scottish recruitment consultancies signalled a reduction in temp billings during October, thereby ending a 25-month run of expansion. The rate of contraction was the quickest seen since July 2020 during the initial wave of the pandemic and strong overall. According to panellists, the latest fall was driven by reduced activity at clients.

Across the UK as a whole, temp billings were broadly stagnant after rising in each of the prior 26 months.

Downturn in permanent staff supply fastest in three months

Recruiters across Scotland noted a twenty-first successive monthly fall in permanent candidate availability during October. The pace of decline quickened on the month and was marked overall. Panellists generally linked the latest downturn to skill shortages and increased hesitancy to seek out new roles due to rising economic uncertainty.

The pace of reduction across Scotland was more rapid than that recorded for the UK as a whole.

The supply of temp labour across Scotland fell again during October. Despite being severe overall, the rate of decline was the second-slowest in seven months (after September). Recruiters highlighted a lack of European workers and ongoing skill shortages as factors constraining supply.

As has been the case for the last seven months, the rate of contraction in temp staff availability in Scotland was sharper than that seen at the UK level.

Starting salary inflation softens further in October

Latest survey data indicated that average starting salaries for permanent staff in Scotland increased at the slowest pace since June 2021 during October. That said, the pace of wage inflation remained elevated in comparison to the historical average. According to anecdotal evidence, skill and candidate shortages continued to drive up rates of pay.

Data for the UK as a whole also signalled a softer rise in starting salaries during October. Moreover, the pace of inflation was softer than that seen for Scotland for the first time in four months.

As has been the case for the past 23 months, temp wages rose across Scotland during October. While the respective seasonally adjusted index hit an 18-month low, it signalled a sharp rise overall. Greater competition for scarce candidates was cited as a key driver of the latest increase in temp pay.

At the national level, wages also increased at a much slower rate during October. However, the rate of inflation was quicker than that registered in Scotland.

Demand for permanent staff expands at slowest pace in 20 months

Demand for permanent staff grew sharply during October, thereby extending the current period of expansion to 21 months. However, the respective seasonally adjusted index fell for the sixth month running, with the latest reading edging down to a 20-month low.

Across the monitored job categories, IT & Computing registered the steepest rate of expansion, followed by Nursing/Medical/Care.

Recruiters across Scotland noted a twenty-fifth successive monthly rise in temp staff demand during October. While the rate of growth was the weakest since February 2021, it was quicker than that seen across the UK as a whole.

At the sector level, IT & Computing saw the quickest growth in short-term vacancies, followed by Accounts & Financial.

Sebastian Burnside, Chief Economist at Royal Bank of Scotland, commented: “Labour market conditions across Scotland deteriorated in October, as for the first time since August 2020, both permanent placements and temporary billings contracted.

“At the same time, rates of vacancy growth for both permanent and short-term staff continued to ease. Candidate and skill shortages meanwhile stretched the supply of labour thin, with recruiters also noting that increased economic uncertainty had impacted candidate numbers. Though it does seem that market imbalances are becoming less pronounced, the effect on pay remains strong.

“The data therefore suggest that growing uncertainty about the economy and the cost of living crisis are already affecting the labour market, and could weigh further on hiring decisions for the remainder of the final quarter of 2022.”

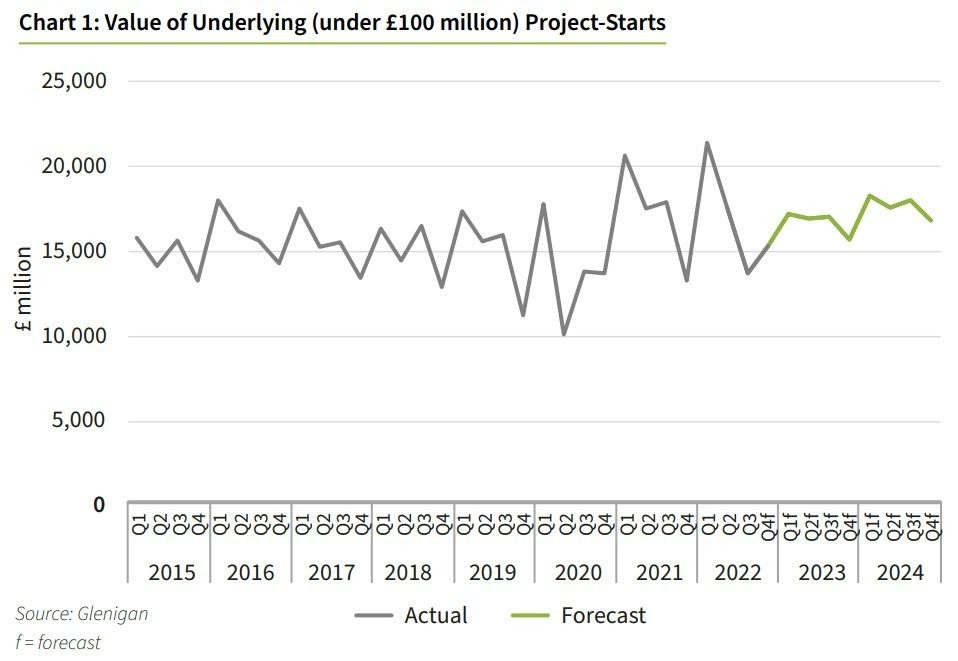

Glenigan’s autumn 2022-2024 Construction Forecast indicates poor market conditions are stifling construction activity, predicting a return to growth by 2024

Glenigan, one of the construction industry’s leading insight and intelligence experts, has released its widely anticipated autumn UK Construction Industry Forecast 2023-2024.

The key takeaway from this Forecast, which focuses on the next two years (2023-2024), is that the construction industry will struggle in the face of extremely challenging economic conditions, with predicted growth in decline during 2022 (-2%) and 2023 (-2%).

However, the sunnier uplands, although far off in the distance, are starting to emerge on the horizon, with a 6% increase predicted in 2024.

The slower road to recovery

Post-pandemic project-starts recovery has lost considerable momentum during the second half of 2022. Forecast to slip back by 2% by the end of the year, and in 2023, it paints a dim picture of activity levels in the short term.

Glenigan predicts the next 24 months to be a challenging period for the construction industry, with ongoing material, labour, and energy supply chain disruption continuing to hold back activity for the foreseeable future.

These external events have resulted in rocketing inflation, rising interest rates, and stalled economic growth, affecting the pipeline of future work. This has been further compounded by the promise of higher tax, utility bills, and rising mortgage costs which has constrained consumer-related construction, including private housing, retail, and hotel and leisure.

The situation has prompted some clients, contractors and developers to pause or scale back on planned investments, further stagnating output. This was confirmed by the value of projects securing detailed planning consent during the first nine months of 2022 dropping by 5%, and main contract awards falling by 8% against the same period in 2021.

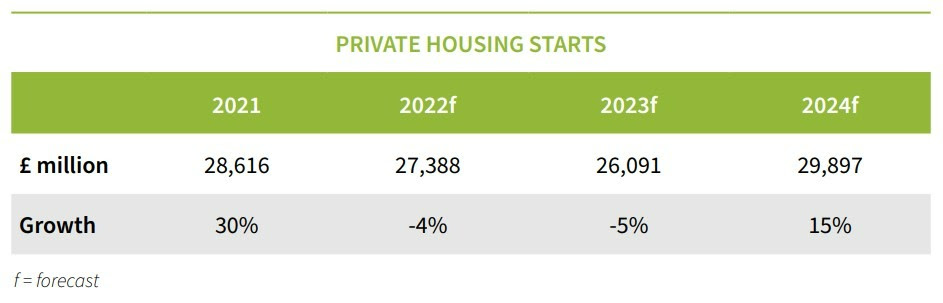

Resurgence in private residential construction

Housing market activity cooled-off in 2022, and is predicted to slow further in 2023 as developers respond to weakening market conditions.

Project-starts are forecast to drop 4% this year, with a further 5% decline next, as lower household incomes, higher mortgage rates and lack of affordable homes continues to afflict the wider housing market.

The reduction in stamp duty rates announced in the mini-Budget will provide a small benefit to first time buyers. However, the end of the government’s Help to Buy scheme has removed direct support for new builds, coupled with mortgage providers significantly raising rates in reaction to the current rate of inflation, meaning that any benefit for first time buyers will be negated for the foreseeable future.

Nevertheless, the growing prospect of a stabilising economy in 2023, prompted by a changing of the guard at Number 10, and gradually improving consumer confidence over the next two years supports a forecast of a respectable 15% rise in residential project-starts during 2024.

Social housing slips back

In the public sector, the social housing project-starts prediction is less positive, forecast to slip back during 2022 and 2023, following a rapid 16% recovery in 2021 as housing associations pressed on with schemes delayed during the pandemic.

Despite improved funding, increased construction costs appear to be significantly constraining development activity, with approvals similarly falling back over the past 12 months.

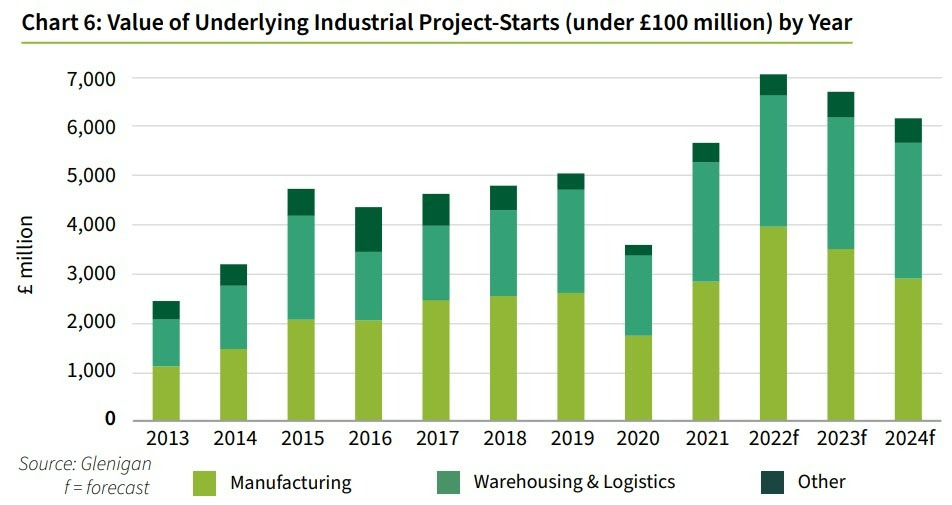

Industrial Consolidation

Industrial project-starts have enjoyed a strong rebound post-pandemic, a rise which has largely been driven by logistics and light industrial projects as significant growth areas. Looking forward, the sector faces a period of consolidation during 2023 and 2024 as the recent spurt in activity inevitably slows.

Weak domestic and overseas demand is expected to temper manufacturing investment in facilities, but warehousing and logistics premises are forecast to remain a growth area. This is due largely to a long-term shift towards online retailing, resulting in continued demand for logistics space, and accounting for the majority of industrial project-starts’ 25% growth in 2022.

Retail tails-off

In the short term, however, the demand for both logistics and retail space is expected to be damped by weak retail sales as consumer confidence falls in response to higher inflation and falling earnings.

An overhang of empty retail premises, weak consumer spending, and the growth in online sales’ market share is predicted to constrain retail construction starts over the forecast period.

Despite this, investment by discount supermarkets Aldi and Lidl are set to be a bright spot within the sector over the forecast period.

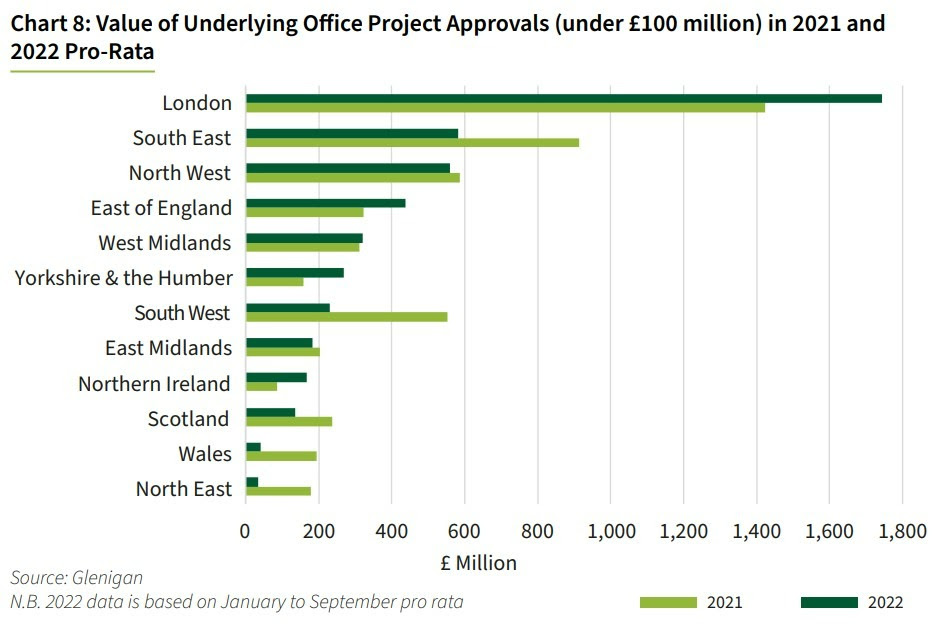

Back to the office

Office starts have also bounced back sharply since 2021, increasing by 27%. The Covid-19 pandemic radically altered working trends globally as many businesses shifted to hybrid working, reducing overall floorspace requirements.

Despite this, the sector is predicted to benefit over the forecast period from a rise in refurbishment projects as tenants and landlords adapt premises to further accommodate these changing work patterns. Conversely, new build office projects are likely to be slower to recover as developers continue to assess the long-term demand for additional office accommodation.

Work, rest and delay

The squeeze on household budgets is set to curb consumers’ discretionary spending in the hospitality and leisure industries. The hospitality sector is still recovering from operational restrictions during Lockdown, as well as reduced revenues due to fewer overseas visitors.

Combined with spiking energy costs over the last 12 months, as well as a potential fall-off in domestic custom over 2023, the hospitality sector will be under considerable pressure. This is predicted to result in retrenchment, causing further delays to project-starts as asset owners wait for confidence to return.

Investment bolsters public sector

A core pillar of the Government’s UK Growth Strategy, public sector investment was set to be an important driver of construction activity over the forecast period. Funding for rail projects and regulated utilities in particular have been tipped to provide the bulk of the output over the forecast period.

However, as a new administration begins, with an ambition to balance the public finance books, planned capital funding allocation may be vulnerable, with a potential range of departmental cuts on the horizon to protect the economy against a looming recession.

Securing our energy infrastructure

Energy security will no doubt remain a national priority following the sharp rises in energy prices over the course of 2022, and an over-dependence on gas-powered electricity. This is expected to drive investment in offshore wind farms, solar PV, increasing our nuclear capacity and strengthening nascent hydrogen capture capabilities.

Building for future generations

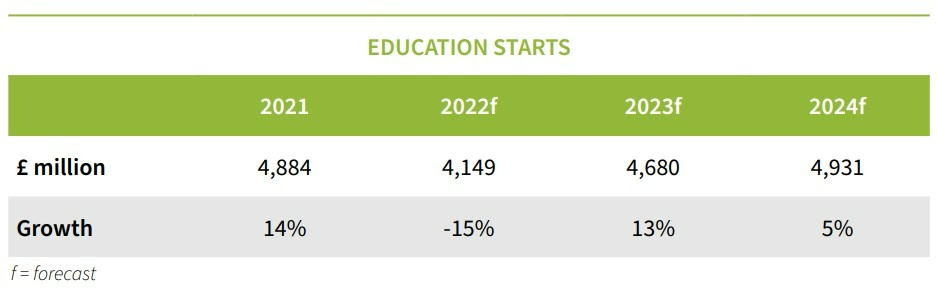

The Government is also committed to rebuilding 500 schools over the coming decade. The latest Spending Review includes additional capital funding for the Department of Education, in a move to tackle the shortage of secondary school places. This is expected to support growth in school building projects in 2023 after a weak performance over the last year.

Healthier predictions

Positively, health sector project-starts remained high during both 2021 and 2022, with an optimistic outlook for the future as a 3.8% real-term growth rate in NHS capital funding is set to maintain project-starts at a high level over the forecast period.

Whilst starts are forecast to slip back 6% in 2023, the value of work started during 2021 and 2022 remains above pre-pandemic levels.

Commenting on the Forecast, Glenigan’s economic director Allan Wilen says, “Construction will face a challenging environment in the coming year as the Russia-Ukraine war continues to hinder the UK’s post-Covid recovery, exacerbating supply chain disruption, resulting in materials and energy shortages, and leading to cost inflation and dented market confidence.

“The pattern of UK construction activity is being reshaped by economic slowdown, but structural changes are expected to create new opportunities in warehouse & logistics, office refurbishment and new housing schemes. Going forward, it will be crucial for firms to be responsive and adaptable in order to mitigate risks in the current marketplace and exploit new opportunities as they emerge over the forecast period.”

To request a copy of Glenigan’s November 2022 Forecast click here.

To find out more about Glenigan, its expert insight and leading market analysis, click here.