There’s been another busy week of economic and fiscal news to cover. The main headline is of course that the Bank of England Monetary Policy Committee (MPC) decided to raise interest rates for the eighth successive time, to 3%.

Also grabbing the headlines was the forecast that, if interest rates follow market expectations and go up to 5.25% by Q3 2023, the economy is likely to contract for 2 years, only returning to growth in Q3 2024.

The Governor of the Bank, Andrew Bailey, made clear that it was possible that the markets has over done the likely pathway for rates, implying that they may not end up getting above 5%.

But, as the chart below shows, their view is that the economy is in for a rough time over the next 2-3 years, whatever the specific pathway for rates. Whatever happens, their expectation is that we will not be above pre-pandemic levels of output by the end of 2025.

Chart: Outlook for UK GDP Growth, 2019 Q4=100

Source: BoE

On Wednesday, we published our latest Scottish Business Monitor, covering Q3 2022, which showed that business sentiment is now in negative territory for the first since the end of 2020.

Chart: Net balance (%) of firms expecting an increase in their volume of business over the next six months, Q1 1998 – Q3 2022

*Net balance of firms is defined as the share of firms reporting higher minus the share of firms reporting lower

With the price of goods, energy, and borrowing on the rise, the majority of Scottish firms that we surveyed are expecting to wind down their operations or pass on costs to their consumers over the next year.

However, there is some good news from our latest survey. Supply chain issues continue to ease, which may dampen inflationary pressures, and the ongoing energy crisis has motivated Scottish businesses to consider making energy-efficient improvements to their processes.

Additionally, In the most recent quarter, half of responding businesses reported that they had vacancies to hire new members of staff, down from 56% reported in the previous quarter.

Of those firms with vacancies, 90% were finding them difficult to fill – up 3 percentage points since the last survey. A lack of skills and applications continue to be the main barriers to filling job posts, and, increasingly, wage expectations are making it difficult for Scottish firms to hire the staff that they need.

Unsurprisingly, Scottish firms expect energy bills and wages to be their main cost pressures in the coming 6 months.

Scottish Economy contracts in August

Somewhat lost in the other news on Wednesday (see below) was new GDP data from the Scottish Government for August.

This showed that GDP fell by 0.3% in August, taking the Scottish economy below pre-pandemic levels of output – very consistent with the messages we saw from the Bank about a likely contraction overall in Q3.

The contraction was driven mainly by a fall in services output. In a sign of things to come, consumer facing services fell by 2.4%, chiming with what we are hearing from businesses.

Scottish Government cuts health funding to fund pay deals

On Wednesday, we had the Scottish Government’s Emergency Budget Review. We gave our initial reactions here, and the coverage since the publication on Wednesday has focussed very much on the cuts made to health spending to fund pay deals for health workers.

What is clear is that this may not be the end of the story for the 2022-23 budget. John Swinney in the Chamber made it clear that there could be further implications for the Scottish Budget from the UKG’s Autumn Budget on 17th November, perhaps even for 2022-23. And it is also clear that many pay deals are far from settled.

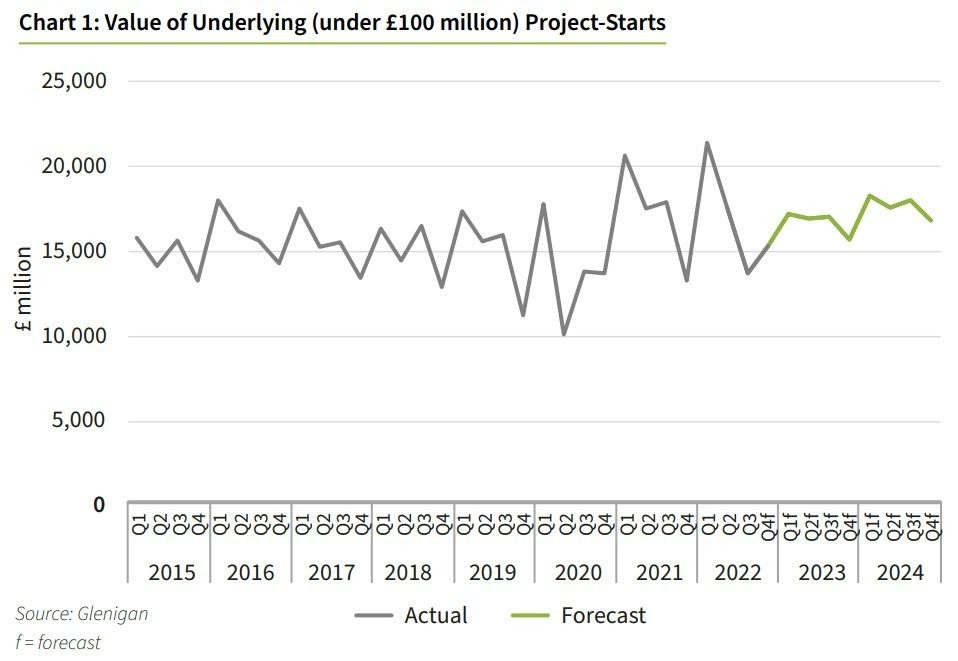

Glenigan’s autumn 2022-2024 Construction Forecast indicates poor market conditions are stifling construction activity, predicting a return to growth by 2024

Glenigan, one of the construction industry’s leading insight and intelligence experts, has released its widely anticipated autumn UK Construction Industry Forecast 2023-2024.

The key takeaway from this Forecast, which focuses on the next two years (2023-2024), is that the construction industry will struggle in the face of extremely challenging economic conditions, with predicted growth in decline during 2022 (-2%) and 2023 (-2%).

However, the sunnier uplands, although far off in the distance, are starting to emerge on the horizon, with a 6% increase predicted in 2024.

The slower road to recovery

Post-pandemic project-starts recovery has lost considerable momentum during the second half of 2022. Forecast to slip back by 2% by the end of the year, and in 2023, it paints a dim picture of activity levels in the short term.

Glenigan predicts the next 24 months to be a challenging period for the construction industry, with ongoing material, labour, and energy supply chain disruption continuing to hold back activity for the foreseeable future.

These external events have resulted in rocketing inflation, rising interest rates, and stalled economic growth, affecting the pipeline of future work. This has been further compounded by the promise of higher tax, utility bills, and rising mortgage costs which has constrained consumer-related construction, including private housing, retail, and hotel and leisure.

The situation has prompted some clients, contractors and developers to pause or scale back on planned investments, further stagnating output. This was confirmed by the value of projects securing detailed planning consent during the first nine months of 2022 dropping by 5%, and main contract awards falling by 8% against the same period in 2021.

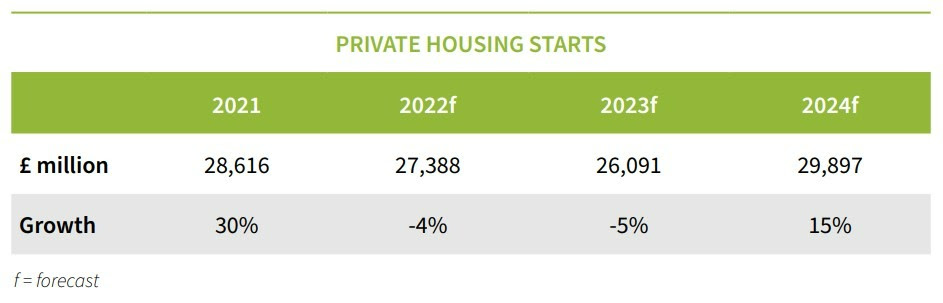

Resurgence in private residential construction

Housing market activity cooled-off in 2022, and is predicted to slow further in 2023 as developers respond to weakening market conditions.

Project-starts are forecast to drop 4% this year, with a further 5% decline next, as lower household incomes, higher mortgage rates and lack of affordable homes continues to afflict the wider housing market.

The reduction in stamp duty rates announced in the mini-Budget will provide a small benefit to first time buyers. However, the end of the government’s Help to Buy scheme has removed direct support for new builds, coupled with mortgage providers significantly raising rates in reaction to the current rate of inflation, meaning that any benefit for first time buyers will be negated for the foreseeable future.

Nevertheless, the growing prospect of a stabilising economy in 2023, prompted by a changing of the guard at Number 10, and gradually improving consumer confidence over the next two years supports a forecast of a respectable 15% rise in residential project-starts during 2024.

Social housing slips back

In the public sector, the social housing project-starts prediction is less positive, forecast to slip back during 2022 and 2023, following a rapid 16% recovery in 2021 as housing associations pressed on with schemes delayed during the pandemic.

Despite improved funding, increased construction costs appear to be significantly constraining development activity, with approvals similarly falling back over the past 12 months.

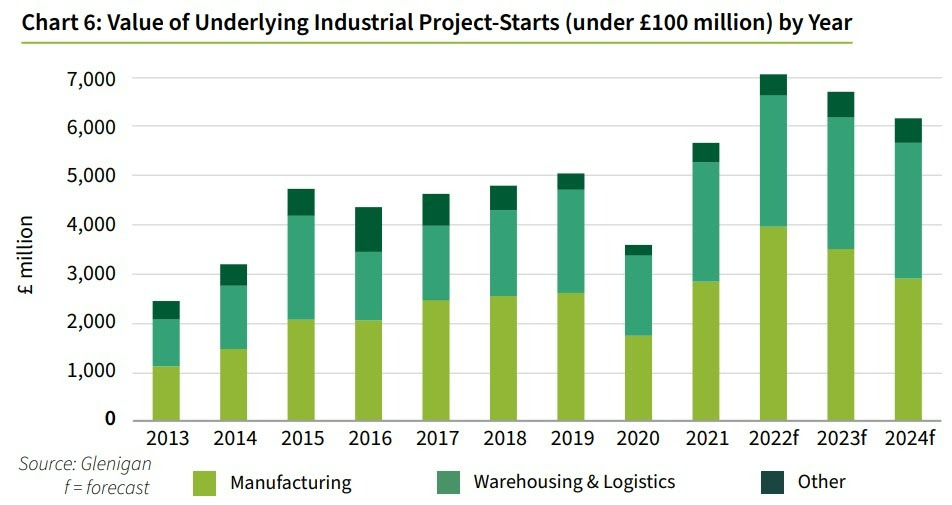

Industrial Consolidation

Industrial project-starts have enjoyed a strong rebound post-pandemic, a rise which has largely been driven by logistics and light industrial projects as significant growth areas. Looking forward, the sector faces a period of consolidation during 2023 and 2024 as the recent spurt in activity inevitably slows.

Weak domestic and overseas demand is expected to temper manufacturing investment in facilities, but warehousing and logistics premises are forecast to remain a growth area. This is due largely to a long-term shift towards online retailing, resulting in continued demand for logistics space, and accounting for the majority of industrial project-starts’ 25% growth in 2022.

Retail tails-off

In the short term, however, the demand for both logistics and retail space is expected to be damped by weak retail sales as consumer confidence falls in response to higher inflation and falling earnings.

An overhang of empty retail premises, weak consumer spending, and the growth in online sales’ market share is predicted to constrain retail construction starts over the forecast period.

Despite this, investment by discount supermarkets Aldi and Lidl are set to be a bright spot within the sector over the forecast period.

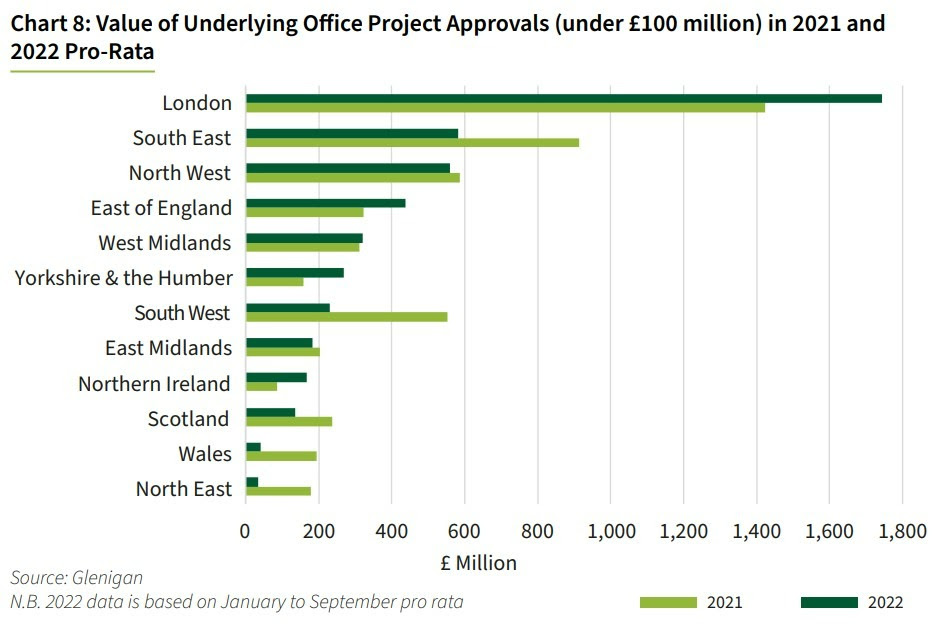

Back to the office

Office starts have also bounced back sharply since 2021, increasing by 27%. The Covid-19 pandemic radically altered working trends globally as many businesses shifted to hybrid working, reducing overall floorspace requirements.

Despite this, the sector is predicted to benefit over the forecast period from a rise in refurbishment projects as tenants and landlords adapt premises to further accommodate these changing work patterns. Conversely, new build office projects are likely to be slower to recover as developers continue to assess the long-term demand for additional office accommodation.

Work, rest and delay

The squeeze on household budgets is set to curb consumers’ discretionary spending in the hospitality and leisure industries. The hospitality sector is still recovering from operational restrictions during Lockdown, as well as reduced revenues due to fewer overseas visitors.

Combined with spiking energy costs over the last 12 months, as well as a potential fall-off in domestic custom over 2023, the hospitality sector will be under considerable pressure. This is predicted to result in retrenchment, causing further delays to project-starts as asset owners wait for confidence to return.

Investment bolsters public sector

A core pillar of the Government’s UK Growth Strategy, public sector investment was set to be an important driver of construction activity over the forecast period. Funding for rail projects and regulated utilities in particular have been tipped to provide the bulk of the output over the forecast period.

However, as a new administration begins, with an ambition to balance the public finance books, planned capital funding allocation may be vulnerable, with a potential range of departmental cuts on the horizon to protect the economy against a looming recession.

Securing our energy infrastructure

Energy security will no doubt remain a national priority following the sharp rises in energy prices over the course of 2022, and an over-dependence on gas-powered electricity. This is expected to drive investment in offshore wind farms, solar PV, increasing our nuclear capacity and strengthening nascent hydrogen capture capabilities.

Building for future generations

The Government is also committed to rebuilding 500 schools over the coming decade. The latest Spending Review includes additional capital funding for the Department of Education, in a move to tackle the shortage of secondary school places. This is expected to support growth in school building projects in 2023 after a weak performance over the last year.

Healthier predictions

Positively, health sector project-starts remained high during both 2021 and 2022, with an optimistic outlook for the future as a 3.8% real-term growth rate in NHS capital funding is set to maintain project-starts at a high level over the forecast period.

Whilst starts are forecast to slip back 6% in 2023, the value of work started during 2021 and 2022 remains above pre-pandemic levels.

Commenting on the Forecast, Glenigan’s economic director Allan Wilen says, “Construction will face a challenging environment in the coming year as the Russia-Ukraine war continues to hinder the UK’s post-Covid recovery, exacerbating supply chain disruption, resulting in materials and energy shortages, and leading to cost inflation and dented market confidence.

“The pattern of UK construction activity is being reshaped by economic slowdown, but structural changes are expected to create new opportunities in warehouse & logistics, office refurbishment and new housing schemes. Going forward, it will be crucial for firms to be responsive and adaptable in order to mitigate risks in the current marketplace and exploit new opportunities as they emerge over the forecast period.”

To request a copy of Glenigan’s November 2022 Forecast click here.

To find out more about Glenigan, its expert insight and leading market analysis, click here.

Brexit has cost Edinburgh the equivalent of £211.4 million as Scottish exports have plummeted since the UK left the EU to the value of £2.2bn.

Figures from HMRC show that exports have dropped 13% in the past two years from £16.7bn to £14.5bn.

The £2.2bn loss is equivalent to Edinburgh losing £211.4 million.

Commenting, Gordon Macdonald MSP said: “Brexit has been an unmitigated disaster for every area of Scotland, including in Edinburgh. These latest figures show why it is essential for Scotland to become independent and re-join the European Union.

“Only with independence can we get back on the road towards prosperity as both Labour and the Tories offer no way back to the European Union, just continuing decline under Westminster control.

“Industries in Edinburgh and across Scotland are suffering as a result of the disastrous Brexit, the only way Scotland can flourish and realise our full potential is by becoming an independent country in the European Union.”

Bank of Scotland’s Business Barometer for October 2022 shows:

Business confidence in Scotland fell 10 points during the last month to 5%

Country’s businesses identify top growth opportunities as evolving their offering (33%), investing in their teams (29%) and entering new markets (27%)

Overall UK business confidence fell one point during the last month to 15%, with five out of 11 nations and regions reporting a higher reading than September

Business confidence in Scotland fell 10 points during October to 5%, according to the latest Business Barometer from Bank of Scotland Commercial Banking – conducted between 3rd-17th October.

Companies in Scotland reported lower confidence in their own business prospects month-on-month, down 11 points at 22%. When taken alongside their optimism in the economy, down 10 points to -14%, this gives a headline confidence reading of 5%.

Scottish businesses identified their top target areas for growth in the next six months as evolving their offering (33%), investing in their teams (29%) and entering new markets (27%).

The Business Barometer, which questions 1,200 businesses monthly, provides early signals about UK economic trends both regionally and nationwide.

A net balance of 16% of Scottish businesses expect to reduce staff levels over the next year, down two points on last month.

Overall UK business confidence fell one point during October to 15%, in line with the average over the last three months. Firms’ outlook on their future trading prospects was up two points to 27%, and a net balance of 21% are planning to create new jobs, up four points on last month. However, businesses optimism in the wider economy dropped three points to 2%.

Five UK regions and nations recorded a month-on-month increase in optimism in October. Of those, London (up 16 points to 49%), the North West (up 14 points to 28%) and Wales (up nine points to 5%) saw the largest monthly increases, with London remaining the most optimistic region overall.

Chris Lawrie, area director for Scotland at Bank of Scotland, said: “Ongoing economic challenges, not least the cost of doing business, is hitting firms and we’re seeing this reflected in a less optimistic outlook.

“As we approach the busiest trading period of the year for many, businesses across the country need to prioritise maintaining a steady cashflow to remain resilient and be well-equipped for any opportunities to grow.

“After all, Christmas can be a frenetic and expensive time for businesses and their customers, so firms need to have a plan in place to manage this, as well as having some money aside to cover unexpected costs.

“We’ll remain by the side of Scottish businesses to help them continue to navigate the challenging market conditions and push for growth.”

Business confidence in the manufacturing sector fell for the fifth month in a row, to 13%, down 1 percentage point, the lowest confidence level since February 2021.

Confidence in the retail sector declined by 6 percentage points to 9%, while confidence in the services sector also fell to 16%, both the lowest levels since early 2021.

However, the construction sector saw a 10 percentage point rise to 20%, although this level still remains weaker than in the first half of the year.

Paul Gordon, Managing Director for SME and Mid Corporates, Lloyds Bank Commercial Banking, said:“While confidence has marginally decreased this month, this also comes at a time of great economic uncertainty. The fact that it has only fallen by 1% suggests that businesses are showing resilience.

“As we head into the winter months and price pressures continue, energy price increases will start to bite and we are seeing continued pressure on pay expectations.

“Businesses need to keep a watchful eye on costs to ensure they are in the best possible position to face any future headwinds. For businesses that may be struggling, we encourage them to reach out to their networks for support. At Lloyds Bank we remain by the side of businesses to help navigate these challenging times.”

Hann-Ju Ho, senior economist for Lloyds Bank Commercial Banking, said: “While business confidence has marginally fallen this month, along with a drop in forward looking economic optimism, it is encouraging to see businesses still looking to increase their headcounts.

“However, cost pressures remain evident as businesses raise prices to protect their margins and wage pressure continue to be impactful. Given the recent turbulence in financial markets, it will be interesting to see how this will affect business confidence.”

A new report by Westminster’sinfluential Business, Energy and Industrial Strategy Committee has urged the Government to publish a draft Digital Markets Bill that would help deter predatory practices by big tech firms ‘without delay’.

Proposals for a Digital Markets Competition and Consumer Bill were trailed by the Government in the Queen’s Speech. It announced measures that would empower the Competition and Markets Authority’s (CMA) Digital Markets Unit (DMU) to rein in abusive tech giants by dropping the turnover threshold for immunity from financial penalties from £50 million to £20 million, and hiking potential maximum fines to 10% of global annual income.

The Committee concluded that fines have been viewed as ‘a small business cost’ by large companies, adding that there is ‘strong evidence of abuses of market dominance’ within digital markets. It warned that ‘consumers and others are at risk’ until a Bill is published and passed.

BEIS Committee Chair Darren Jones said: “The Competition, Consumer and Digital Markets Bill has wide support and should be prioritised, especially given the difficulty the Government currently has at passing other laws which are more controversial.

“There are many areas in the economy where stronger competition is required in the interests of consumers, small business and economic growth and this bill is an essential stepping stone to driving this issue forward.”

The report also called on the Government to ‘end [the] uncertainty’ caused by its failure to publish final guidance on the post-Brexit subsidy control regime, which the Committee found had left subsidy awarding bodies ‘in limbo’. The guidance needs to be published as soon as possible, MPs said.

Passed in April, and due to come into full force in early January, the Subsidy Control Act omits key details of the regime for public authorities to follow when awarding money. These gaps are due to be filled in by final guidance, which authorities will need if they are to have confidence when preparing bids for funding from the Shared Prosperity Fund. The Fund is a replacement for money formerly awarded through EU structural funding.

Mr Jones added: “The Government promised to replace previous EU funding into projects across the country as part of its Brexit and levelling up offers to the public. This has not yet been delivered and without full guidance and proper financing of the new subsidy schemes, funds that help deliver projects will be further delayed.

“The public will no doubt be disappointed to have not yet seen the so called ‘Brexit opportunities’ that were promised to level up their local community.”

Monday morning seems like an age ago, and the political circus is likely to continue into next week (writes Fraser of Allander Institute’s MAIRI SPOWAGE).

On Monday, the new chancellor undid pretty much every tax measure in the ex-Chancellor and soon-to-be ex-PM’s “mini”-budget. Only those already legislated for will proceed (the scrapping of the health and social care levy and the stamp duty cuts in England will still happen).

Although the PM has resigned, it still looks like the Fiscal Plan will be presented on 31st October, which is an interesting political situation given that presumably means that Jeremy Hunt will remain as Chancellor whoever wins the leadership election over the next week. But perhaps the last wee while has taught us that presuming anything is foolish!

For Scotland, the extra funding that was going to be generated by these tax measures for the Scottish Budget has now largely disappeared, with only the stamp duty reductions generating additional funding for Scotland.

This presents significant challenges for the Deputy First Minister in managing an already very stretched budget.

Economic Case for Independence published

Somewhat overshadowed by events at Westminster, the Scottish Government published the third in their series of papers to set out a new case for independence on Monday. This paper, “A stronger economy with independence” was expected to set out the economic case, covering issues such as currency, trade, and public sector finances.

We published analysis of the paper on Monday – and look out for our Guide to the Economics of Independence which we’ll be publishing soon and updating as more information is released by the Scottish Government.

Inflation goes back above 10%

The Office for National Statistics (ONS) published September inflation data, which showed that CPI inflation had gone back into double digits, running at 10.1%.

Underneath the headline rate, food and non-alcoholic beverages inflation is now estimated to be 13.1%. There was a slight downward pressure from motor fuels, as the prices at the pumps fall back from the peaks they reached in July.

These data still do not capture the energy price rises households are now experiencing as of 1st October, so expect there to be further increases in the rate when that data is published next month.

Interestingly (well, if you are interested in economic statistics, come on!) it may be that the change in the way the government is supporting households on energy may change the outlook for inflation. If, as is expected, the help after April is more targeted as cash transfers to those households most in need, then this will not put downward pressure on the actual price of energy.

We’ll be looking out for the OBR and Bank of England’s (3rd November) view on the pathway for inflation given these changes.

New Public Sector Finance Data published this morning (Friday)

ONS have also put out the latest public sector finances release, which contains public finance statistics (including deficit and debt) up to September 2022.

These have the first statistics on revenue generated by the Energy Profits Levy, which shows that £2.7 billion was generated from this tax in the year to date. It will be interesting to get the OBR’s independent view of the likely take from this tax over the next few years – and obviously to see if the Chancellor chooses to extend this in some way in the Fiscal Statement.

More broadly, it contains up-to-date statistics on the size of the UK National Debt. Debt has reached £2.5 trillion, which is equivalent to 98% of GDP – levels not seen since the 1960s.

This reminds us of the challenging fiscal environment, which sets the backdrop for the statement by the Chancellor in 10 days time.

No confirmation on the Scottish Government’s Emergency Budget Review

As we write this, we have no confirmation whether the Scottish Government’s Emergency Budget Review (EBR) will go ahead next week, as previously indicated.

Remember, this review is to look at in-year (2022-23) spending to balance the budget in the face of higher than expected (at the time of the last budget) inflationary pressures, particularly in relation to the public sector pay bill.

We wrote yesterday about employability support, one of the areas that John Swinney has already indicated will be cut. A number of questions remain to be answered. and we hope the EBR will be clear in laying out the evidence considered when deciding where the axe will fall.

The response to whatever is set out by the UK Chancellor on the 31st October will come in the Scottish Government’s draft budget for 2023-24 on the 15th December. For fiscal fans, the fun is due to continue for some months yet!

New research from insolvency and restructuring trade body R3 reveals Scottish firms had almost 1.7 million overdue invoices on their books in the last quarter.

R3’s analysis of data provided by Creditsafe shows 1,696,445 invoices were overdue in Scotland in Q3 – an increase of 7.1% from Q2’s total of 1,583,353.

Scotland and the West Midlands saw the biggest quarter-on-quarter rise in overdue invoices across the UK, followed by Northern Ireland (6.9% increase), the East Midlands (5.4%) and East Anglia (5.2%).

And Scottish businesses’ debt burden has been increasing steadily since the beginning of the year, rising from 552,897 unpaid bills in July, to 564,375 in August and 579,173 in September.

Almost 101,500 Scottish businesses reported that they had late payments on their books in Q3 2022 – a figure which peaked at 33,936 firms in September.

Richard Bathgate, Chair of insolvency and restructuring trade body R3 in Scotland, says: “This research highlights late payment is a growing issue in Scotland, and would suggest that businesses are facing ongoing cash-flow challenges, whether that’s supplier or client side …

“For small businesses that rely on regular income, even if just one client fails to pay or there is a delay in payment, that can have a serious effect – and in some cases, may mean they become financially distressed or insolvent.”

Richard, who is Restructuring Partner at Johnston Carmichael in Aberdeen continues: “I would urge the directors of any businesses who are worried about the impact of late payments or are worried about their ability to pay their invoices to seek professional advice.

“There are many steps that can be taken to support businesses, but they can only be taken if you move quickly and act early before the issue spirals.”

A major new survey of small and medium-sized businesses across the UK has shown a dramatic dip in confidence amidst rising inflation and wider economic turbulence.

The Be the Business Productive Business Index (PBI), now in its fifth edition, shows business owners and directors forecasting a negative shift in their prospects over the next three months due to the difficult economic environment.

The Productive Business Index, unique amongst UK business surveys, tracks changes in five key areas of business activity shown to impact on productivity. Management capability; Technology adoption; Training, Development and HR; Operating efficiency; and Innovation.

Key findings include:

The first-ever negative change in headline figure since the Index launched;

Two in five businesses are seeking efficiencies as a direct result of inflation;

Business leaders feel less confident that they have the management skills to handle the current economic situation, but are fighting back with plans to improve

Anthony Impey MBE, CEO of Be the Business, said: “These findings tell a stark story – following two years of unprecedented challenge, many businesses are struggling to cope with the latest turbulence in the UK economy.

“For the first time ever, our Productive Business Index shows a decrease in the optimism and outlooks of business leaders. Having been through the challenges of the pandemic and the ongoing supply chain and workforce issues, it highlights how heavily the economic situation is weighing on them.

“The headline figures are concerning, but it’s encouraging to see more leaders digging deep and looking for ways to improve themselves and their business to help navigate the next year. Business owners are tired, but they’re being forced to pedal harder in response to the difficult conditions they’re facing. It’s vitally important that they’re given all the support they need so that improving their business and boosting productivity is as easy as possible.”

The Be the Business’ Productive Business Index’s headline score, running from 0 to 200, decreased for the first time this quarter, from 121.1 to 115.6, indicating a fall in the productivity of firms.

In response to inflation, two-fifths (38%) of business leaders are planning to respond by finding efficiencies, one quarter (26%) will prioritise growth opportunities, and about one in six (15%) are considering reducing headcount to help their business survive.

Despite fighting through the previous two years of ups and downs, business outlook has fallen for the first time since Q4 2020, with half (50%) of leaders not confident in their business’ ability to respond to sustained inflation.

However, leaders are increasingly looking to improve their businesses and performance as they look to survive these new challenges.

Beneath the figures: Bruised UK firms are still looking to improve in the face of decreasing confidence

The consistent pressure on business leaders over the last several years – from the pandemic through to supply chain issues and now the escalating cost of living crisis – appears to have had a negative impact on them.

Business leaders feel less confident in their management skills as they look to navigate an increasingly challenging autumn and winter.

While belief in capabilities is down, business leaders continue to respond positively, by looking to bolster their skills as managers and invest time and money in their business over the next year:

Over half (56%) of UK business leaders believe their management teams have the right blend of skills, an 8% decrease from Q1 2022.

However, determination and the drive to improve shine through, with 45% expecting to spend more time on management and leadership activities – a 9% increase in only 6 months.

Just 54% of business leaders believe they have the skills and talent needed to succeed, a 10% decrease from Q1 2022

But 4 in 10 (40%) have plans to reassess pay, rewards and incentives to improve employee motivation, an increase of 8% on the last PBI.

There has been a significant drop (9%) in the number of business leaders that feel their company fosters innovation and new ideas from employees.

Yet, 41% of business leaders plan to develop new ideas, an increase of 7% compared to the beginning of the year.

The contrast between lower confidence and intent to improve is striking in the data on capabilities, and demonstrates the determination from business leaders to succeed in spite of the volatile economic context.

THIS week the government replaced one catastrophic plan with another (writes TUC’s GEOFF TILY). A new course to placate financial markets is traded off against likely massive hits to household budgets and fears about the future.

Support for energy bills was cut, public services already stretched beyond breaking point will be hit again, little was offered on soaring borrowing and mortgage costs, and nothing about already deeply inadequate benefits and universal credit falling further behind inflation.

There is another way to deliver an economy that works for working people, but the government couldn’t be further from it,

Dealing with failure

The Truss government were right about one thing, the economic policies of the past decade and more have been a disastrous failure. As Kwasi Kwarteng admitted, growth has been ‘anaemic’. In the ONS words: the UK is the only G7 economy yet to recover above its pre-coronavirus pandemic level in Quarter 4 2019. The UK has the lowest investment as a share of GDP (see our ‘companies for the people report’, Figure 7) In Spring OECD figures showed UK real wages would fall furthest of all G7 economies.

Mini budget catastrophe

But the mini budget was catastrophically wrongheaded. Truss and Kwarteng took the fundamental problem of an economy serving wealth not work and turned it into the solution. The flip side of support for energy bills, was lavish tax breaks for those least in need – under the spurious and long discredited fallacy of ‘trickle down’.

On top of this their intention was to borrow to fund this extreme project. They did so the day after the Bank of England had confirmed that they would be reducing support for government borrowing, and implementing a £80billon programme of ‘quantitative tightening’ [i.e. selling back government bonds to financial markets] from the start of October. (Regardless of anything else this revealed staggering lack of coordination on the part of both institutions – the excellent Daniella Gabor called this ‘uncoordinated class war on the British public’.)

Financial markets took fright and instead of buying started to dump government debt, but this was also intimately connected to a third factor. The complex financial strategies – so-called liability driven investments (LDI) – that pension funds have been deploying (unnoticed by most) for the past 20 years began to unravel in the face of these rate rises.

The Bank of England was obliged to step in to halt a vicious cycle – or doom loop – of bond sales leading to higher interest rates and so more bond sales. The spike in the chart below of interest rates on UK 30-year bonds shows how the episode was at least momentarily brought under control.

And in the meantime the government came under sustained assault for ‘fiscal irresponsibility’.

U-turn to a worse economy

After two U-turns (on the 45p top rate and corporation tax reductions), yesterday they U- turned on pretty much the whole thing.

But reversing a wrong doesn’t make a right, far from it.

We are now on the brink of a deep and damaging recession that threatens millions of jobs. But the latest Conservative chancellor has now announced the same basic approach that got us into this mess.

He warned of “more difficult decisions” on tax and spending to come. And immediately that “Some areas of spending will need to be cut”.

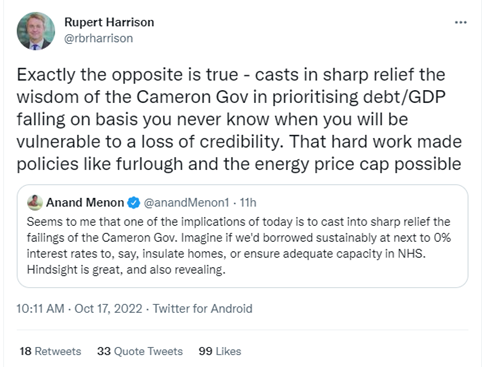

The Chancellor not only announced austerity. He not only sought once more – as did his George Osborne – to make a political virtue about imposing misery. He even invited George Osborne’s favourite adviser Rupert Harrison (now at Blackrock, one of three key institutions in LDI strategies) back to the Treasury to head a new panel of ‘economic advisers’ to deliver this reborn monstrosity.

Yesterday morning Rupert gave his City-oriented perspective on austerity

But this is a seriously misleading statement. The Osborne government did not repair the public finances. Over 2010-2019 the public debt ratio increased by 22 percentage point of GDP – the worse performance over a decade of economic recovery for a century (here).

For workers, this meant the worst pay crisis for 200 years. As Frances O’Grady spells out today, now expected (and this was before yesterday) to last at least two decades.

But the context for policy today is even more worrying than in 2010. Central banks, led by the Federal Reserve in the United States, are engaged in a forceful (their word) tightening of monetary policy.

This amounts to ending a strategy that has been in place since the start of the global financial crisis. In the wake of the last increase to 3.0 to 3.25 per cent, a Fed committee member has pointed to rates at up to 4.5 to 5 per cent. Fear of the impact of these rate rises on mortgage rates is likely common to all countries – for example in the US rates on a 30-year mortgage are up from 2.7 per cent at the start of 2021 to 6.9 per cent now.

And while in the UK the spike was brought under control, government interest rates are still seriously elevated and will carry on feeding through to mortgages.

In the UK money expert Martin Lewis has offered a grim rule of thumb: “For each 1 percentage point your mortgage rate increases, expect to pay roughly £50 more a month (£600/year) per £100,000 of mortgage debt.” The Resolution Foundation reckoned five million families would see annual payments rising by an average of £5,000 between now and the end of 2024.

Standing further back, the Financial Stability Board (Dietrich Domanski on the Today programme, 6 Oct.) have warned of the challenges of raising interest rates to deal with inflation under the conditions of the high global indebtedness that prevail today.

Likewise the IMF last week warned of “hidden leverage”, “waves of deleveraging”, and in particular the risk to ‘non-bank financial institutions’ – the latter including pension funds.

In terms of countries, first in the firing line are emerging market economies – with 20 countries “in default or trading at distressed levels”.

While the immediate trigger for central bank policies is the inflation set in motion by the end of lockdowns and Putin’s brutal invasion of Ukraine, the scale of the dislocation reflects a wider failure to set the economy right since the global financial crisis of 2008-09 exposed deep underlying failings. Summing up, the IMF offered the chilling: “the level of risk we are flagging at the moment is the highest outside acute crisis”

As the Biden administration has argued, for 40 years the interests of wealth have been prioritised over those of workers. The economy crashed in the first place because these financial interests proved wildly at odds with the interests of the population as a whole. An economy of speculation and debt crowded out production and decent pay and work.

The chancellor’s new advisory panel puts these interests back front and centre of policymaking at the Treasury. The other members so far announced are also from the City of London, not least securing J.P. Morgan a seat at the table.

Yesterday the Financial Times reported that the Bank of England’s programme of quantitative tighten has been put on hold, likely to protect the casino capitalism around pension funds.

Ahead of the mini budget the TUC issued a plan for a budget ‘on the side of working people’. We desperately need a government that will put first our interests not those of wealth. But instead once more the interests of the city of London are put ahead of those of workers and the country.

A new single rate for the national minimum wage to reflect the increased cost of living, and more effective employment law to protect workers’ rights underpin plans to build a fairer labour market in an independent Scotland, according to Deputy First Minister John Swinney.

Following publication of the paper Building a New Scotland: A stronger economy with independence, Mr Swinney said the powers of independence would allow the Scottish Government to build a fairer, more equal future for all workers. This includes new measures to improve access to flexible working and better industrial relations.

Deputy First Minister John Swinney said: “Improving job security, wages and work-life balance are essential to delivering a more socially just Scotland. The UK labour market model has generated high income inequality while failing to drive productivity growth.

“Compared to independent European countries similar to Scotland, the UK has a higher prevalence of low pay, a bigger gender pay gap, longer working hours and significantly lower statutory sick pay.

“The Scottish Government is committed to Fair Work, but we could go much further to strengthen that agenda in an independent Scotland, developing a legal framework that more effectively addresses the workplace challenges of the 21st century. It would give us an opportunity to redesign the system to better meet the needs of Scotland’s workers and employers.”

Specific measures proposed in the paper include:

establishing a Scottish Fair Pay Commission to lead a new approach to setting a national minimum wage, working with employers, trade unions and government

improving pay and conditions with a single rate minimum wage for all age groups and better access to flexible work to help parents and carers

repealing the UK Trade Union Act 2016 as part of developing an approach to industrial relations which suits both workers and employers

introducing a law to help workers organise co-operative buyouts or rescues when a business is up for sale or under threat

legislating to support workers in precarious employment, and banning the practice of staff being made redundant and re-hired on reduced wages and conditions

increasing transparency in pay reporting and data to address gender, ethnicity and disability pay gaps and building on Scottish Government work to break down barriers to employment

The paper outlines how it would be easier for an independent Scotland to deal with labour market shocks.

In responding to the global financial crisis and pandemic, other countries were able to quickly draw on existing institutions and initiatives. This could include a permanent short-time working scheme, modelled on the German Kurzarbeit programme which provides compensation for private sector workers whose hours are reduced because of economic difficulty. A scheme like this in Scotland could help retain skills, reduce long-term unemployment and the associated costs and allow for more rapid economic recovery.

Job Security Councils, modelled on a Swedish initiative, could provide support to workers who have lost – or are at risk of losing – their jobs. These non-profit foundations led by social partners, employer representative bodies and trades unions, would help workers find new employment by providing a range of advice and high-quality retraining.

{kind=link}

{kind=link}