Liz Truss has given her final speech as Prime Minister on the steps of Downing Street:

It has been a huge honour to be Prime Minister of this great country.

In particular, to lead the nation in mourning the death of Her Late Majesty The Queen after 70 years of service,

and welcoming the accession of His Majesty King Charles III.

In just a short period, this government has acted urgently and decisively on the side of hardworking families and businesses.

We reversed the National Insurance increase.

We helped millions of households with their energy bills and helped thousands of businesses avoid bankruptcy.

We are taking back our energy independence…

…so we are never again beholden to global market fluctuations or malign foreign powers.

From my time as Prime Minister, I am more convinced than ever we need to be bold and confront the challenges that we face.

As the Roman philosopher Seneca wrote: “It is not because things are difficult that we do not dare. It is because we do not dare that they are difficult.”

We simply cannot afford to be a low growth country where the government takes up an increasing share of our national wealth…

and where there are huge divides between different parts of our country.

We need to take advantage of our Brexit freedoms to do things differently.

This means delivering more freedom for our own citizens and restoring power in democratic institutions.

It means lower taxes, so people keep more of the money they earn.

It means delivering growth that will lead to more job security, higher wages and greater opportunities for our children and grandchildren.

Democracies must be able to deliver for their own people…

We must be able to outcompete autocratic regimes, where power lies in the hands of a few.

And now more than ever we must support Ukraine in their brave fight against Putin’s aggression.

Ukraine must prevail.

And we must continue to strengthen our nation’s defences.

That is what I have been striving to achieve… and I wish Rishi Sunak every success, for the good of our country.

I want to thank Hugh, Frances, Liberty, my family and friends, and all the team at No10 for their love, friendship and support.

I also want to thank my protection team.

I look forward to spending more time in my constituency, and continuing to serve South West Norfolk from the backbenches.

FORMER Prime Minister Boris Johnson issued the following statement last night:

Johnson’s final acceptance that the anticipated support just isn’t there for him clears the way for a run-off between hot favourite Rishi Sunak and Penny Mordaunt – but only if the latter can attract enough votes among her fellow Tory MPs. That’s looking increasingly unlikely.

If she can’t reach the 100 vote target, we can look forward to the anointing of Rishi Sunak as our new Prime Minister, with the Tory party membership having no say.

Monday morning seems like an age ago, and the political circus is likely to continue into next week (writes Fraser of Allander Institute’s MAIRI SPOWAGE).

On Monday, the new chancellor undid pretty much every tax measure in the ex-Chancellor and soon-to-be ex-PM’s “mini”-budget. Only those already legislated for will proceed (the scrapping of the health and social care levy and the stamp duty cuts in England will still happen).

Although the PM has resigned, it still looks like the Fiscal Plan will be presented on 31st October, which is an interesting political situation given that presumably means that Jeremy Hunt will remain as Chancellor whoever wins the leadership election over the next week. But perhaps the last wee while has taught us that presuming anything is foolish!

For Scotland, the extra funding that was going to be generated by these tax measures for the Scottish Budget has now largely disappeared, with only the stamp duty reductions generating additional funding for Scotland.

This presents significant challenges for the Deputy First Minister in managing an already very stretched budget.

Economic Case for Independence published

Somewhat overshadowed by events at Westminster, the Scottish Government published the third in their series of papers to set out a new case for independence on Monday. This paper, “A stronger economy with independence” was expected to set out the economic case, covering issues such as currency, trade, and public sector finances.

We published analysis of the paper on Monday – and look out for our Guide to the Economics of Independence which we’ll be publishing soon and updating as more information is released by the Scottish Government.

Inflation goes back above 10%

The Office for National Statistics (ONS) published September inflation data, which showed that CPI inflation had gone back into double digits, running at 10.1%.

Underneath the headline rate, food and non-alcoholic beverages inflation is now estimated to be 13.1%. There was a slight downward pressure from motor fuels, as the prices at the pumps fall back from the peaks they reached in July.

These data still do not capture the energy price rises households are now experiencing as of 1st October, so expect there to be further increases in the rate when that data is published next month.

Interestingly (well, if you are interested in economic statistics, come on!) it may be that the change in the way the government is supporting households on energy may change the outlook for inflation. If, as is expected, the help after April is more targeted as cash transfers to those households most in need, then this will not put downward pressure on the actual price of energy.

We’ll be looking out for the OBR and Bank of England’s (3rd November) view on the pathway for inflation given these changes.

New Public Sector Finance Data published this morning (Friday)

ONS have also put out the latest public sector finances release, which contains public finance statistics (including deficit and debt) up to September 2022.

These have the first statistics on revenue generated by the Energy Profits Levy, which shows that £2.7 billion was generated from this tax in the year to date. It will be interesting to get the OBR’s independent view of the likely take from this tax over the next few years – and obviously to see if the Chancellor chooses to extend this in some way in the Fiscal Statement.

More broadly, it contains up-to-date statistics on the size of the UK National Debt. Debt has reached £2.5 trillion, which is equivalent to 98% of GDP – levels not seen since the 1960s.

This reminds us of the challenging fiscal environment, which sets the backdrop for the statement by the Chancellor in 10 days time.

No confirmation on the Scottish Government’s Emergency Budget Review

As we write this, we have no confirmation whether the Scottish Government’s Emergency Budget Review (EBR) will go ahead next week, as previously indicated.

Remember, this review is to look at in-year (2022-23) spending to balance the budget in the face of higher than expected (at the time of the last budget) inflationary pressures, particularly in relation to the public sector pay bill.

We wrote yesterday about employability support, one of the areas that John Swinney has already indicated will be cut. A number of questions remain to be answered. and we hope the EBR will be clear in laying out the evidence considered when deciding where the axe will fall.

The response to whatever is set out by the UK Chancellor on the 31st October will come in the Scottish Government’s draft budget for 2023-24 on the 15th December. For fiscal fans, the fun is due to continue for some months yet!

Following the news about the closure of the Modern Two art gallery in Edinburgh until next year due to rising energy bills, Sarah Boyack MSP, Scottish Labour’s Spokesperson for Culture and MSP for Lothian, highlighted the wider issues the sector is facing and called on the Scottish Government to deliver urgent action.

The Scottish Labour MSP commented: “Our arts and culture organisations are on the brink of collapse – many are fighting for survival, they are struggling to cope with the perfect storm of reduced incomes, skyrocketing energy bills and inflation.

“Earlier this month, we found out that Falkirk Town Hall, the Filmhouse in Edinburgh, the Belmont in Aberdeen and the Edinburgh International Film Festival have all gone under.

“The Scottish Government reassured us that Scotland’s National Collections will remain open to the public free of charge. However, the reality on the ground tells us a very different story.

“Instead of rhetoric and empty promises, we need the Government to deliver the urgent action the arts and culture sector needs at this moment of crisis.”

In his written response to Sarah Boyack MSP, on 30th September, Culture Secretary Neil Gray said: “the National Collections are an important part of Scotland’s culture.

!”As part of setting and reviewing annual budgets for grant in aid, the Scottish Government maintains close contact with National Museums Scotland and the National Galleries of Scotland about their cost and revenue, in order to continue to ensure that their permanent collections remain open to the public free of charge.”

PRIME Minister Liz Truss has resigned after just six weeks in post.

Truss, who yesterday declared she was ‘a fighter, not a quitter’, has, well, quit after just 45 days in the job.

Her resignation statement was equally short:

I came into office at a time of great economic and international instability.

Families and businesses were worried about how to pay their bills.

Putin’s illegal war in Ukraine threatens the security of our whole continent.

And our country had been held back for too long by low economic growth.

I was elected by the Conservative Party with a mandate to change this.

We delivered on energy bills and on cutting national insurance.

And we set out a vision for a low tax, high growth economy – that would take advantage of the freedoms of Brexit.

I recognise though, given the situation, I cannot deliver the mandate on which I was elected by the Conservative Party.

I have therefore spoken to His Majesty The King to notify him that I am resigning as Leader of the Conservative Party.

This morning I met the Chair of the 1922 Committee Sir Graham Brady.

We have agreed there will be a leadership election to be completed in the next week.

This will ensure we remain on a path to deliver our fiscal plans and maintain our country’s economic stability and national security.

I will remain as Prime Minister until a successor has been chosen.

Thank you.

Scotland’s First Minister Nicola Sturgeon tweeted:”There are no words to describe this utter shambles adequately. It’s beyond hyperbole – & parody. Reality tho(ugh) is that ordinary people are paying the price.

“The interests of the Tory party should concern no-one right now. A General Election is now a democratic imperative.”

Labour leader Sir Keir Starmer said: “After 12 years of Tory failure, the British people deserve so much better than this revolving door of chaos. We need a general election, now.”

His full statement:

Truss will remain as PM until her successor is elected – not by the people of Great Britain, but by Tory MPs.

THIS week the government replaced one catastrophic plan with another (writes TUC’s GEOFF TILY). A new course to placate financial markets is traded off against likely massive hits to household budgets and fears about the future.

Support for energy bills was cut, public services already stretched beyond breaking point will be hit again, little was offered on soaring borrowing and mortgage costs, and nothing about already deeply inadequate benefits and universal credit falling further behind inflation.

There is another way to deliver an economy that works for working people, but the government couldn’t be further from it,

Dealing with failure

The Truss government were right about one thing, the economic policies of the past decade and more have been a disastrous failure. As Kwasi Kwarteng admitted, growth has been ‘anaemic’. In the ONS words: the UK is the only G7 economy yet to recover above its pre-coronavirus pandemic level in Quarter 4 2019. The UK has the lowest investment as a share of GDP (see our ‘companies for the people report’, Figure 7) In Spring OECD figures showed UK real wages would fall furthest of all G7 economies.

Mini budget catastrophe

But the mini budget was catastrophically wrongheaded. Truss and Kwarteng took the fundamental problem of an economy serving wealth not work and turned it into the solution. The flip side of support for energy bills, was lavish tax breaks for those least in need – under the spurious and long discredited fallacy of ‘trickle down’.

On top of this their intention was to borrow to fund this extreme project. They did so the day after the Bank of England had confirmed that they would be reducing support for government borrowing, and implementing a £80billon programme of ‘quantitative tightening’ [i.e. selling back government bonds to financial markets] from the start of October. (Regardless of anything else this revealed staggering lack of coordination on the part of both institutions – the excellent Daniella Gabor called this ‘uncoordinated class war on the British public’.)

Financial markets took fright and instead of buying started to dump government debt, but this was also intimately connected to a third factor. The complex financial strategies – so-called liability driven investments (LDI) – that pension funds have been deploying (unnoticed by most) for the past 20 years began to unravel in the face of these rate rises.

The Bank of England was obliged to step in to halt a vicious cycle – or doom loop – of bond sales leading to higher interest rates and so more bond sales. The spike in the chart below of interest rates on UK 30-year bonds shows how the episode was at least momentarily brought under control.

And in the meantime the government came under sustained assault for ‘fiscal irresponsibility’.

U-turn to a worse economy

After two U-turns (on the 45p top rate and corporation tax reductions), yesterday they U- turned on pretty much the whole thing.

But reversing a wrong doesn’t make a right, far from it.

We are now on the brink of a deep and damaging recession that threatens millions of jobs. But the latest Conservative chancellor has now announced the same basic approach that got us into this mess.

He warned of “more difficult decisions” on tax and spending to come. And immediately that “Some areas of spending will need to be cut”.

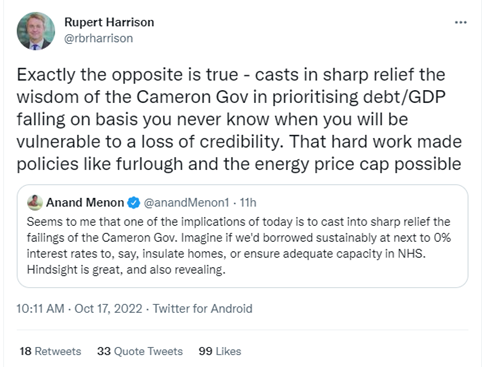

The Chancellor not only announced austerity. He not only sought once more – as did his George Osborne – to make a political virtue about imposing misery. He even invited George Osborne’s favourite adviser Rupert Harrison (now at Blackrock, one of three key institutions in LDI strategies) back to the Treasury to head a new panel of ‘economic advisers’ to deliver this reborn monstrosity.

Yesterday morning Rupert gave his City-oriented perspective on austerity

But this is a seriously misleading statement. The Osborne government did not repair the public finances. Over 2010-2019 the public debt ratio increased by 22 percentage point of GDP – the worse performance over a decade of economic recovery for a century (here).

For workers, this meant the worst pay crisis for 200 years. As Frances O’Grady spells out today, now expected (and this was before yesterday) to last at least two decades.

But the context for policy today is even more worrying than in 2010. Central banks, led by the Federal Reserve in the United States, are engaged in a forceful (their word) tightening of monetary policy.

This amounts to ending a strategy that has been in place since the start of the global financial crisis. In the wake of the last increase to 3.0 to 3.25 per cent, a Fed committee member has pointed to rates at up to 4.5 to 5 per cent. Fear of the impact of these rate rises on mortgage rates is likely common to all countries – for example in the US rates on a 30-year mortgage are up from 2.7 per cent at the start of 2021 to 6.9 per cent now.

And while in the UK the spike was brought under control, government interest rates are still seriously elevated and will carry on feeding through to mortgages.

In the UK money expert Martin Lewis has offered a grim rule of thumb: “For each 1 percentage point your mortgage rate increases, expect to pay roughly £50 more a month (£600/year) per £100,000 of mortgage debt.” The Resolution Foundation reckoned five million families would see annual payments rising by an average of £5,000 between now and the end of 2024.

Standing further back, the Financial Stability Board (Dietrich Domanski on the Today programme, 6 Oct.) have warned of the challenges of raising interest rates to deal with inflation under the conditions of the high global indebtedness that prevail today.

Likewise the IMF last week warned of “hidden leverage”, “waves of deleveraging”, and in particular the risk to ‘non-bank financial institutions’ – the latter including pension funds.

In terms of countries, first in the firing line are emerging market economies – with 20 countries “in default or trading at distressed levels”.

While the immediate trigger for central bank policies is the inflation set in motion by the end of lockdowns and Putin’s brutal invasion of Ukraine, the scale of the dislocation reflects a wider failure to set the economy right since the global financial crisis of 2008-09 exposed deep underlying failings. Summing up, the IMF offered the chilling: “the level of risk we are flagging at the moment is the highest outside acute crisis”

As the Biden administration has argued, for 40 years the interests of wealth have been prioritised over those of workers. The economy crashed in the first place because these financial interests proved wildly at odds with the interests of the population as a whole. An economy of speculation and debt crowded out production and decent pay and work.

The chancellor’s new advisory panel puts these interests back front and centre of policymaking at the Treasury. The other members so far announced are also from the City of London, not least securing J.P. Morgan a seat at the table.

Yesterday the Financial Times reported that the Bank of England’s programme of quantitative tighten has been put on hold, likely to protect the casino capitalism around pension funds.

Ahead of the mini budget the TUC issued a plan for a budget ‘on the side of working people’. We desperately need a government that will put first our interests not those of wealth. But instead once more the interests of the city of London are put ahead of those of workers and the country.

Responding to the latest figures showing the Royal Infirmary of Edinburgh sees only 40.6% of A&E patients within 4 hours, Foysol Choudhury MSP said:“The figures for patients being seen at A&E within 4 hours in Edinburgh remain alarmingly low, even before the anticipated winter crisis hits.

“The Cabinet Secretary for Health has said that ‘recovery from Covid will not happen overnight’, but we are yet to see any evidence of recovery at all. The 4-hour figures for NHS Lothian last averaged above 90% in March 2021, while the figures for Edinburgh Royal last averaged above 90% in October 2020. The trend has been downwards since then.

“Hard-working NHS staff are doing their best for patients in very difficult circumstances, but they are being let down by long-running structural failures which remain unresolved by this SNP-Green government.

“The Scottish Government needs to take urgent action now to arrest two years of decline in our health service, or risk putting patient safety in jeopardy over winter.”

The Scottish Conservatives said: “This week, A&E waiting time figures showed 1506 patients waiting more than half a day in emergency departments.

“Hardworking NHS staff are being pushed beyond their limits and patients are suffering needlessly as a result of SNP inaction.”

Mr Yousaf said: “A&E departments are working under significant pressure and, in common with other healthcare systems across the UK and globally, the pandemic continues to impact performance.

“Recovery from Covid will not happen overnight, which is why we are continuing to work with boards on a number of measures to reduce pressure this winter.”

Statement from Chancellor of the Exchequer, Jeremy Hunt:

Chancellor of the Exchequer, Jeremy Hunt said:“My focus is on growth underpinned by stability. The drive on growing the economy is right – it means more people can get good jobs, new businesses can thrive and we can secure world class public services. But we went too far, too fast.

“We have to be honest with people and we are going to have to take some very difficult decisions both on spending and on tax to get debt falling but the top of our minds when making these decisions will be how to protect and help struggling families, businesses and people.

“I will set out clear and robust plans to make sure government spending is as efficient as possible, ensure taxpayer money is well spent and that we have rigorous control over our public finances.”

CHANCELLOR Kwasi Kwarteng has been sacked, carrying the can for the ill-judged ‘mini-budget’ which has caused economic turmoil since it was announced three weeks ago today.

‘I’m going nowhere’ Kwarteng, Prime Minister Liz Truss’s choice as Chancellor, was recalled from an IMF meeting in Washington DC this morning to be told the news.

Prime Minister Liz Truss will desperately hope that the departure of close ally Kwarteng will appease the markets. She made the following brief statement confirming a humiliating U-turn this afternoon:

Good afternoon,

My conviction that this country needs to go for growth is rooted in my personal experience.

I know what it’s like to grow up somewhere that isn’t feeling the benefits of growth.

I saw what that meant and I am not prepared to accept that for our country.

I want a country where people can get good jobs, new businesses can set up and families can afford an even better life.

That’s why from day one I’ve been ambitious for growth.

Since the 2008 financial crisis, the potential of this great country has been held back by persistently weak growth.

I want to deliver a low tax, high wage, high growth economy.

It’s what I was elected by my party to do.

That mission remains.

People across this country rightly want stability.

That is why we acted to support businesses and households with their energy costs this winter.

It’s also the case that global economic conditions are worsening due to the continuation of Putin’s appalling war in Ukraine.

And on top of this, debt was amassed helping people through the Covid pandemic.

But it is clear that parts of our mini budget went further and faster than markets were expecting. So the way we are delivering our mission right now has to change.

We need to act now to reassure the markets of our fiscal discipline.

I have therefore decided to keep the increase in corporation tax that was planned by the previous government. This will raise £18 billion per year.

It will act as a down-payment on our full Medium-Term Fiscal Plan which will be accompanied by a forecast from the independent OBR.

We will do whatever is necessary to ensure debt is falling as a share of the economy in the medium term.

We will control the size of the state to ensure that taxpayers’ money is always well spent.

Our public sector will become more efficient to deliver world-class services for the British people.

And spending will grow less rapidly than previously planned.

I met the former Chancellor earlier today. I was incredibly sorry to lose him. He is a great friend and he shares my vision to set this country on the path to growth.

Today I have asked Jeremy Hunt to become the new Chancellor.

He is one of the most experienced and widely respected government ministers and parliamentarians.

And he shares my convictions and ambitions for our country.

He will deliver the Medium-Term Fiscal Plan at the end of this month.

He will see through the support we are providing to help families and businesses including our Energy Price Guarantee that’s protecting people from higher energy bills this winter.

And he will drive our mission to go for growth, including taking forward the supply side reforms that our country needs.

We owe it to the next generation to improve our economic performance to deliver higher wages, new jobs and better public services, and to ease the burden of debt.

I have acted decisively today because my priority is ensuring our country’s economic stability.

As Prime Minister, I will always act in the national interest.

This is always my first consideration.

I want to be honest, this is difficult. But we will get through this storm.

And we will deliver the strong and sustained growth that can transform the prosperity of our country for generations to come.

Kwarteng’s replacement – and the UK’s fourth Chancellor in a tumultuous 2022 – is none other than veteran former health secretary Jeremy Hunt.

Hunt supported Rishi Sunak – who’s predictions on the economy have been proved painfully accurate – in the recent Tory leadership election.

Hunt himself was an early casualty in the recent Tory leadership election and was also once voted as the most unpopular front-line politician of all time!

Clearly another popular choice … what could possibly go wrong?

HM Treasury issued the following statement this evening:

Government update on Corporation Tax

The Prime Minister has set out that the way the government is delivering on its mission to achieve a low tax, high wage, high growth economy is to change.

The legislated increase in the Corporation Tax rate from April 2023 will go ahead, with most small businesses benefitting from the new small profits rate.

Chancellor Jeremy Hunt will deliver the Medium-Term Fiscal Plan on 31 October, detailing action to get debt falling as a percentage of GDP over the medium term.

The government has today [Friday 14 October] announced that Corporation Tax will increase to 25% from April 2023 as already legislated for, raising around £18 billion a year and acting as a down payment on its full Medium-Term Fiscal Plan.

The decision has been taken in recognition of the need to ensure the UK’s economic stability and reassure markets of its commitment to fiscal discipline, after elements of September’s Growth Plan went further and faster than markets were expecting.

The Prime Minister has set out that the government is prepared to do whatever is necessary to ensure debt is falling as a share of the economy in the medium term and to ensure that taxpayers’ money is well spent, putting public finances on a sustainable footing.

The previously announced small profits rate of Corporation Tax will be maintained. Smaller or less profitable businesses will not pay the full 25% rate, and companies with less than £50,000 of profit – the large majority – will not see any increase at all, continuing to pay Corporation Tax at 19%.

The UK’s corporate tax regime will remain competitive and supportive of growth at the 25% rate, continuing to be the lowest rate in the G7. As part of the forthcoming tax review, the government will look at how the tax system can go further to promote growth and investment.

The government is committed to growing the economy and taking forward supply-side reforms that will ignite strong and sustained growth that delivers prosperity for the UK.

Chancellor of the Exchequer Jeremy Hunt will set out the government’s Medium-Term Fiscal Plan on 31 October, alongside a full forecast from the independent Office for Budget Responsibility.

Lorna Slater, the Scottish Greens MSP for Lothian has welcomed the Scottish Parliament’s vote to introduce a national rent freeze and new protections from evictions.

The measures in the Bill, which was introduced by a Scottish Green Minister, Patrick Harvie MSP, was overwhelmingly passed last week. It will provide vital protections for tenants over Winter and last until at least March 2023.

These changes will help tenants across Lothian where the average monthly rent is £942, which is an increase of 41.7% since 2010.

Lorna Slater, the Scottish Green MSP for Lothian said: “I am delighted that this Bill has been passed. These are vital changes that will make a huge difference at what is a desperate time for tenants all across Scotland.

“The measures in the Bill will provide stability and support for households and families across Lothian and beyond at a time when many are being hit by soaring costs and bills.

“These are the most progressive set of tenants’ rights anywhere in the UK. The legislation, which will last until at least the end of March 2023, puts Scotland at the forefront of tenants rights in the UK and sets a crucial precedent for other governments to follow.

“With Greens in the Scottish Government, we are leading the change and building a fairer, greener and better future for our communities.”

{kind=link}

{kind=link}