- Retired women have to struggle with £7,600 a year less than men on average.

- Women approaching retirement have only built up half as much in a workplace or private pension as men.

- More action needs to be taken to close the gap for women set to retire in the years ahead.

- The recent revival of the Pension Commission is a much-needed opportunity to ensure that in the future everyone receives a decent retirement income.

The gender pension gap in the UK means that retired women effectively go over four months each year without getting a pension – the equivalent of losing out on £7,600 a year on average.

This means that compared to men, retired women effectively stop receiving pension income from yesterday (Thursday 21 August), the TUC warns.

The income gap between men and women in retirement is now 36.5%, according to research from Prospect union – more than double the level of the gender pay gap (currently 13.1%).

Reasons for the gap

The TUC says that the main drivers of the gender pensions income gap are:

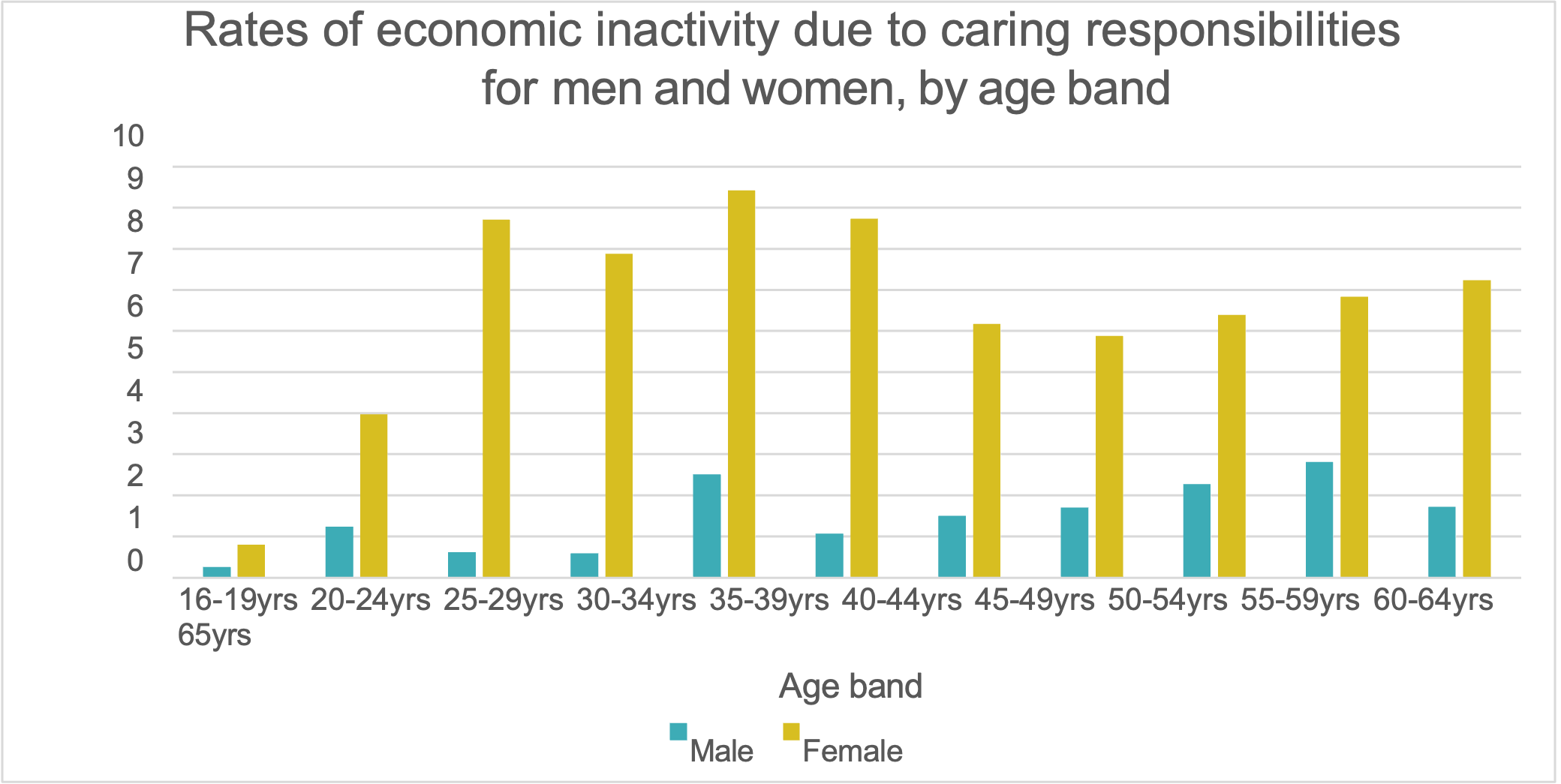

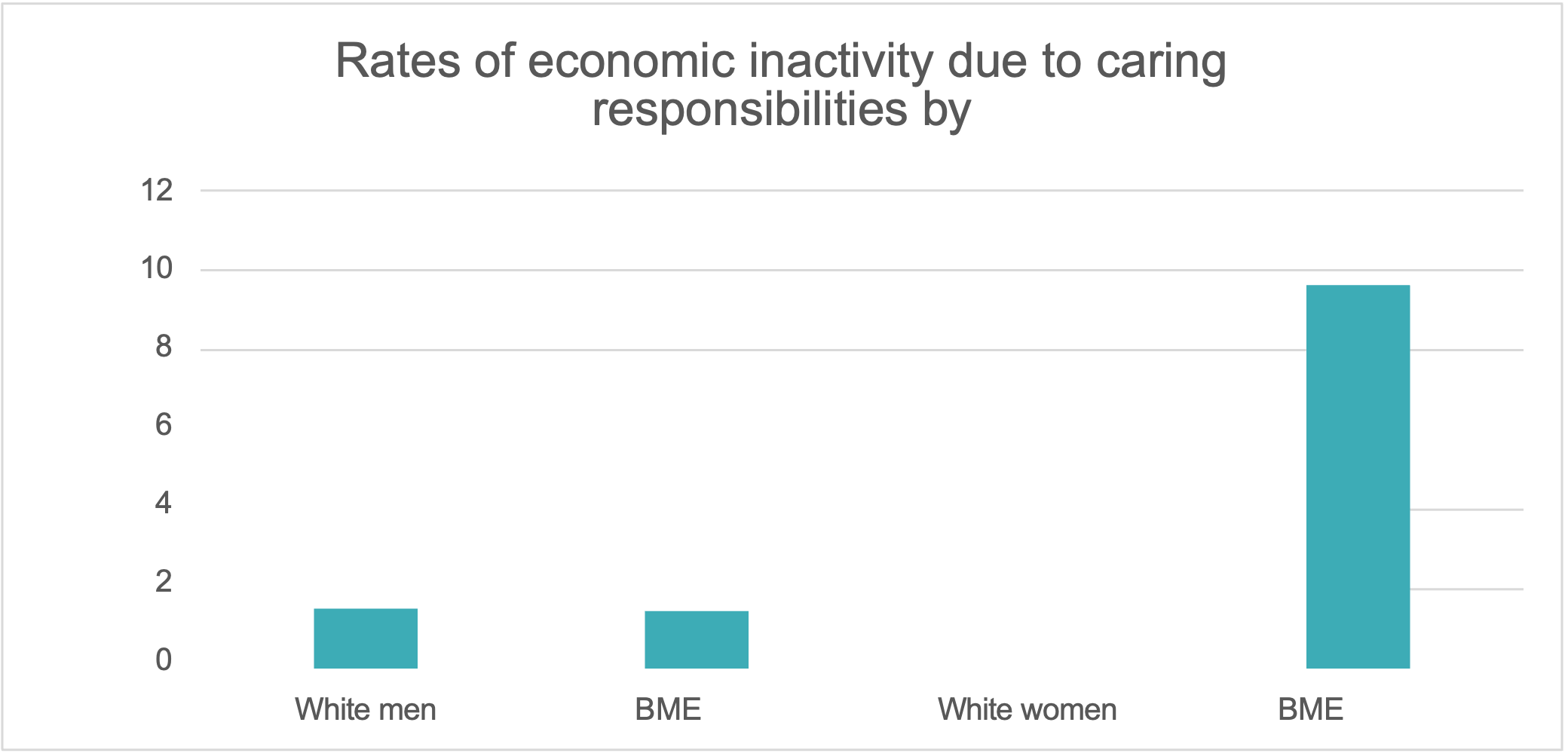

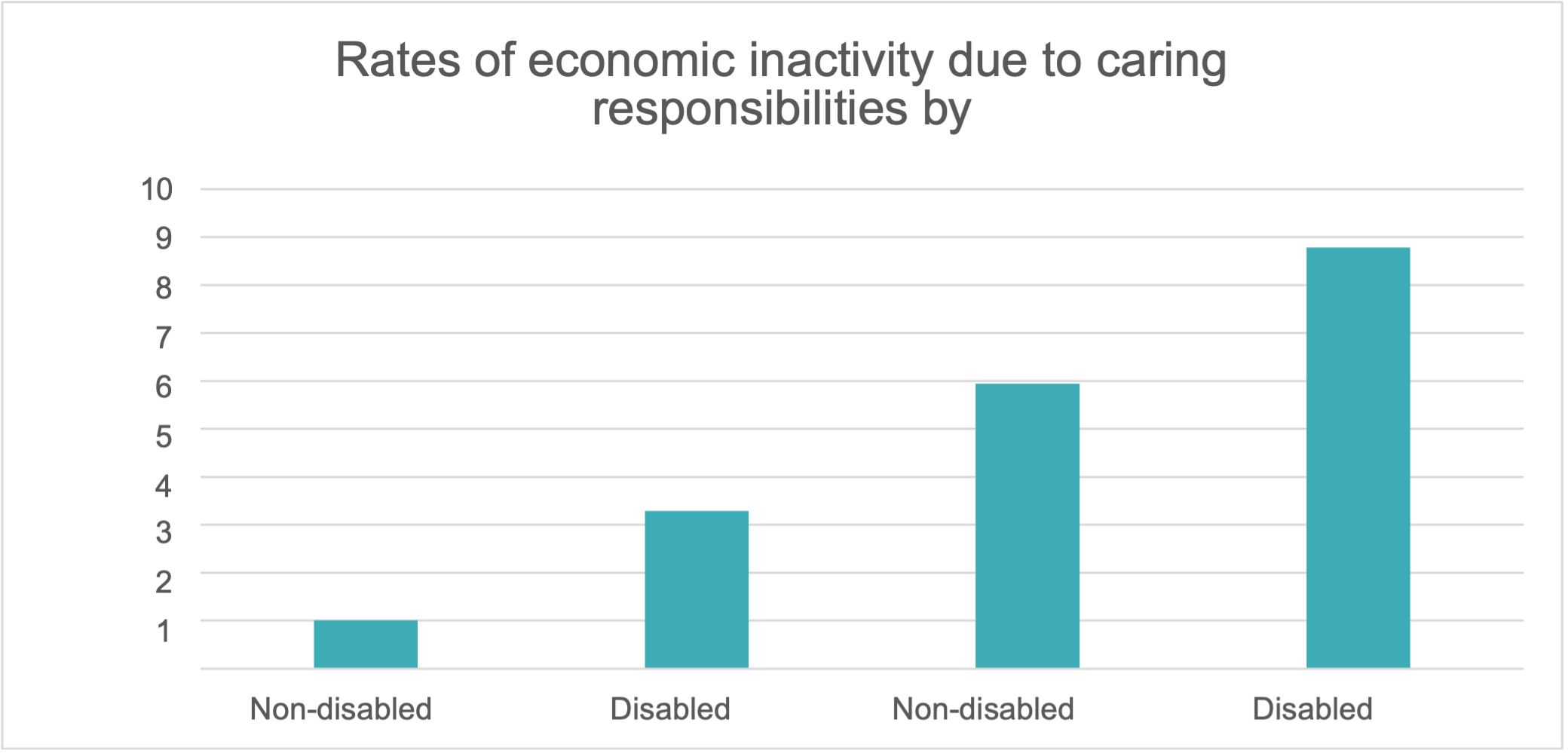

- Unpaid caring responsibilities: women are five times more likely than men to be out of paid work to look after children, elderly or disabled family members – missing out on workplace pension contributions as a result. BME and disabled women are among the worst impacted – respectively at seven and nine times more likely than White and non-disabled men to be out of work due to caring responsibilities.

- Gender pay gap: across their working lives, women persistently earn less than men and therefore accrue lower pension contributions. In particular, women are three times more likely than men to earn below £10,000 – the threshold for employers to have to put workers into a workplace pension.

- State pension: historic differences in state pension have left currently retired women with lower state pensions on average.

Lasting solutions

The TUC has highlighted three key solutions for narrowing the gender pension gap for women retiring in the future:

- Addressing the gender pay and employment gaps. This should include improving childcare and social care, continuing to strengthen rights to work flexibly as well as reforming the parental leave system to enable more equitable sharing of caring responsibilities. The Employment Rights Bill – which will introduce a right to request flexible working from day one of employment – and the Parental Leave and Pay Review are important opportunities to achieve changes.

- Reforming the occupational pension system so that people on low pay don’t miss out on employer’s pension contribution. This should include phasing out the £10,000 automatic-enrolment earnings threshold that excludes many women from workplace pensions and paying pension contributions from the first pound of earnings.

- Ensuring the pension system better recognises the value of unpaid caring and addresses the penalty faced by those who take time out of paid work because of caring responsibilities. This should include introducing a Carer’s Credit in addition to existing National Insurance credits for carers, to replace lost workplace pension contributions. This would mean carers qualify for extra state pension to replace some of the workplace pension they miss out on building up.

The Pension Commission

Last month, the Government revived the Pension Commission, which will bring together unions, employer and independent experts to look into the causes of the gap, among other issues.

It aims to reach a consensus on long-term changes needed to ensure that millions of people benefit from a more secure retirement – including women.

And where consensus already exists – like calculating pension contributions from the first pound of earnings and bringing more young workers into auto-enrolment – the government should press ahead quickly.

This is a much needed opportunity to ensure that everyone receives a decent retirement income and the gender pension gap is closed.

TUC General Secretary Paul Nowak said: “Everyone deserves dignity and security in retirement. But right now, too many retired women have been left without enough to get by.

“We must make sure that these inequalities are addressed for future generations.

“That’s why reviving the Pensions Commission – bringing together unions, employers and independent experts – is a vital step forward.

“We now have a chance to make sure everyone, including women, receive the decent retirement income that all workers need.”

Prospect Senior Deputy General Secretary Sue Ferns OBE said: “The Gender Pension Gap is very slowly moving in the right direction but without a more concerted effort millions of women will continue to suffer from unequal earnings in retirement for much of the rest of this century.

“The first step was the success of Prospect’s campaign for the government to recognise and measure the Gender Pension Gap. The next step is for government to show the way as an employer and take real action to close the gap by adopting trailblazing reforms across all public sector pension schemes.

“That the gender pay gap sits at 14% is unacceptable, for the gender pension gap to be more than twice that is nothing short of disgraceful and shames a society that doesn’t take action.”

TUC report on Gender Pension Gap can be found here.

{kind=link}

{kind=link}

{kind=link}