Today is Gender Pension Gap Day – the point of the year from which, if women received their pension at the same rate as men, they wouldn’t get another penny until January.

The fact that we reach this point in the middle of the summer holidays is a stark illustration of the levels of inequality in our pension system.

At just under 37.9 per cent, the gender pension gap is much wider than the gender pay gap and, according to annual research by Prospect, it has barely budged in recent years (it stood at 40.7 per cent in 2015-16 when the trade union started measuring it).

The result is that, taking into account all forms of pension, retired women today have incomes around £7,000 a year lower than retired men.

What causes the gender pensions gap?

There are three main drivers of the gender pensions gap:

- Different lifetime working patterns that mean women are more likely to take time out of the labour market or work part-time, most often because of unpaid caring responsibilities

- The gender pay gap, exacerbated by a workplace pension system that excludes many low earners altogether

- Differing levels of state pension entitlement

The impact of unpaid caring

Previous TUC analysis has highlighted the role of the pay gap – and a workplace pension system that excludes many low earners – in leaving women poorer in retirement.

But the most significant factor in the wildly unequal pension outcomes for men and women is the first bullet point – women are much more likely than men to spend time out of work or working part-time because of caring commitments than men.

This matters because our pension system is designed so that the typical worker will get around half the retirement income they need from the State Pension and half from a workplace pension.

National Insurance credits generally recognise the value of unpaid work such as caring so that people continue to build up state pension entitlement, but those out of paid work stop building up their workplace pension.

These contribution gaps are the biggest factor in women with a defined contribution pension approaching retirement having a pension pot less than half the size of men on average.

How wide is the ‘economic activity gap’?

New TUC analysis shows that women are vastly more likely than men to be out of paid work – and therefore unlikely to be building up a workplace pension – because of caring responsibilities.

This disparity can be seen in every age group, and is particularly wide for groups who face additional barriers in the labour market, such as disabled women and BME women.

Overall, women are 4.5 times more likely than men to be economically inactive – the Office for National Statistics’ term for people neither in or looking paid work – because of caring responsibilities.

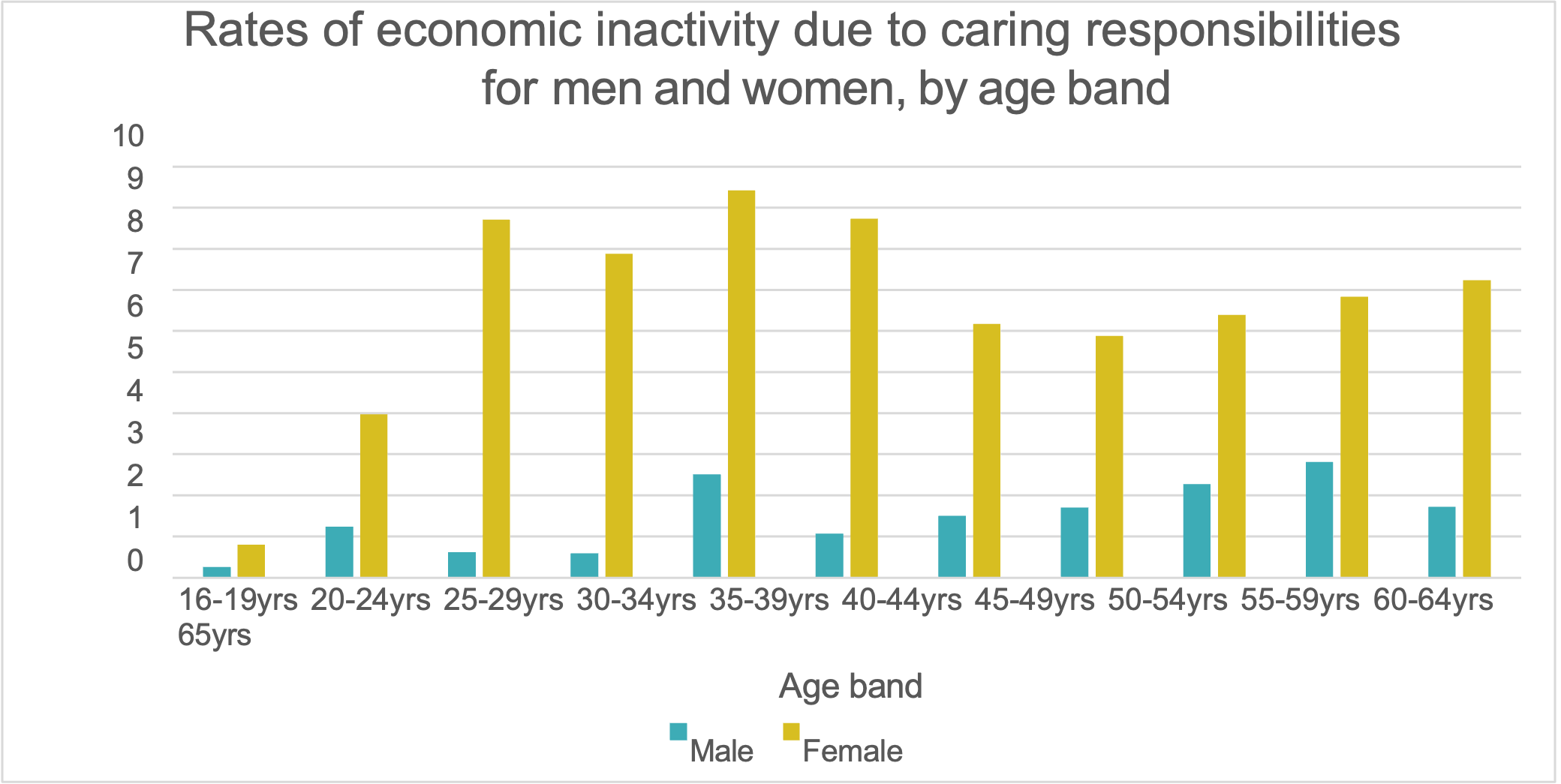

The chart below shows that rates of economic activity due to caring responsibilities peak between the ages of 25 and 44, with more than one in 11 women aged 35-39 in this category.

The gap is highest in the late 20s, with women aged 25-29 more than 14 times more likely than male counterparts to be out of paid work because of caring commitments.

{kind=link}

Source: TUC analysis of ONS Labour Force Survey, Q1 2024

This is perhaps unsurprising, with working mums much more likely to take time off work to look after kids.

It has a particularly large impact on pension saving, however. These are the years when workers typically have higher incomes than when they are just starting out, meaning their pension contributions are greater, but they are also far from retirement, so those contributions will remain invested for longer and have more time to grow.

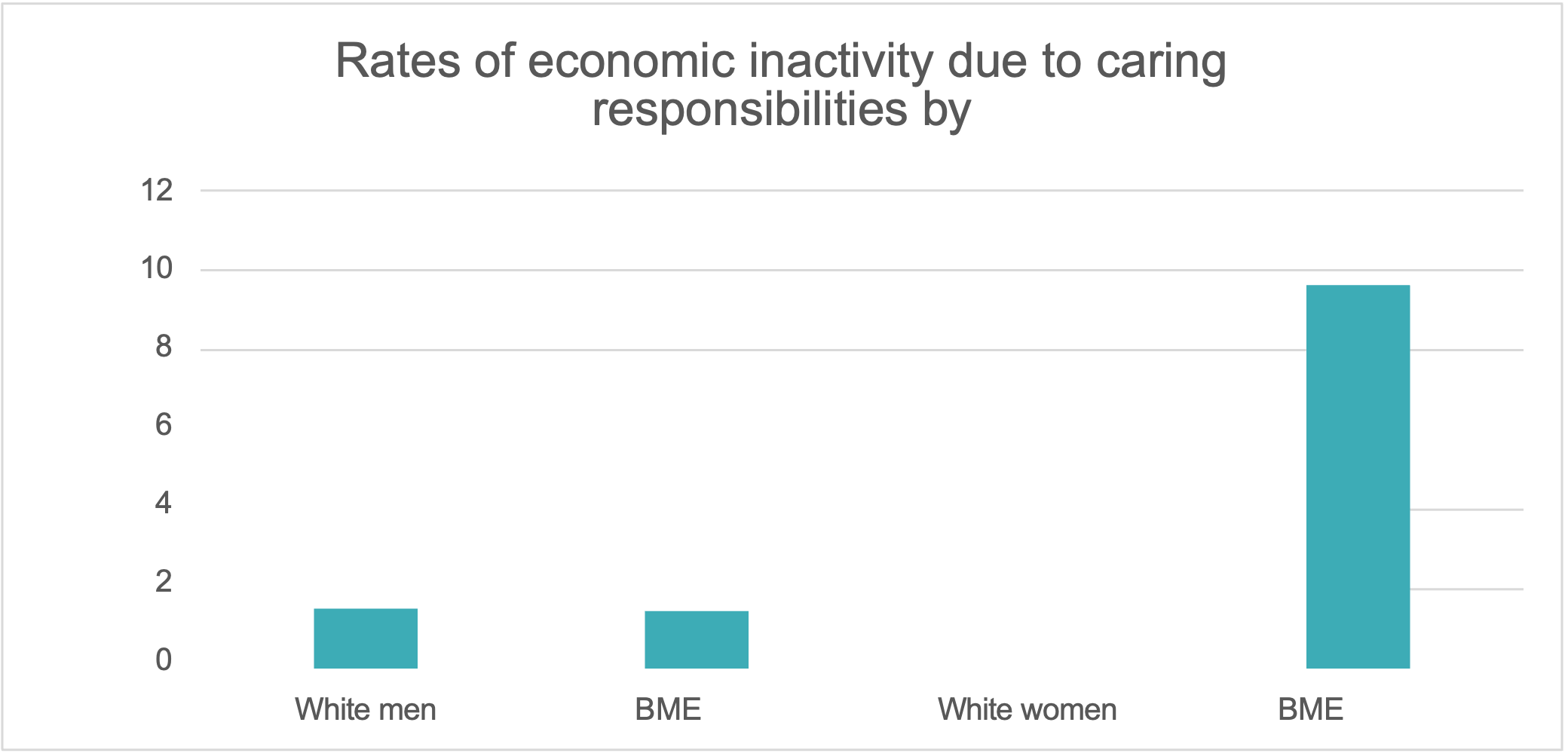

The charts below show that BME women are particularly likely to be affected. While white women are four times more likely than men to be out of work looking after a loved one, the figure rises to 6.4 times more likely for BME women.

Previous TUC analysis has highlighted the impact this has on older BME women, with almost one in three who leave the labour market before they reach State Pension Age doing so because of caring responsibilities.

{kind=link}

Source: TUC analysis of ONS Labour Force Survey, Q1 2024

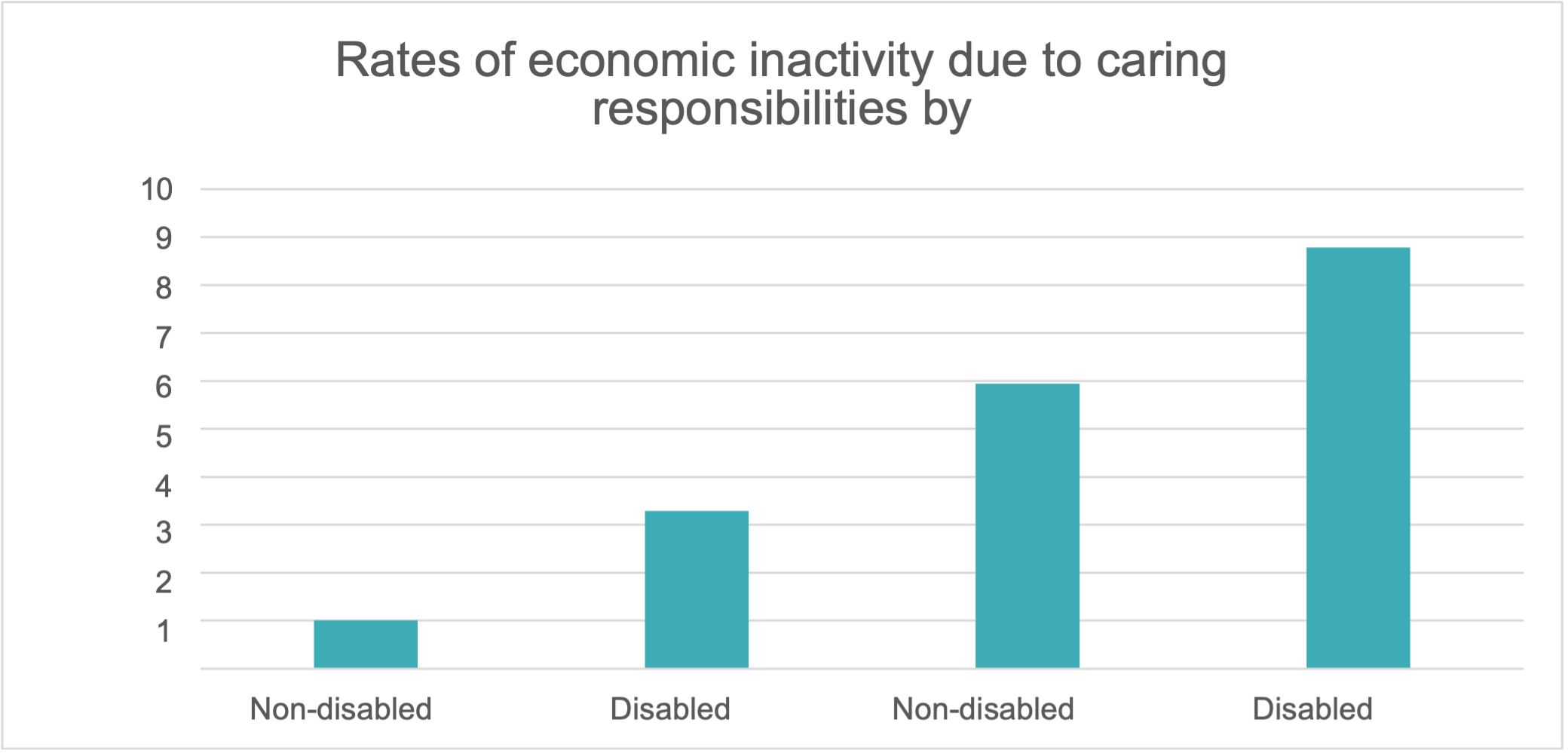

And the chart below shows that people who are themselves disabled, are also much more likely to be out of the labour market because of caring responsibilities to others.

Disabled women are almost nine times more likely than non-disabled men to be in this position.

{kind=link}

Source: TUC analysis of ONS Labour Force Survey, Q1 2024

Tackling the gender pension gap

The TUC has long called on governments to get serious about measuring the gender pension gap, and set out a plan to reduce it.

The last government did begin reporting on the gender pension gap (it’s measure looks only on the differences in workplace pension built up by men and women and put the gap at 35 per cent).

But this is only the first step, and the new government must build on this by setting out a comprehensive plan to reduce the gap

The recently announced Pensions Review is a great opportunity to do this, and we believe this should include an explicit strand on tackling pensions inequality.

We have previously made recommendations to bring more low paid and part-time workers into workplace pensions by expanding auto-enrolment, and to address the crisis in our social and childcare systems.

Time to give carers credit

But the figures above make clear that it will be difficult to improve women’s retirement incomes without improving the way our pension system recognises the value of unpaid care work.

This would require replacing the workplace pension contributions lost by those out of paid work, and there have been a number of proposals to introduce a Carers Credit that would do this.

We believe the most straightforward way of doing this is for those out of the labour market with a young child and registered carers to build up additional State Pension, on top of the flat-rate New State Pension.

This would be essentially reintroducing a feature that was removed in 2016. Before this point, people looking after children under 12 and registered for child benefit built up State Second Pension credit in addition to a credit towards the basic state pension.

When it was removed this credit was worth an extra £1.80 a week in pension in 2015-16 terms. So a worker who took five years out of paid work to raise kids, for example, would have built up almost £500 a year in additional State Pension over these years to plug the gap in their workplace pension contributions.

There is no single policy that would fix the gender pension gap, but introducing (or reintroducing) a Carers Credit would be a very significant step in the right direction.