A new annual report explores how the significant disruption of last year is setting the market mood of the construction sector in 2023.

Today, Glenigan, one of the construction industry’s leading insight and intelligence experts, releases its 2022 Construction Performance Review.

Providing a topline overview of UK construction sector activity over the past 12 months, this report evaluates overall output whilst offering insight into how this will influence the market in 2023.

Figures presented are drawn from Glenigan’s own data, combining both major (> £100m) and underlying (<£100m) projects, complemented with information from other official sources, including ONS figures.

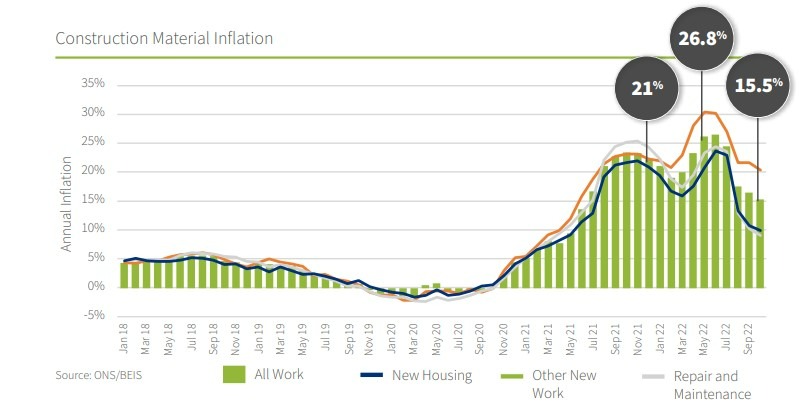

The key takeaway from the Review is the staggering inflation in construction materials costs, which had been gathering momentum since January 2021 to peak at a massive 26.8% in Q.2 2022. Whilst currently figures have settled at around 15%, ongoing international geopolitical events and domestic socioeconomic disruption indicates market volatility and, possibly, another inflation spike in the first half of 2023.

Looking at specific materials categories, energy intensive products were hit hardest, with the price of aggregates and insulation rising an eye-watering 53% and 32% respectively. More barriers to imports post-Brexit and rocketing power prices can be seen as the key reasons for these dramatic rises, and will put considerable pressure on contractors already working to extremely tight margins.

Labour and Wait

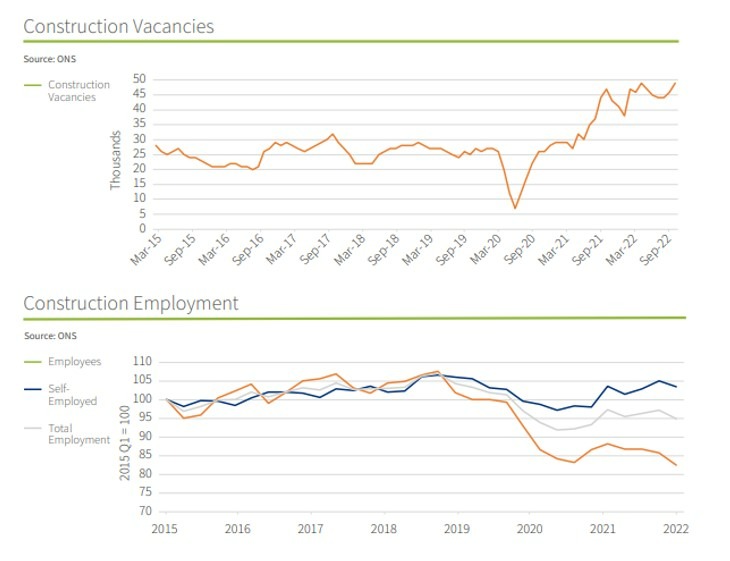

The construction sector also felt the pinch in terms of labour supply, which intensified over the course of 2022. Alongside legacy issues, such as a shallow recruitment pool and a greying workforce, Brexit and the Pandemic has resulted in less ready access to EU workers.

Looking at the figures as they stand at the start of the year, whilst there are currently 2.14 million employed in the sector, this number still languishes almost 7% below pre-Pandemic levels and 2.4% on a year ago. Couple this with 49,000 construction vacancies and there’s a shortfall with the very-real potential to stifle 2023 activity. This might put a serious dent in the current Government’s ambitious infrastructure and levelling-up plans in the short-term.

Projected Performance

Despite material and labour pressures, output actually rose in 2022 by 6% compared to the previous year. Most significant was a 52% leap in industrial new build and 11% registered for private residential new build activity.

However, tempering any optimism for a speedy recovery, a drop in the number of projects starting on site last year points to a weakening in construction output in 2023.

2022 saw a significant slowdown in projects progressing to work on site, as contractors and clients have reappraised the design and cost of build, largely prompted by price inflation and regulatory changes.

For example, many housing developers pushed back start dates in Q.3 2022, following the introduction of Part L of the Building Code. Overall this has led to a 50% increase in the time it takes from planning approval to commencing on site.

Furthermore, the value of underlying project starts also declined by 5% in the second half of 2022, compared with the same period a year ago. This was reflected in a 5% dip in the value of underlying planning consents during the same period and a concerning 14% drop in the number of projects securing planning consent.

Looking Ahead

Commenting on 2022 performance, and how it relates to the year ahead, Glenigan’s Economic Director, Allan Wilen, says: “The construction sector has already been buffeted by strong headwinds in the second half of 2022, and these look to become more forceful in 2023.

“The cautious optimism and tentative performance increase this time last year has been washed away by events out of the sector’s control, and many businesses will be battening down the hatches and hedging their bets for a potential, if modest, uplift in the latter half of the year.

“Whilst supply side pressures may ease, the skills shortage is a persistent problem which the industry will urgently need to tackle if it wants to return to pre-Pandemic output levels. However, there are a few bright spots in the gloom, with major projects including HS2 driving activity, as well as an increased focus on other critical infrastructure in energy, healthcare and data centre developments.

“Whilst next year will remain depressed, with a 2% decrease in the overall value of underlying project starts, Glenigan predicts a 6% increase in 2024, setting construction back on the road to recovery.”

To read the full 2022 Construction Performance Review Report, containing deeper analysis of the above, click here.

2023 sees Glenigan celebrate its 50th anniversary, commemorating half a century of delivering the highest-quality construction market intelligence.

To find out more about its services and expertise click here.