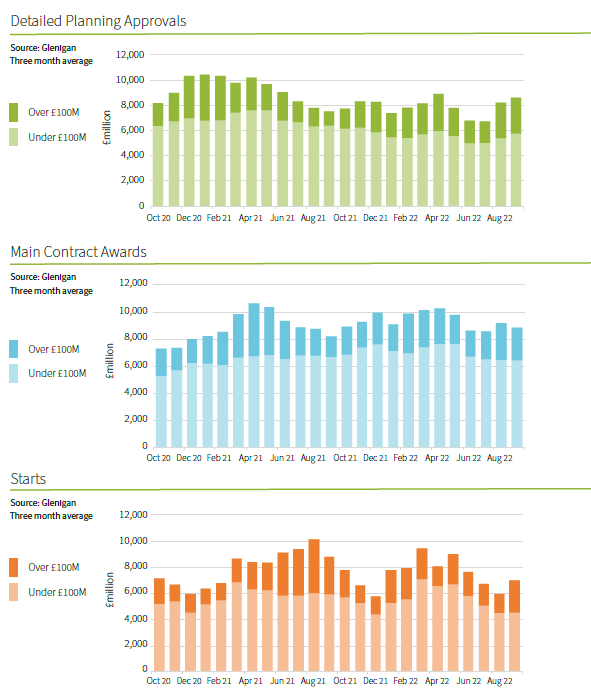

- Overall project starts decline 9% on previous quarter

- Major project contract awards and planning approvals up on 2021 figures by 59% and 158% respectively

- Civils project starts modestly increase due to a spurt of utilities-related activity

Glenigan, one of the construction industry’s leading insight and intelligence experts, releases the October 2022 edition of its Construction Review.

This Review focuses on the three months to the end of September 2022, covering all major (>£100m) and underlying (<£100m) projects, with all underlying figures seasonally adjusted.

It’s a report which provides a detailed and comprehensive analysis of year-on-year construction data.

The central finding of the October Review reflects recent, previous iterations, with high materials and energy costs, economic and political chaos and ratcheting building regulations keeping the market depressed for the foreseeable future.

However, whilst project starts dipped once more (-9% against the preceding three months), a modest rise in main contract awards (+3%) and detailed planning approvals (+3%) hint that recovery, although not immediate, is on the horizon.

Glimmers of Hope

The slight growth in the project pipeline can largely be attributed to a jump in major project contract awards, which were up 27% against the preceding three months, 59% higher than a year ago. Equally, major project planning approvals were up an impressive 58% by the end of Q.3, to stand a staggering 158% up on 2021 figures.

However, underlying performance was comparatively week, tempering results, dipping 8% compared the previous three months in contract award terms, 6% down on last year. Despite planning approvals increasing 8% over the past quarter, they remained 10% lower than a year ago.

Once again, major projects saw a respectable rise in work starting on site, climbing by a third in comparison to the preceding three months, however this figure remained 14% lower than the same period in 2021.

Underlying project-start performance was dismal, posting a 27% decline against the preceding three months, 23% down on last year.

Commenting on the results, Glenigan Economics Director, Allan Wilen, says, “The sector has faced considerable amounts of turbulence over the past twelve months. A new Prime Minister, changing of the ministerial guard and wildly fluctuating markets have done nothing to inspire consumer and investor confidence.

“At the time of this Review’s release, we find ourselves in a state of flux, with yet another new premier, however, the pound rallying once again and the promise of economic stability from the autumn financial statement should go some way to calming the choppy waters.

“With activity trickling back into the pipeline, everyone in the sector hopes the flow of awards and approvals picks up once again, even if project starts currently remain stagnant.”

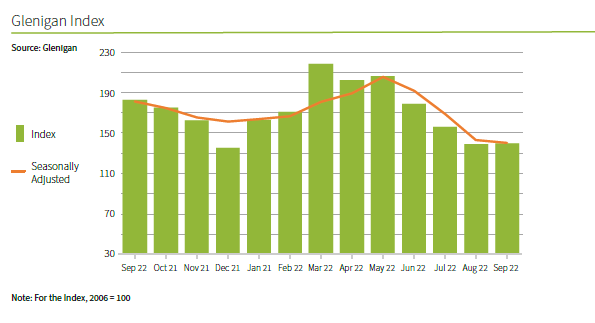

The sector-specific and regional index, which specifically measures underlying project performance, was characterised by overall decline. However, a few bright spots could be seen within an otherwise gloomy picture.

Sector Analysis – Residential

Overall, residential work starting on site fell by a third during Q.3, to sit 24% lower than a year ago.

Private housing performed particularly poorly, plummeting 37%, 20% lower than in 2021. Social housing also fell by 13% and 36% against the same set of criteria.

Sector Analysis – Non-Residential

Sharp decline was the consistent theme across most verticals during Q.3, education and health weakened 37% and 39% respectively against the preceding three months. Both were also down on 2021.

Office project starts fell dramatically, 30% against the preceding quarter and 37% compared to the previous year.

Industrial (-13%) and retail (-14%) experienced relatively small declines against the preceding quarter, but dropped 16% and 27% respectively against last year’s performance scores. Hotel and leisure was 13% up on the preceding three months but down 28% on 2021 levels.

Civils provided a welcome lift in an otherwise disappointing period, increasing 1% on the preceding quarter and over 10% on last year. Particularly, growth can be attributed to a spurt in utilities work starting on site, as well as a relatively steady stream of infrastructure project-starts.

Regional Performance

Once again, Northern Ireland performed well with project-starts increasing 31% against the preceding quarter, standing 51% up on a year ago. Wales also delivered positive results, remaining unchanged on the previous three months, rising 7% on 2021.

Unfortunately, the outlook was decidedly bleaker across the rest of the UK. The North East (-38%), East of England (-36%) and London (-30%) and Scotland (-26%), all slide back on the preceding quarter. London, which has seen a steady decline in activity over 2022, also posted the largest decline against last year, diving 45%.

Wilen concludes, “Sector verticals and the UK regions are feeling the economic pinch and, whilst a few major projects are bolstering results, the underlying figures indicate there’s a massive mountain to climb to stabilise the sector.

“The new Government needs to get a grip of the situation from day one and offer a clear strategy to support UK construction, which currently lacks the rigorous policy from key departments to recover and progress.”

To find out more about Glenigan click here.