Environmental campaigners have reacted to the announcement that oil giant Shell has made £8.19bn ($9.5 Billion) in profits in the third quarter of this year.

Campaigners say that the forthcoming Scottish Energy Strategy is a chance for Scotland to ‘chart a clear path’ away from the oil and gas companies who are harming people and the planet to instead create an energy system that runs on renewable energy.

Climate science is clear that we urgently need to transition away from our broken fossil fuel energy system in order to stay within safe climate limits. Analysis has shown that renewable energy is 9 times cheaper than new fossil fuel energy.

Independent climate advisors have made it clear that increasing UK supply of oil and gas will have almost no impact on UK bills as prices are set by the international market. However, continued reliance on volatile fossil fuels will leave millions vulnerable to spikes in their prices.

Shell’s profits for the previous 3 months of 2022 (Q2) were £9.5billion ($11.5billion).

Friends of the Earth Scotland’s Oil and Gas campaigner Freya Aitchison said: “The announcement of yet another obscene profit for Shell shows the scale of the pain that these companies are inflicting on the public.

“While oil companies continue to make record breaking profits, ordinary people are facing skyrocketing energy bills and millions are being pushed into fuel poverty.

“Bosses and shareholders at Shell are being allowed to get even richer by exploiting one of our most basic needs. Shell is also worsening climate breakdown and extreme weather by continuing to invest and lock us into new oil and gas projects for decades to come.

“The Scottish Government must use the opportunity of its forthcoming Energy Strategy to chart a clear path away from fossil fuels and towards an energy system that is built on clean, reliable renewables.

“They must listen to the science which tells us that to meet climate targets in a fair way, fossil fuel extraction needs to be phased out in the next decade.”

Drivers currently paying £463 on average following a recent spike

Drivers in central Scotland have seen the biggest increase to their car insurance premium over the past 12 months. The current cost stands at £505, on average, following a £73 (17%) rise.

Drivers in the Scottish borders are currently paying the cheapest rates for their car insurance. Premiums are £391, on average, despite a 20% price increase in the past 12 months.

Although FCA changes to regulation have made pricing fairer to customers at renewal, further research highlights that this does not necessarily protect customers from price increases. More than 2 in 5 (41%) UK drivers who received a renewal quote in the past 3 months said that they saw an increase of £38, on average(1).

However, those who shopped around using a price comparison website were able to save £50 on their car insurance, on average.

With the current cost-of-living crisis affecting millions across the UK, Confused.com recently launched its money saving hub to support consumers and give advice on how to manage recent price hikes.

In light of the recent price increases, Louise O’Shea, CEO at Confused.com emphasises the importance of shopping around for the best deals and why drivers shouldn’t settle for auto-renewal.

That means motorists are seeing a £69 increase compared to this time last year. That’s according to the latest car insurance price index (Q3 2022) from Confused.com, powered by WTW. Based on 6 million quotes a quarter, it’s the most comprehensive car insurance price index in the UK.

However, some drivers in Scotland could be paying more than the national average, depending on the region in which they live. The latest data shows that drivers in central Scotland are currently paying the most for car insurance.

Their current premium is £505, following a £73 (17%) year-on-year increase. Despite facing an annual increase of £64 (20%), drivers living in the Scottish Borders pay the cheapest rates for their car insurance, with an average premium of £391.

Meanwhile, drivers in East and North East Scotland are paying £431, on average, for their car insurance. That’s as drivers faced a £69 (19%) increase in the past 12 months. And as for drivers in the Scottish Highlands and Islands, the current car insurance premium is £420, on average, following an increase of £61 (17%).

Region

Average Premium

YOY £

YOY %

Scottish Borders

£391

£64

20%

Central Scotland

£505

£73

17%

East & North East Scotland

£431

£69

19%

Scottish Highlands & Islands

£420

£61

17%

It’s a similar picture across the rest of the UK, where prices continue to rise. In fact, premiums have risen by £72 (14%) in the past 12 months alone.

The current UK premium stands at £586, on average, and is the highest annual increase in the past 5 years.

With the latest data revealing that premiums are on the rise, some drivers might think that they’re better off sticking with the same insurer when it comes to renewal. But further research conducted by Confused.com finds that some insurers don’t seem to be doing enough to protect their existing customers.

In a survey of 2,000 UK drivers, data reveals that more than 2 in 5 (41%) drivers who considered sticking with their current insurer received renewal quotes £38 more expensive than the previous year, on average(1). That’s despite the fact that more than a quarter (28%) of drivers who have renewed so far this year thought that their insurance quote would be cheaper this time around.

However, some motorists are taking action after receiving a more expensive renewal and are really seeing the benefits of switching. More than a quarter (27%) of drivers who chose to shop around using a price comparison site were able to save £50, on average. In fact, the Financial Conduct Authority (FCA) is actively advising consumers to shop around when it comes to buying insurance for this very reason.

Earlier this year, the FCA made important changes to stop ‘price walking’ and ensure all customers were treated fairly, but it seems some motorists remain complacent as a result. One in 5 (20%) drivers told Confused.com that they were less inclined to shop around because of these changes.

However, these new regulations don’t mean that better deals still can’t be found elsewhere and, as research shows, consumers are saving money by switching.

While the cost of car insurance premiums is on the up, there’s no ignoring the fact that the general cost of living is increasing, too. That’s why it’s more important than ever to shop around for the best deals. And as we head into the colder months, it’s clear that money will be tight for many.

With difficult months ahead, Confused.com has launched a money saving hub to help people understand where they can save money on bills to balance out price hikes. The hub focuses on a variety of insurance options, but also includes advice on how to be more fuel efficient and keep car costs down.

Its aim is to provide useful and digestible information that will help customers save money, without necessarily having to compromise and give up essentials.

Louise O’Shea, CEO at Confused.com, comments: “With costs currently rising all around us, I’m sure it comes as no surprise that the cost of car insurance is increasing, too.

“However, the pace at which it’s rising will be a real worry for many. The latest figures reveal a true example of how volatile the market currently is, which is why I need to stress just how important it is to shop around when it comes to renewing any insurance policy.

“As we head into winter, money is going to be tight. With concerns over the rising costs of energy, fuel and even food, millions of us will be looking for new ways to number-crunch and save money where we can. In recent months, the FCA have really amplified the importance of shopping around to help find some of the best deals out there during this time.

“Research shows that customer loyalty doesn’t always pay off, which is why it’s always encouraged to shop around and see what else is out there. If you switch insurers using Confused.com, there’s some fantastic rewards available that could help during a difficult time.

“A £20 voucher could pay towards a food shop in Lidl or even go towards an MOT or service in Halfords. And we even guarantee to beat your renewal(5). If we can’t, we’ll give you £20, plus the difference. Either way, you’re better off just by using a price comparison service.

“I cannot emphasise enough just how important it is to take time, do your research and compare insurance prices. You might be missing out on fantastic deals and it will really help in the long run.”

The First Minister has convened a second summit with energy companies and advice organisations.

Further actions to support consumers and businesses through the winter have been agreed at yesterday’s virtual summit between energy companies and advice organisations and Ministers.

The energy cost crisis summit discussed this week’s reversals to UK Government measures set out since the previous summit, and agreed longer-term certainty is urgently needed ahead of the anticipated energy price cap increase, currently due in April.

First Minister Nicola Sturgeon said: “The curtailing of the Energy Price Guarantee by the Chancellor of the Exchequer earlier this week has eradicated what meagre certainty people and businesses had over their bills and finances in the short to medium-term.

“Even the current cap of £2,500 until April – while better than a rise to £3,500 – is still a very significant increase for households who are already struggling to pay their bills and heat their homes. Without further mitigation the increase to £2,500 under the Energy Price Guarantee will see an additional 150,000 households in extreme fuel poverty.

“The deficiencies in the UK Government’s package mean we are still in an emergency situation. The economic outlook has been made far worse by other aspects of the mini-budget – most of which have now had to be reversed entirely.

“The Scottish Government is working hard within its limited powers and finite budget to support people, business, public services and the economy. Part of that work will involve ongoing engagement with energy companies and advice organisations throughout the winter to see how, individually and collectively, we can alleviate the huge challenges people are facing as well as signposting existing schemes and support that is available.

“It is clear however that more substantial reform of the energy market is needed to address the issue in the long term, and the power to do so lies with the UK Government.”

ADT shares guidance on protecting homes amid rise in property crime

ONS has recently released its property crime data, which shows that 23% of the UK have been victims of household theft from April 2021 to March 2022 – up 2% from last year.

As the nights get darker earlier, and clocks change, the security experts at ADT have provided top tips to ensure your property is fully protected this winter.

Glenn Amato, Managing Director, Subscriber UK&I at ADT UK said: “The latest data from ONS shows a rise in household theft over the last year, with 23% of the UK being victims of it – though this isn’t wholly surprising, given that there are less people working from home full time now.

“That said, when paired with the deepening cost of living crisis, the potential of a looming recession and moving into the winter season and darker nights, it’s understandable how some people might be starting to feel concerned about the safety of their homes.

“In the 2008 recession, we saw rates of personal theft increase by 25% and burglaries rise 4%, so if the country heads into another recession, property crime could sadly increase again.

“Historically, when the cost of living has increased, there has also been increases in ‘snatch and steal’ type crimes. “

The good news is that there are many precautions homeowners can take to protect their properties and feel safer:

1. Double lock and double check – one lock on the door often isn’t enough to protect the home, burglars can use their foot to check whether there is a deadlock on the door. Invest in a second lock and always double check both front and back doors are locked when leaving the house.

2. Social Media awareness – If a burglar has access to your name through old post or personal information, they can easily find your social media accounts too. Sharing posts whilst you’re away visiting relatives during the Christmas season, or posting so-called holiday countdowns are an open invitation for burglars to head into your home with the knowledge that they won’t be disturbed.

3. Think twice about lights – While leaving your lights on may signal an occupied house to potential intruders, it can increase the cost of bills, as well as making valuable belongings more visible to thieves. Consider using smart plugs to turn lights on, only when necessary and you’re away from your home to give the impression of occupancy. Make sure curtains or blinds are closed at night so that potential burglars don’t have a direct line of sight into your valuables and the layout of your home, and only leave on dim or energy saving bulbs.

4. Invest in your security – Having an up-to-date digital alarm system is the best way to prevent burglaries. It’s worth investing in home security that is professional installed and monitored by trusted professionals, which signals directly to an alarm receiving centre when it detects an intruder. Smart home security systems are also a great option for people looking for protection. Systems like ADT’s Smart Home system integrate entry sensors and sirens to a range of devices like lights, smart plugs, doorbells, cameras and remote mobile apps, by connecting through WiFi and GPRS.

5. Forget hiding a key – Most people have managed to lock themselves out at least once but hiding a key in the vicinity of a home – whether under a flowerpot or above the doorframe – simply isn’t worth the risk. If a spare must be kept outside, at least keep it in a locked key safe, which requires a code.

THIS week the government replaced one catastrophic plan with another (writes TUC’s GEOFF TILY). A new course to placate financial markets is traded off against likely massive hits to household budgets and fears about the future.

Support for energy bills was cut, public services already stretched beyond breaking point will be hit again, little was offered on soaring borrowing and mortgage costs, and nothing about already deeply inadequate benefits and universal credit falling further behind inflation.

There is another way to deliver an economy that works for working people, but the government couldn’t be further from it,

Dealing with failure

The Truss government were right about one thing, the economic policies of the past decade and more have been a disastrous failure. As Kwasi Kwarteng admitted, growth has been ‘anaemic’. In the ONS words: the UK is the only G7 economy yet to recover above its pre-coronavirus pandemic level in Quarter 4 2019. The UK has the lowest investment as a share of GDP (see our ‘companies for the people report’, Figure 7) In Spring OECD figures showed UK real wages would fall furthest of all G7 economies.

Mini budget catastrophe

But the mini budget was catastrophically wrongheaded. Truss and Kwarteng took the fundamental problem of an economy serving wealth not work and turned it into the solution. The flip side of support for energy bills, was lavish tax breaks for those least in need – under the spurious and long discredited fallacy of ‘trickle down’.

On top of this their intention was to borrow to fund this extreme project. They did so the day after the Bank of England had confirmed that they would be reducing support for government borrowing, and implementing a £80billon programme of ‘quantitative tightening’ [i.e. selling back government bonds to financial markets] from the start of October. (Regardless of anything else this revealed staggering lack of coordination on the part of both institutions – the excellent Daniella Gabor called this ‘uncoordinated class war on the British public’.)

Financial markets took fright and instead of buying started to dump government debt, but this was also intimately connected to a third factor. The complex financial strategies – so-called liability driven investments (LDI) – that pension funds have been deploying (unnoticed by most) for the past 20 years began to unravel in the face of these rate rises.

The Bank of England was obliged to step in to halt a vicious cycle – or doom loop – of bond sales leading to higher interest rates and so more bond sales. The spike in the chart below of interest rates on UK 30-year bonds shows how the episode was at least momentarily brought under control.

And in the meantime the government came under sustained assault for ‘fiscal irresponsibility’.

U-turn to a worse economy

After two U-turns (on the 45p top rate and corporation tax reductions), yesterday they U- turned on pretty much the whole thing.

But reversing a wrong doesn’t make a right, far from it.

We are now on the brink of a deep and damaging recession that threatens millions of jobs. But the latest Conservative chancellor has now announced the same basic approach that got us into this mess.

He warned of “more difficult decisions” on tax and spending to come. And immediately that “Some areas of spending will need to be cut”.

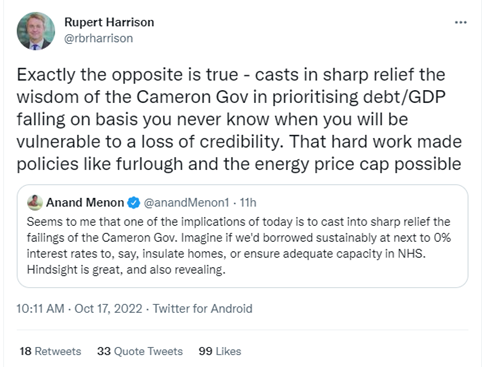

The Chancellor not only announced austerity. He not only sought once more – as did his George Osborne – to make a political virtue about imposing misery. He even invited George Osborne’s favourite adviser Rupert Harrison (now at Blackrock, one of three key institutions in LDI strategies) back to the Treasury to head a new panel of ‘economic advisers’ to deliver this reborn monstrosity.

Yesterday morning Rupert gave his City-oriented perspective on austerity

But this is a seriously misleading statement. The Osborne government did not repair the public finances. Over 2010-2019 the public debt ratio increased by 22 percentage point of GDP – the worse performance over a decade of economic recovery for a century (here).

For workers, this meant the worst pay crisis for 200 years. As Frances O’Grady spells out today, now expected (and this was before yesterday) to last at least two decades.

But the context for policy today is even more worrying than in 2010. Central banks, led by the Federal Reserve in the United States, are engaged in a forceful (their word) tightening of monetary policy.

This amounts to ending a strategy that has been in place since the start of the global financial crisis. In the wake of the last increase to 3.0 to 3.25 per cent, a Fed committee member has pointed to rates at up to 4.5 to 5 per cent. Fear of the impact of these rate rises on mortgage rates is likely common to all countries – for example in the US rates on a 30-year mortgage are up from 2.7 per cent at the start of 2021 to 6.9 per cent now.

And while in the UK the spike was brought under control, government interest rates are still seriously elevated and will carry on feeding through to mortgages.

In the UK money expert Martin Lewis has offered a grim rule of thumb: “For each 1 percentage point your mortgage rate increases, expect to pay roughly £50 more a month (£600/year) per £100,000 of mortgage debt.” The Resolution Foundation reckoned five million families would see annual payments rising by an average of £5,000 between now and the end of 2024.

Standing further back, the Financial Stability Board (Dietrich Domanski on the Today programme, 6 Oct.) have warned of the challenges of raising interest rates to deal with inflation under the conditions of the high global indebtedness that prevail today.

Likewise the IMF last week warned of “hidden leverage”, “waves of deleveraging”, and in particular the risk to ‘non-bank financial institutions’ – the latter including pension funds.

In terms of countries, first in the firing line are emerging market economies – with 20 countries “in default or trading at distressed levels”.

While the immediate trigger for central bank policies is the inflation set in motion by the end of lockdowns and Putin’s brutal invasion of Ukraine, the scale of the dislocation reflects a wider failure to set the economy right since the global financial crisis of 2008-09 exposed deep underlying failings. Summing up, the IMF offered the chilling: “the level of risk we are flagging at the moment is the highest outside acute crisis”

As the Biden administration has argued, for 40 years the interests of wealth have been prioritised over those of workers. The economy crashed in the first place because these financial interests proved wildly at odds with the interests of the population as a whole. An economy of speculation and debt crowded out production and decent pay and work.

The chancellor’s new advisory panel puts these interests back front and centre of policymaking at the Treasury. The other members so far announced are also from the City of London, not least securing J.P. Morgan a seat at the table.

Yesterday the Financial Times reported that the Bank of England’s programme of quantitative tighten has been put on hold, likely to protect the casino capitalism around pension funds.

Ahead of the mini budget the TUC issued a plan for a budget ‘on the side of working people’. We desperately need a government that will put first our interests not those of wealth. But instead once more the interests of the city of London are put ahead of those of workers and the country.

Latest research from the Gas Safe Register reveals that almost one third (31%) of UK homeowners will skip their annual gas safety checks this year in attempts to reduce household costs. Heating expert and leading manufacturer, Alpha, believes a nationwide call to action is needed to address this imbalance and ensure gas safety remains an essential priority.

“The Gas Safe Register data is alarming and demonstrates yet further implications of the cost-of-living crisis,” says Alpha’s product engineer, Jonathan Kidner. “Gas safety checks in the home can prevent serious or life-threatening accidents including gas leaks, explosions, house fires and carbon monoxide poisoning.

While it was encouraging that the research also showed the majority (77%) of homeowners knew the benefits of regular servicing and maintenance, most notably performance and cost savings, it seems this awareness isn’t translating into enough action and is therefore an extreme cause for concern.”

Alpha argues one of the most important steps for homeowners is to arrange for a Gas Safe Registered engineer to undertake checks on all gas appliances, including an annual boiler service.

This will not only ensure boilers continue to run at optimum efficiency, but also identify any potential faults and ensure warranties and insurance policies remain valid. Homeowners can set reminders for boiler services via the Gas Safe Register’s Stay Gas Safe website.

Jonathan continues: “The boiler is one of the most used pieces of equipment in the home yet the perceived maintenance costs remain one of the main reasons people don’t book a service; our own research from 2021 indicated this being the barrier for 54% of respondents. This needs to change.

“The experts at Which? suggest the average price of a boiler service is just £80 which, when compared with the cost of repairing or replacing the most common faulty parts, could save homeowners anywhere between £30 and £219.”

Additional measures homeowners can take to remain gas safe include:

Undertaking visual checks to look for warning signs on unsafe appliances including lazy yellow flames instead of crisp blue; pilot lights which frequently blow out; excessive condensation on windows; and unusual dark marks/staining on or around gas appliances;

Testing and replacing smoke alarm batteries;

Installing a carbon monoxide alarm and familiarising themselves with the six key symptoms of carbon monoxide poisoning.

Jonathan concludes: “While some of these points may seem obvious or even repetitive, the Gas Safe Register research highlights there is a need for reinforcement.

“Only one in three homeowners knew house fires were a potential result of not having regular gas safety checks and less than half could correctly identify symptoms of carbon monoxide poisoning.

“This is a conversation we need to keep having until this knowledge becomes commonplace.

“We understand the collective concern about rising costs but the loss could be far greater if we do not encourage homeowners to act now and prioritise their gas safety.”

In response to the cost of living crisis, Fresh Start will be hosting a weekly community meal (Meet and Eat) on Wednesday evenings and Friday afternoons at Fresh Start Kitchen, 28-30 Ferry Road Drive – see flier (above).

This is for anyone you can think of who would benefit specifically from a free two course hot meal in a safe and welcoming environment.

We will begin the Wednesday evening Meet and Eat on 26th October, and this will run until March 2023.

Our Friday afternoon Meet and Eats are currently running as usual:

First Minister announces doubling of December Bridging Payment to £260

Families of an estimated 145,000 children will benefit from extra support this winter to help with cost of living pressures – backed by Scottish Government investment of £18.9 million.

Bridging Payments were introduced in 2021 ahead of the extension of the Scottish Child Payment to 6-15 year olds. The final quarterly Bridging Payment, due in December, will now be doubled to £260, meaning families will receive up to £650 per eligible child this year.

All children registered to receive free school meals on the basis of family low income are eligible and will receive this payment automatically.

Total Scottish Government funding for the Bridging Payments will increase to an estimated £169 million across 2021 and 2022.

This is in addition to the Scottish Child Payment which will be extended to all eligible under-16s from 14 November and will rise to £25 per child per week on the same date – a 150% increase in the benefit within eight months.

First Minister Nicola Sturgeon said: “I am proud of the work the Scottish Government is doing to tackle child poverty. The Scottish Child Payment is paid to eligible families and is unique in the United Kingdom.

“It started for under-6s at £10 per week per eligible child. In April we doubled it to £20. Five weeks from today we will increase it again, to £25 and will also extend it to families with children up to age 16.

“That is vital financial help for well over 100,000 children, delivered in time for Christmas. That is the sign of a government with the right priorities.

“But we need to do more because we know this winter is going to be really tough. Rather than looking forward to Christmas, too many families will be dreading it because they don’t know if they can afford to heat their homes or even pay for food.

“As part of our help to the poorest families over last year and this, ahead of rolling out the Scottish Child Payment to under 16s, we have made quarterly bridging payments of £130 to children and young people in receipt of free school meals.

“I am delighted that the Scottish Government will double the December Payment from £130 to £260.

“That will help put food on the Christmas table for families of 145,000 children and young people. I don’t pretend it will make all of their worries go away – no government with our limited powers can ever do that. But I hope this investment of almost £20 million will bring a bit of Christmas cheer to those who need it most.”

Bridging Payments were introduced in 2021 ahead of the roll out of the Scottish Child Payment to under 16s. The £130 payments are paid quarterly by councils on behalf of the Scottish Government. Families received up to £520 per eligible child in 2021 and will receive up to £650 in 2022. Bridging Payments support around 145,000 school age children.

Povery campaigners have welcomed the announcement.

The Poverty Alliance tweeted: ‘We welcome @NicolaSturgeon announcement today that the @scotgov will double the final Scottish Child Payment bridging payment, up from £130 to £260.

‘This will put cash in the pockets of those who need it most. This is how we #ChallengePoverty‘

Business activity across Scotland’s private sector contracted again in September, according to the latest Royal Bank of Scotland PMI® data. The seasonally adjusted headline Royal Bank of Scotland Business Activity Index – a measure of combined manufacturing and service sector output – was little-changed from 47.8 in August at 48.0, signalling a second consecutive month of contraction.

Despite easing, a high inflationary environment drove the latest decline in business activity and new orders, with the rate of contraction for the latter gaining momentum.

The challenging conditions meant that the degree of confidence further weakened during September. The latest reading registered a 28-month low, suggesting subdued performance as we progress into the final quarter of the year.

New business received at Scottish private sector companies contracted for the third month running during September. The rate of reduction quickened on the month and was solid overall. Inflationary pressures and the cost-of-living crisis were primarily linked to the latest downturn.

At the sectoral level, manufacturing firms reported the softest decline in factory orders in three months, while services providers reported their first contraction since March 2021.

Amid soaring prices and recession fears, overall activity expectations weakened for the second consecutive month in Scotland’s private sector in September. Business confidence hit a 28-month low, posting below the average recorded over the series history and much weaker than the UK-wide average.

As has been the case since April 2021, employment across Scotland’s private sector increased in September. According to anecdotal evidence, successful hiring was in part linked to fresh graduates entering the workforce. While the respective seasonally adjusted index improved marginally from the that seen in August, it was the second-lowest reading in 17 months.

The pace of employment growth in Scotland was softer than the UK average.

September data revealed a reduction in backlogs of work for the fourth consecutive month at private sector companies in Scotland. The rate of depletion quickened to the fastest in 20 months. Respondents frequently mentioned the fall in backlogs reflected fewer new orders.

The rate of reduction at Scottish private sector companies was quicker than the UK-wide average which, in contrast to Scotland, softened during September.

For the twenty-eighth month running, average cost burdens rose across private sector firms in Scotland during September. The rise was largely blamed on inflationary pressures in labour market and supply chains. Despite the rate of input price inflation remaining historically high, the latest incline was the softest since August 2021 with both sectors noting slower rates of inflation.

Moreover, the pace of inflation in Scotland lagged behind that seen at the UK level, posting the second-softest of the 12 monitored regions ahead of the South West of England.

Scotland’s private sector firms raised their charges during September, thereby stretching the current run of output price inflation to 23 months. According to panellists, prices were raised primarily to offset increasing costs. That said, the rate of output price inflation was the weakest in 13 months and the softest of the 12 monitored UK regions.

Source: Royal Bank of Scotland, S&P Global.

Judith Cruickshank, Chair, Scotland Board, Royal Bank of Scotland, commented: “Business activity and new orders continued to decrease across the Scottish private sector during September, thereby stretching the current runs of contraction to two and three months respectively.

“The squeeze on customer disposable incomes amid a high inflation environment underpinned the latest downturn in output and new business.

“Despite falling business requirements, firms raised employment for the eighteenth successive month, albeit at a moderate pace. The combination of a drop in new work and expanding workforces allowed firms to work through their backlogs.

“The post-pandemic boom is clearly at an end, as the ongoing cost-of-living crisis plays an increasingly important role. Moreover, the 12-month outlook continues to weaken.”

From small jobs to big changes, here are our top tips for cutting your energy bills

WHICH? consumer research found that in August 2022, 65% of households cut back, dipped into savings or borrowed money in order to cover essential spending. And with most people’s gas boilers whirring into action this month as the temperature drops, outgoing expenses are only increasing.

Our experts have identified a variety of ways to reduce your heating energy bills this winter.

The big things can drastically change how much energy you use every year, while the small things can cheaply make an immediate dent in your bills during a time where a bit of help goes a long way.

Sometimes it’s simply a matter of using a new boiler setting or spending 15 minutes plugging a gap in your home that provided a welcome breeze during the summer heatwave. We’ve also listed a few more expensive, longer-term fixes. If you do feel able to, it’s worth thinking about whether any of these could suit your home.

Read on for our top tips for getting ahead this winter.

Emily Seymour, Which? Energy and Sustainability Editor, said:“Many people will be looking to save money by reducing their energy use this winter. Some easy ways to cut your bills include using radiator valves to make sure each room of your house is only ever as warm as you need it to be.

“If your home has a single room thermostat, it should be set at the lowest comfortable temperature as heating bills will rise by about 10 per cent for every additional degree you turn it up.

“Combi boiler owners can try turning its flow temperature down and the preheat setting off. Tap water will initially come out cool before it heats up, but you’ll be wasting less energy.

“If you have a hot water cylinder, you can’t make use of low flow temperatures. Instead, insulate your hot water tank with a jacket no less than 75mm thick and make sure you’ve got lagging on pipes.

“Simple steps like placing weatherproofing tape over gaps or putting down a draught excluder can guard against heat loss.”

Boilers are easy to cast as a cost-of-living villain. They’re big, sometimes noisy, most of them run on fossil fuels, and they can have a big impact on your energy bills – in fact, in most homes the boiler is the one single thing that uses up the biggest portion of your annual energy bill.

But a central heating system that’s working efficiently and using energy proportionate to your home’s heating need is still the best way to heat your home during the coldest months of the year.

For most people, the priority should be making your boiler cost less to use, and not deferring to replacements like portable heaters.

There’s a lot you can do to make your heating run more efficiently:

Get your boiler serviced. This will reduce the chance of a costly emergency repair and keep a new boiler in warranty. Plus, a well-maintained central heating system will run more efficiently, and you can ask your boiler engineer about whether your boiler’s settings can be toggled to run more cheaply. If you rent, you are within your rights to ask your landlord to arrange a boiler service every year.

Toggle pre-heat off. Combi boilers use water on demand, but sometimes they pre-heat water so it’s ready to get to taps quicker. This is nice, but it will keep your boiler burning more than it needs to.

Bleed your radiators – or ask an engineer to do it if you prefer – and install thermostatic radiator valves (TRVs) onto them so you can turn radiators off in rooms you don’t often use (more on this below).

Combi boiler owners should look at their flow temperature. You can save up to 8% on your heating bill by turning down the temperature of the water that gets circulated around your radiators. If your boiler heats this water to its max, your boiler won’t even condense, which means it’s running inefficiently.

The Heating & Hot Water Industry Council (HHIC) recommends that people adapt their boiler settings with the advice of a boiler engineer. This is particularly true if you have a system or regular boiler that keeps water stored in a tank. Because stored water needs to be heated a certain amount to avoid Legionnella bacteria, you should only change settings with professional advice if you have one of these.

However, if you have a combi boiler, you’ve made sure it’s safe and you’ve checked your boiler’s technical manual, you can adjust these settings yourself.

This setting is accessible to anyone and it can be changed using your boiler controls. The flow temperature for heating is generally symbolised by a little picture of a radiator, and for hot water, a picture of a tap. Up and down arrows will change the temperature settings.

It recommends a 55°C setting, but we suggest starting a bit higher initially to see if you’re comfortable with the change.

3. Insulate your boiler’s hot water cylinder and pipes

if you have a boiler with a hot water tank, the advice above doesn’t apply. That’s because boilers that store water in a tank usually can’t manage the efficiency gains of combis as they’re not well suited to running low flow temperatures without modification.

You shouldn’t change the flow temperature of a regular or system boiler with a hot water cylinder without consulting an engineer, because your boiler must be able to pasteurise stored water effectively to avoid bacteria such as Legionella developing.

However, that doesn’t mean there’s nothing you can do to improve your boiler’s efficiency. You’ll be using a lot of energy to heat up the water in your storage cylinder, and you don’t want to lose out on any of that. So make sure the cylinder itself is well insulated. This can be as easy as buying a jacket for about £20. It should be no less than 75mm thick according to industry standards.

You can also lag the pipes that carry water around your home for around £5 a metre. Water loses a lot of heat in transit, so it’s a small expenditure for a good long-term saving. It’s particularly useful to do it for the pipes coming in and out of the cylinder.

Lagging pipes will also reduce the risk of them freezing in a cold spell, which can be costly to repair.

Smart technology isn’t for everyone, but if you do like using your phone, tablet or voice assistant for managing your home, then a smart thermostat will give you easy and precise control over your central heating.

They’re designed to provide automation to help you use your heating at the best times. Whether it’s toggling your boiler when you’re nearby to benefit from it, learning your routine so it can predict the optimal times to run or even checking the weather forecast to anticipate increases and decreases in heating need, smart home heating is becoming increasingly clever.

While many of these features are designed for your comfort, rather than your wallet, smart thermostats really come into their own when it comes to making savings if you set up zonal heating with compatible radiator valves.This means you can vary the routine and temperature of different rooms so you’re not wasting energy by heating rooms at the wrong times.

For example, you might want to programme your kitchen to get a burst of heating in the morning before you put the kettle on and your living room to be warmest in the early evening, while you’re happy for your bedroom to stay cold all day until you’re about to go to bed. All of these adjustments mean you’re saving crucial kilowatts by never heating a room you’re not actually using.

Since the introduction of new legislation in 2018, new gas boilers need to come with one of four energy-saving add-ons. Smart heating controls are one of them. But if you have an older boiler you can still buy and install a smart thermostat separately.

If smart tech isn’t for you, you can still make significant improvements by installing manually operated thermostatic radiator valves, or TRVs. They control the heat of your home by adjusting how much hot water flows through the radiator they’re fitted to, so you can make sure each room of your house is only ever as warm as you need it to be.

It works by sensing the room temperature and opening or closing the valve as appropriate.

The numbers on TRVs determine how much a radiator is allowed to heat up. They correspond more to a level of comfort than a specific temperature, but as a rough guide the following applies:

0

Off

* (the maintenance setting)

The radiator will turn on as a protective measure when the temperature nears 0°C.

1

Approximately 12°C, a low room temperature for an unoccupied room

2

Approximately 16°C, a lukewarm heat for an occupied room.

3

Approximately 20°C, a comfortable heat for an occupied room.

4

Approximately 24°C, a warm heat for an occupied room.

5

The valve is fully open.

Use trial and error. We recommend using settings two and three to try and cut heating use, knowing that you can go higher if you’re feeling chilly.

If you’ve also turned down your boiler’s central heating flow temperature, you might find you need to open your TRVs to higher settings to reach comfortable temperatures.

Smart radiator valves can work with smart thermostats to do this automatically. Some of them also take temperature readings to fine-tune your thermostatic system.

6. Turn your thermostat down a little

It’s age-old advice, and for people who are already frugal with their heating it may not apply. But each degree you turn your thermostat down is energy saved. According to the NHS, temperatures as low as 18°C are healthy for most people.

The Energy Saving Trust claims that turning your thermostat down by one degree can save you up to 10% off your heating bill. Realistically, a lot of variables affect this, but even one degree lower will move your bills in the right trajectory.

For older people, Age UK reminds that very low temperatures can increase your risk of flu or other breathing problems, and can raise your blood pressure. When you’re older, your blood pressure takes longer to return to normal once you get cold. Try to make sure you’re keeping at least one room at a comfortable temperature for you, and keep the doors closed as much as you can to keep that room as warm as possible.

7. Only use electric heaters sparingly

We’re often asked whether people should turn off their heating completely and replace it with electric heaters. Unfortunately, it’s unlikely to be cost effective over long periods of time.

Portable electric heaters use electricity to warm the air by convection, either with an exposed heating element, or with a radiator design that transfers heat from the element through a system of fins.

They are great at providing a quick heating fix for a short period of time, such as for a 10-minute blast on a particularly freezing morning. And if your central heating system isn’t working, they’re reliable back-ups.

It’ll take a portable heater between 15 – 30 minutes to raise the temperature of a medium-sized room by 10ºC at full blast. After that it will toggle on and off as needed to maintain temperature, based on its thermostat.

Remember that you pay for energy by the unit. With the current price cap, electricity is much more expensive than gas. So be prudent when you use your electric heater in place of gas.

They usually have rated outputs of 2 or 3kW – that’s how many they’d get through in an hour on full blast. For reference, that’s about the same amount of energy as a kettle. Heaters do generally have settings that let them run at lower outputs too.

If you’re on a standard variable tariff, the average unit price for dual fuel customers is 34p per/kWh for electricity and 10.3p per/kWh for gas. That means that a 2kW portable heater at its full output would use 34p of electricity every half an hour.

If you’re short on cash, there are things you can do right now to plug in gaps in your home and hold onto your heat.

You can draught proof any gaps in your home, whether that’s keyholes, postboxes, door cracks, cavities near doors and windows, or gaps around electrical outlets and pipes. Just remember that homes do need some ventilation, so make sure you leave any purpose-built vents clear, such as window trickle vents or grills in wodden flooring.

Draught-proofing may involve putting down tape or a draught excluder where there’s a draft. Even something basic like a door snake is a help in the war against heat loss. Many of these solutions cost less than a tenner, or can be homemade.

Other tools include:

Adhesive weatherproof tape made of PVC or foam to go around doors and windows.

Threshold seals to go on either side of doors.

Letterbox excluders with brush pile material.

Thermoplastic rubber (TPR) to fit flexibly into door and window cavities.

Pillows designed to fit inside an open chimney to block off draughts when it’s not in use.

One visit to a DIY shop can provide you with several small solutions that don’t break the bank and can be installed yourself.

While individual draught-proofing measures are unlikely to save huge sums from your energy bills in isolation, collectively they will make your home feel more pleasant and cosy to be in. You might even find you can comfortably turn your thermostat down a degree.

In the long run, the key way to keep energy bills low is to trap as much as possible of the heat we generate inside our homes.

If you have the money to do it, insulation is a very good long-term investment. As energy bills go up, the time it takes to see a return on your investment becomes shorter. The Energy Saving Trust estimates that having a professional install loft insulation in a typical semi-detached home would cost around £480 in October 2022, but once it’s done you’d save £355 a year on your energy bills. So in less than 18 months you’d be making a saving.

Professional installation in a detached home would cost more – around £630 – but the savings are as much as £590 a year. And you’ll be saving around 1,000kg CO2 emissions from being released.

So it’s a win-win: you’ll waste less energy and be able to run central heating more cheaply – and break even relatively quickly.

Plus, you’ll be ready for whatever comes next. The central heating options of the future will operate more cheaply if homes can retain heat. Technology like heat pumps are able to operate efficiently because they’re designed for well insulated properties.

Floor insulation usually comes next, and it can reportedly reduce heat loss by 15%.

Cavity wall insulation is useful for properties built in the last century. It’s injected into the gap between your outer and inner walls.

Solid wall insulation can be placed within or outside a wall that’s not eligible for cavity wall insulation. It’s very expensive to install, so a longer term investment.

The energy efficiency of your home or of the home you’re renting is quantified by an EPC certificate. Find out how to get assessed and what the ratings mean here.

10. Update windows with double glazing or alternatives

Windows are a source of heat loss in any home. But if you have single glazing, you’ll notice you need much more energy to heat your home sufficiently. Double or even triple-glazing windows will reduce your heating needs dramatically.

Installing A-rated double glazing could save between £95 and £115 a year on the heating bill of a typical home. However, it doesn’t come cheaply.

We ask Which? members to rate the double glazing companies they’ve actually used.

If you need a quick fix and don’t have the money to spend, window foam seal, foam sealant or metallic brush strips can all help.

We’ve tested secondary glazing film in the past, like clingfilm for your windows, but we thought it wasn’t very resilient. It also needed re-stretching with a hair dryer periodically.

Thick curtains across windows can make a big difference too. Drawing them creates a barrier between your room and the elements and keeps your heat inside.

11. Explore home grants

If you’re replacing your heating system, the government’s Boiler Upgrade Scheme helps you to decarbonise with a heat pump if your home has no outstanding insulation recommendations.

With the latest price cap, a heat pump needs to run at an efficiency of 280% to have parity with a gas boiler’s running costs. Heat pumps can run at 300-400% efficiency, so they can prove cheaper to run.

Other grants can help if you’re in a vulnerable situation, such as:

Cold weather payment to top-up your energy bills during cold snaps.

Winter fuel payment to help people born before September 1955 pay their energy bills.

Fuel Direct lets you deduct essential bills directly from income support, Universal Credit and other assistance available to you. The amount is decided by Jobcentre Plus or your pension centre.

The government’s 2022 Energy Price Guarantee and Energy Bill Support Scheme will both provide households in the UK with a bit of extra help this winter.

{kind=link}

{kind=link}