Tax paid on pints and other drinks on tap in over 38,000 UK pubs is now up to 11p cheaper than their supermarket equivalents

The new Brexit Pubs Guarantee will keep it this way for good

Alcohol duty now simplified so drinks are taxed by strength, lowering duty on supermarket shelves for many UK favourites including bottles of pale ale, pre-mixed gin and tonic, and prosecco

Over 38,000 UK pubs and bars have seen a tax cut on the pints they pull from today as the government’s alcohol duty changes take effect.

The duty paid on drinks on tap in pubs will be up to 11p lower than at the supermarket. The changes are designed to help pubs compete on a level playing field with supermarkets, so they can continue to thrive at the heart of communities across the UK. The Brexit Pubs Guarantee announced in the Chancellor’s Spring Budget secures the pledge that pubs will always pay less alcohol duty than supermarkets going forwards.

It comes as other landmark changes to the alcohol duty system also come into effect today, which see drinks taxed by strength for the first time and a new relief – named Small Producer Relief – to help small businesses and start-ups create new drinks, innovate and grow.

Today’s changes have automatically lowered the duty in shops and supermarkets on many of the UK’s favourites including certain bottles of pale ale, pre-mixed gin and tonic, hard seltzer, Irish cream, coffee liquor and English sparkling wine, amongst others.

Prime Minister Rishi Sunak said: “I want to support the drinks and hospitality industries that are helping to grow the economy, and the consumers who enjoy the end result.

“Not only will today’s changes mean that that the price of your pint in the pub is protected, but it will also benefit thousands of businesses across the country.

“We have taken advantage of Brexit to simplify the duty system, to reduce the price of a pint, and to back British pubs.”

Jeremy Hunt, Chancellor of the Exchequer, said: “British pubs are the beating heart of our communities and as they face rising costs, we’re doing all we can to help them out. Through our Brexit Pubs Guarantee, we’re protecting the price of a pint.

“The changes we’re making to the way we tax alcohol catapults us into the 21st century, reflecting the popularity of low alcohol drinks and boosting growth in the sector by supporting small producers financially.”

The three alcohol duty changes that have taken effect today are only possible thanks to the UK’s departure from the EU and the guarantees set out in the Windsor Framework.

The previous duty system was complex and unfair but now that the UK is free to set excise policy to suit its needs, the government has brought about common-sense reforms in order to support wider UK tax and public health objectives.

Brexit Pubs Guarantee

Over 38,000 UK pubs will benefit from lower alcohol tax on the drinks they pour from tap from today. This is because the government has expanded Draught Relief, which effectively freezes or cuts the alcohol duty on the vast majority of these drinks. This is to protect pubs, who are often undercut by supermarket competitors.

It means that the duty they pay on each drink poured from draught, such as pints of beer and cider, will be up to 11p cheaper than in supermarkets. The government has pledged that the duty pubs and bars pay on these drinks will always be less than retailers, known as the Brexit Pubs Guarantee.

This tax reduction is part of a wider shake up of the alcohol duty system which also comes into effect from today – the biggest in 140 years.

A simpler, more modern alcohol duty system

The alcohol duty reforms were announced at the Autumn Budget in 2021. The reforms pledged to modernise and simplify a duty system that had not been changed in 140 years, only possible as the UK has left the EU.

The key changes are:

All products taxed in line with alcohol by volume (ABV) strength, rather than different duty structures for different drinks

Fewer main duty rates, from 15 to 6, to make it easier for businesses to grow and operate

There will be lower taxes on lower alcohol products – those below 3.5% alcohol by volume (ABV) in strength – a huge growth area in the drinks industry

All drinks above 8.5% ABV will pay the same rate regardless of product type This will mean that many UK favourites will see duty reductions. Irish cream will drop by 3p, cans of 5% ABV ready-to-drink spirit mixers by 6p, Prosecco by 61p and 500ml 3.4% pale ale by 20p a bottle.

New tax relief to encourage small producers to make new drinks

The UK alcoholic drinks market reached just under £50 billion in 2022, up 6% year on year and is expected to continue to grow – sales are forecast to reach £60.9 billion in 2026. The UK government is laser-focused on continuing this burgeoning success.

The government is introducing Small Producer Relief effective from today, which replaces and extends the previous Small Brewers Relief scheme.

This allows small businesses who produce alcoholic products with an ABV of less than 8.5% to be eligible for reduced rates of alcohol duty on qualifying products.

The new tax relief scheme promotes innovation in the drinks sector, giving small producers the financial freedom to experiment with new types of drink and grow their business. It also supports the modern drinking trend of lower alcohol beverages.

New requirements on banks will protect freedom of expression

New rules will give consumers greater confidence to challenge account closures

Changes available because of Brexit and recent government legislation

Banks will be forced to explain and delay any decision to close an account under new rules, protecting freedom of expression.

The Government has stepped in to address fears that banks are terminating accounts because they disagree with someone’s political beliefs.

The changes will increase the notice period to 90 days – giving customers more time to challenge a decision through the Financial Ombudsman Service, or find a replacement bank.

Banks will also be required to spell out why they are terminating a bank account – boosting transparency for customers and aiding their efforts to overturn decisions.

The changes announced today can only be made due to new powers in the Financial Services and Markets Act 2023, which give Britain control of its financial rulebook following Brexit.

Economic Secretary to the Treasury, Andrew Griffith, said:“Freedom of speech is a cornerstone of our democracy, and it must be respected by all institutions.

“Banks occupy a privileged place in society, and it is right that we fairly balance the rights of banks to act in their commercial interest, with the right for everyone to express themselves freely.

“These changes will boost the rights of customers – providing real transparency, time to appeal and making it a much fairer playing field.”

The proposed changes follow a call for evidence launched in January, following PayPal’s temporary suspension of several accounts last year. It found that changes were needed to ensure the right balance is being struck between protecting customers, and providers’ rights to manage commercial risk.

They require secondary legislation, which will be delivered through the powers granted in the Financial Services and Markets Act 2023, as part of the Government’s programme in building a Smarter Regulatory Framework for UK financial services.

This runs alongside separate plans to clarify in legislation the requirements for Politically Exposed Persons (PEPs), and a review into whether these are being applied proportionately by financial institutions.

These steps were commissioned by Parliament last month as part of the Financial Services and Markets Act 2023; and the FCA will set out how they intend to conduct the review by the end of September.

Interactive guide expected to help staff spot and tackle economic abuse

95% of women who experience domestic abuse report experiencing economic abuse

Treasury minister calls for experts to provide feedback on the guide

UK businesses and charities are set to benefit from a free interactive guide to help their staff spot and tackle economic abuse when speaking to customers over the phone, Financial Secretary to the Treasury Victoria Atkins has announced today.

The interactive guide, which will be available widely later this year, is being released to 30,000 HMRC staff today to help them spot the signs and create an appropriate environment for victims to disclose their experiences. It builds on the government’s Economic Abuse Toolkit, released earlier this year.

Victoria Atkins met with staff and survivors at Advance charity’s West London Women’s Centre today to mark the announcement and was joined by former Love Island contestant and domestic abuse campaigner Malin Andersson.

The minister ran through an early demo of the tool with attendees at the visit to drum up momentum as she called on experts to work with HMRC to get the online tool right, before they distribute it freely online later this year.

By increasing the awareness of staff in government, business and charities of economic abuse, the government hopes the new interactive tool will play its part in stopping violence against women and girls, to build stronger communities for future generations.

Financial Secretary to the Treasury Victoria Atkins said: “The government passed the landmark Domestic Abuse Act and I am determined to build on that commitment to help victims.

“Economic and financial abuse can be less understood than other forms of domestic abuse, which is why it is vital organisations share best practice with one another whenever they can.

“That is why I’ve asked HMRC to work with charities and experts over the summer to produce a publicly available interactive guide which staff from any organisation which speaks to customers will be able use.”

Economic abuse, which domestic violence charity Refuge estimates 16% of adults in the UK have experienced, is when an individual’s ability to acquire, use and maintain economic resources are taken away by someone else in a coercive or controlling way.

Internal guidance has been distributed to 30,000 HMRC staff today to help front line staff spot victims of economic abuse when speaking to them over the phone. It will help them understand the different types of economic abuse, as well as what signs and characteristics to look out for.

The aim is for this guidance, with support from industry, charities and experts over the summer, to be turned into a free interactive tool to support businesses and organisations whose employees also speak to customers daily.

Malin Andersson said: ““We need everyone to work together if we’re going to be able to stamp out domestic abuse once and for all, so it’s fantastic to see an initiative which will make a difference by training so many people, from businesses and charities, to recognise economic abuse.”

Minister Atkins will also introduce the early demo of the interactive guidance to representatives from the financial services sector and charities at a roundtable later today, where she will hear more about what the sector is doing to tackle economic abuse and what more can be done.

By working with stakeholders to develop and tailor it, the government wants the interactive guidance to reflect the real-world experiences of victims.

Niki Scordi, Advance’s CEO said: ““Understanding the behaviours of domestic abusers and their continuous attempts to intimidate and control survivors, mainly women and children, long after they leave the abusive home is vital.

“This includes control through economic and financial means, such as child support, school fees, bank accounts, loans and access to employment.

“Supporting survivors with specialist Domestic Abuse Advocates in the community and charities like Advance is essential to help change, and sometimes save, the lives of those devasted by domestic and economic abuse.”

The internal guidance distributed by HMRC to its staff today comes hot off the heels of the Economic Abuse Toolkit released in January 2023, which aims to help public sector organisations train staff to identify economic abuse.

Specialist charity Surviving Economic Abuse (SEA), which was one of the organisations which contributed to the Toolkit, has seen a 150% increase in its website user numbers over the past two years (April 2021 5200 users. April 2023 13,000 users).

SEA research also found seven in ten front-line professionals reported the number of victims of economic abuse coming to their organisation for help had increased since the start of the pandemic. By the end of the first lockdown, SEA found one in five women were planning to seek help around welfare benefits.

Tackling domestic abuse is a government priority and improving the response to economic abuse is integral to this. For the first time in history, economic abuse is now recognised in law as part of the statutory definition of domestic abuse included in the Domestic Abuse Act 2021. This is in recognition of the devastating impact it can have on victims’ lives.

Dr Nicola Sharp-Jeffs OBE, CEO and founder of Surviving Economic Abuse said: “Economic abuse is an insidious and often invisible form of control, one which can trap a victim-survivor in a relationship with an abuser and leave them feeling like there is no escape.

“This form of abuse can create dependency on an abuser by restricting their access to economic resources, or instability if the survivor is forced to cover all household costs. It causes long lasting harm including debt and bad credit, so that even when someone manages to leave, these effects can follow them around for the rest of their lives, often preventing them from moving on safely.

“We know that victim-survivors are more likely to disclose economic abuse to their bank than they are to the police.

“It is crucial that frontline employees – whether they work in the public or private sector – are trained to understand economic abuse and how abusers might use their service to continue to control a victim.

“It is vital they are given the knowledge and the tools to spot the signs of economic abuse, develop specialist responses and feel confident signposting a survivor to broader support. The right response can be life changing.

“We’re delighted to see the Treasury take this important step to ensure victim-survivors of economic abuse get a good response whoever they speak to. We look forward to working together to ensure this new interactive guide helps organisations effectively respond to economic abuse.”

Businesses across the UK can take advantage of the Chancellor’s capital allowances package from today as the new business tax year begins.

The new business tax year comes in today 1 April 2023, with a new regime to boost investment and spur UK growth

£27 billion cut to corporation tax, via Chancellor’s new full expensing policy, expected to boost investment by 3% in each of the next three years

Other tax changes coming into force include more business rates relief, extension to the fuel duty cut and a £450 income tax cut for carers.

The package, announced at Spring Budget, comprises 100% full expensing and a 50% first-year allowance. It will mean the UK has the most generous capital allowance regime in the OECD worth £27 billion over the next three years, amounting to an effective £9 billion a year tax cut for companies.

The OBR expects this regime to boost investment by 3% over three years.

To mark the milestone, Financial Secretary to the Treasury visited Brompton Bikes in Greenford, London, who’ll be using full expensing to stimulate their growth.

Victoria Atkins, Financial Secretary to the Treasury, said: “We are determined to make the UK the best place in the world to do business, which is why from today businesses can start to benefit from the raft of tax cuts on offer to boost their growth.

“With full expensing, the more a company invests the less tax they’ll pay, and I encourage companies of any size to take full advantage of this world-leading reform.”

With the new 25% corporation tax rate coming in for the top 10% most profitable companies from today, and the super-deduction ending yesterday, the Chancellor used his Spring Budget to ensure that the UK’s tax system fosters the right conditions for enterprise, investment and growth.

Full expensing lets companies deduct 100% of the cost of certain plant and machinery investments from their profits before tax. It is available from 1 April 2023 to 31 March 2026. It provides the same generosity as the super-deduction, saving firms up to 25p in every £1 of qualifying investment and is for main rate assets – such as construction, warehousing and office equipment.

The 50% First-Year Allowance lets companies deduct 50% of the cost of other plant and machinery, known as special rate assets, from their profits during the year of purchase. This includes long life assets such as solar panels and lighting systems.

Minister Victoria Atkins visited Brompton Bikes in Greenford this week to see how these capital allowances will be used to help the firm invest and grow. The minister toured their factory, viewing a brand new state-of-the-art Autobraze machine and the production line. She also met a selection of 15 trainees currently on Brompton’s training programme.

Phill Elston, Operations Director at Brompton Bicycle, said: “The announcement of a super deduction replacement is great news for us. In previous years it has meant we could invest significantly in our production capabilities, upgrading equipment and building a more progressive factory; which has seen us move from making circa. 45,000 bikes per year in 2019, to around 100,000 bikes per year in 2022.

“Our mission is to improve how people travel around cities, which in turn creates happier communities, and the new expensing scheme helps to accelerate that goal.”

Other tax measures taking effect today include new domestic and ultra-long Air Passenger Duty bands.

For passengers flying in economy class, the new domestic band will be set at £6.50, a 50% cut to bolster UK-wide connectivity, while the new ultra long-haul band will be set at £91, meaning those who fly the furthest will pay the greatest level of duty.

Transport Secretary Mark Harper said: “Transport binds the United Kingdom together, and this cut to Air Passenger Duty will make travelling between our family of nations easier than ever.

“Boosting transport links between our four nations sustains jobs, creates opportunities and is an essential part of this Government’s plan to grow the economy.”

Further tax measures include:

To help household budgets further, the planned 11 pence rise in fuel duty has been cancelled, maintaining last year’s 5p cut for another twelve months, saving a typical driver another £100 on top of the £100 saved so far since last year’s cut.

More business rates relief, as part of the Chancellor’s £13.6 billion package from 2022’s Autumn Statement. This includes the freezing of the multiplier and the introduction of 75% relief for retail, hospitality and leisure businesses, helping the high street to thrive and compete with online firms.

Extending creative sector reliefs: theatres, orchestra and museums and galleries will benefit from a further 2 years of tax relief rates of 45%/50%. The museums and galleries exhibitions tax relief sunset clause will be extended for a further 2 years to allow these organisations to fully benefit from the extension of the highest rates.

The Annual Investment Allowance (AIA), an existing measure which also supports business investment, has been increased permanently to £1m today. This covers the investment needs of 99% of UK businesses.

Rebalancing the rates of Research and Development Expenditure Credit and the R&D SME scheme to ensure taxpayers’ money is spent as effectively as possible. As a result, today the UK now offers the joint-highest uncapped headline rate of R&D tax relief support in the G7 for large companies.

The government also committed to considering the case for further support for R&D intensive SMEs, and at Spring Budget announced that from today there will be an increased permanent rate of relief for the most R&D intensive loss-making SMEs. To support modern methods of innovation, for accounting periods beginning on or after today, businesses will also be able to claim for the costs of datasets and cloud computing under the R&D tax reliefs.

Expanding the Seed Enterprise Investment Scheme (SEIS) to help more UK start-ups raise higher levels of finance. This package will help over 2,000 start-up companies access finance.

Expanding the availability and generosity of the Company Share Option Plan (CSOP) scheme which will widen access to CSOP for growth companies and simplifying the process to grant options under the Enterprise Management Incentives (EMI) scheme.

On 6 April 2023 personal tax changes taking effect include removing tax-barriers that the medical community have made clear stop doctors working, delivering on the Prime Minister’s priority to cut NHS waiting lists so people can get the care they need more quickly.

The pensions annual tax-free allowance will increase by 50% from £40,000 to £60,000, the Money Purchase Annual Allowance will rise from £4,000 to £10,000, and the Lifetime Allowance charge will be removed.

The Office for Budget Responsibility estimate around 15,000 individuals will remain in the labour market because of the changes to the annual and lifetime allowances, many of whom will be highly skilled individuals, including senior doctors in the NHS.

Qualifying Carers Relief will be uprated with inflation from 6 April 2023 to representing a £450 per year income tax cut for carers. The uprating increases the amount of income tax relief from £10,000 to £18,140 plus £375-450 per week for each person cared for.

Childcare revolution to expand 30 hours free childcare for children over the age of nine months, alongside boosts to subsidised childcare for parents on Universal Credit, including upfront support.

A £27 billion tax cut for business through radical ‘full expensing’ policy and capital allowances reform which will drive investment and growth.

Measures to ease cost-of-living burden will help more than halve inflation, with extension of Energy Price Guarantee and duties on fuel and a pub pint both frozen.

Major set of reforms to support people into work, removing barriers that stop those on benefits, older workers, and those with health conditions who want to work from working.

Inflation falling, debt down and growth up in Chancellor’s Spring Budget for growth that delivers upon the Prime Minister’s economic priorities.

A revolution in childcare, a £27 billion tax cut for business and a trio of freezes to help families with the cost-of-living headlined the Chancellor’s Spring Budget today, Wednesday 15 March.

Aimed at achieving long-term, sustainable economic growth that delivers prosperity for the people of the United Kingdom, the Spring Budget breaks down barriers to work, unshackles business investment and tackles labour shortages head on.

Chancellor of the Exchequer, Jeremy Hunt said:“Our plan is working – inflation falling, debt down and a growing economy. Britain is on a lasting path to growth with a revolution in childcare support, the biggest ever employment package and the best investment incentives in Europe.”

The Chancellor announced 30 hours of free childcare for children over the age of nine months, with support being phased in until every single eligible working parent of under 5s gets this support by September 2025.

The government will also pay the childcare costs of parents on Universal Credit moving into work or increasing their hours upfront, rather than in arrears – removing a major barrier to work for those who are on benefits. The maximum they can claim will also be boosted to £951 for one child and £1,630 for two children – an increase of around 50%.

The Chancellor went on to set out plans to continue to support households with cost-of-living pressures including keeping the Energy Price Guarantee at £2,500 for the next three months and ending the premium that over 4 million households pay on their prepayment meter, bringing their charges into line with comparable customers who pay by direct debit.

Taken together with all the government’s efforts to help households with higher costs, these measures bring the total support to an average of £3,300 per UK household over 2022-23 and 2023-24.

To help household budgets further, the planned 11p rise in fuel duty will be cancelled, maintaining last year’s 5p cut for another twelve months and saving a typical driver another £100 on top of the £100 saved so far.

The generosity of Draught Relief has also been significantly extended from 5% to 9.2%, so that the duty on an average draught pint of beer served in a pub both does not increase from August and will be up to 11 pence lower than the duty in supermarkets. The commitment to duty on a pub pint being lower than the supermarket has been termed the “Brexit Pubs Guarantee” by the Chancellor, and this change will also be enjoyed by every pub in Northern Ireland thanks to the Windsor Framework.

The Chancellor also set out a comprehensive plan to remove the barriers to work facing those on benefits, those with health conditions and older workers. An increase in the pensions Annual Allowance from £40,000 to £60,000 and the abolition of the Lifetime Allowance will remove the disincentives to working for longer.

A new ‘Returnerships’ skills offer for older workers and more stringent Universal Credit job search requirements also feature in the plan that will boost the UK’s workforce, fill vacancies and support economic growth.

In line with the government’s vision for the UK to be the best place in Europe for companies to locate, invest, and grow, a new policy of ‘full expensing’ will be introduced for the next three years to boost business investment in an effective cut to corporation tax of £9 billion per year.

This makes the UK the joint most competitive capital allowances regime in the OECD and the only major European economy to have such a policy. The independent Office for Budget Responsibility (OBR) forecast that this will increase business investment by 3% for every year it is in place.

Mr Hunt signalled an intention to make this scheme – which covers equipment for factories, computers and other machinery – permanent when responsible to do so.

Accompanying forecasts by the OBR confirm that with the package of measures Mr Hunt set out today, the economy is on track to grow with inflation halved this year and debt falling – meeting all of Prime Minister Rishi Sunak’s economic priorities. This comes alongside the confirmation that there are no new tax rises within the Spring Budget.

Childcare

Significant reforms to childcare will remove barriers to work for nearly half a million parents with a child under 3 in England not working due to caring responsibilities, reducing discrimination against women and benefitting the wider economy in the process.

30 hours of free childcare for children over the age of nine months with working parents by September 2025, where eligibility will match the existing 3-4 year-old 30 hours offer.

This will be introduced in phases, with 15 hours of free childcare for working parents of 2-year-olds coming into effect in April 2024 and 15 hours of free childcare for working parents of nine months – 3 years old children in September 2024.

The funding paid to nurseries for the existing free hours offers will also be increased by £204 million from this September rising to £288 million next year.

Schools and local authorities will be funded to increase the supply of wraparound care, so that parents of school age children can drop their children off between 8am and 6pm – tackling the barriers to working caused by limited availability of wraparound care.

Childcare costs of parents moving into work or increasing their hours on Universal Credit paid upfront rather than in arrears, with maximum claim boosted to £951 for one child and £1,630 for two children – an increase of around 50%.

In recognition of both the importance and short supply of childminders, incentive payments of £600 will be piloted from Autumn of this year for those who sign up to the profession (rising to £1,200 for those who join through an agency) to increase the number available and increase choice and affordability for parents.

Employment

The Chancellor set out a comprehensive plan to help people move into work, increase their hours, and extend their working lives, including for those on benefits.

The Lifetime Allowance charge will be removed before being abolished altogether, removing barriers to remaining in work and simplifying the tax system by taking thousands out of the complexity of pension tax.

The Annual Allowance will be increased from £40,000 to £60,000, incentivising highly-skilled workers to remain in the labour market. As a result of the pensions tax measures announced today, an estimated 80% of NHS doctors will not receive a tax charge with respect to accruals under the 2015 NHS career average scheme.

A new ‘Returnerships’ apprenticeship targeted at the over 50s will refine existing skills programmes to make them more accessible to older workers, giving them the skills and support they need to find a recognisable path back into work.

The midlife MOT offer will be expanded and improved to ensure people get the best possible financial, health and career guidance well ahead of retirement. There will be an enhanced digital midlife MOT tool and an expansion of DWP’s in person midlife MOTs for 50+ Universal Credit claimants, aiming to reach 40,000 per year.

A DWP White Paper on disability benefits reform will herald the biggest change to the welfare system in the past ten years, to make sure it better meets the needs of those on disability benefits in Great Britain. This includes removing the Work Capability Assessment, meaning the majority of claimants will now have to do one health assessment rather than two. Reforms will also support claimants to try work without fear of losing their financial support.

A new voluntary employment scheme for disabled people and those with health conditions called Universal Support will be funded in England and Wales. The government will spend up to £4,000 per person to find them a suitable role and cater to their needs, supporting 50,000 places per year once fully rolled out.

Over £400 million plan to tackle the leading health causes keeping people out of work, with investment targeted at services for mental health, musculoskeletal conditions, and cardiovascular disease.

Strengthening work search and work preparation requirements for around 700,000 lead carers of children aged 1-12 claiming Universal Credit in Great Britain.

Increasing the Administrative Earnings Threshold (AET) – which determines how much support and Work Coach time a claimant will receive based on their earnings – for an individual claimant, from the equivalent of 15 to 18 hours at National Living Wage and removing the couples AET in Great Britain. Over 100,000 non-working or low-earning individuals will be asked to meet more regularly with their Work Coach for support to move into work or increase their earnings.

The application and enforcement of the Universal Credit sanctions regime will be strengthened, by providing additional training for Work Coaches to apply sanctions effectively, including for claimants who do not look for or take up employment, and automating administrative elements of the sanctions process to reduce error rates and free up Work Coach time.

Elsewhere, international talent will be attracted through a new migration package that includes adding five construction occupations to the Shortage Occupation List and expanding the range of short-term business activities that are covered under the UK’s six-month business visit visa offer.

Enterprise

The Chancellor put forward a plan to boost innovation, drive business investment and hold down energy costs.

A ‘full expensing’ policy introduced from 1 April 2023 until 31 March 2026 and an extension to the 50% first-year allowance in the same period – a transformation in capital allowances worth £27 billion to businesses over three years.

A £500 million per year package of support for 20,000 research and development (R&D) intensive businesses through changes to R&D tax credits.

Generous reforms to tax reliefs for the creative sectors will ensure theatres, orchestras, museums and galleries are protected against ongoing economic pressures and even more world-class productions are made in the UK.

The Medicines and Healthcare products Regulatory Agency (MHRA) will receive £10 million extra funding over two years to maximise its use of Brexit freedoms and accelerate patient access to treatments. This will allow, from 2024, the MHRA to introduce new, swift approvals systems, speeding up access to treatments already approved by trusted international partners and ground-breaking technologies such as cancer vaccines and AI therapeutics for mental health.

All of the recommendations from Sir Patrick Vallance’s review into pro-innovation regulation of digital technologies, published alongside Spring Budget today, are to be accepted.

£900 million of funding for an AI Research Resource and an exascale computer – making the UK one of only a handful of countries to have one – and a commitment to £2.5 billion ten-year quantum research and innovation programme through the government’s new Quantum Strategy.

Levelling Up

To level up growth across the UK and spread opportunity everywhere, local communities will be empowered to command their economic destiny.

Greater responsibility for local leaders to grow their local economy.

Over £200 million for high quality local regeneration projects in areas of need, from the transformation of Ashington Town Centre to a skills and education campus in Blackburn.

Over £400 million for new Levelling Up Partnerships for twenty areas in England most in need of levelling up, such as Rochdale and Mansfield.

Business rates retention expanded to more areas in the next Parliament.

Delivering trailblazer devolution deals for the West Midlands and Greater Manchester Combined Authorities that include single multi-year settlements for the next Spending Review, alongside a commitment to negotiate further devolution deals in England.

12 Investment Zones across the UK including four across Scotland, Wales and Northern Ireland

£8.8 billion over the next five-year funding period for a second round of the City Region Sustainable Transport Settlements.

Many of today’s decisions on tax and spending apply in Scotland, Wales and Northern Ireland.

As a result of decisions that do not apply UK-wide, the Scottish Government will receive around an additional £320 million over 2023-24 and 2024-25, the Welsh Government will receive an additional £180 million, and the Northern Ireland Executive will receive an additional £130 million.

Scottish Secretary Alister Jack said: “Today the Chancellor has set out a Budget which continues cost of living support and will deliver sustainable, long-term growth, helping us halve inflation and reduce our national debt.

“Maintaining the Energy Price Guarantee until June will save the average family £160 a year and gives certainty over their bills until summer. We’ve also made changes to Universal Credit to help people get back to work.

“Other UK Government direct investment in Scotland includes £8.6 million for Edinburgh’s world-class festivals, more than £1 million for five new vital community ownership projects, and investment in Scotland’s innovative high tech sector. The Chancellor has also confirmed there will be Investment Zones in all parts of the UK, building on Scotland’s two new Freeports.”

STAKEHOLDER REACTION: CHILDCARE

Chris McCandless, European CEO, Busy Bees Nurseries said:“Today’s announcement is a positive step for children, parents and providers of early years education.

“At Busy Bees, we know the difference that a great early education makes to a child’s future and look forward to working with the government on implementing these changes. It’s now critical to ensure this increased funding is used to deliver the most favourable impact on parents and staff, and to generate the desired benefit for the economy.”

Justine Roberts, founder and CEO, Mumsnet said:“This is a hugely significant intervention from the Chancellor. Mumsnet has been campaigning for years for childcare to be recognised as the vital national infrastructure that it is, and to see it at the centre of today’s Budget is testament to the work we have done to drive it up the political agenda.

“We know from our users that the current gap in support between the end of maternity leave and a child’s third birthday means for many women it is simply not financially feasible to return to work.

“This has long term consequences for their careers and pensions, as well as slowing economic growth, so it is welcome that the government has listened to us on this issue and set out a plan to address it.

“We are also pleased that the Chancellor has heeded calls to reform the childcare element of Universal Credit so that it no longer forces parents into debt, and has announced changes to increase the supply of wraparound care to better reflect the needs of working parents.

“That said, there are clearly concerns about whether the funding allocated is actually sufficient to deliver this expanded provision. We would urge the Chancellor to engage with these concerns immediately in order to ensure the offer to families that he has outlined can actually be delivered.”

Joeli Brearley, CEO and Founder, Pregnant Then Screwed said:“The budget announcement on childcare today was the main event in the Spring budget which just shows the power of collective action and we are elated to hear that the childcare sector will now receive a significant investment, and that universal credit will be paid upfront, these schemes will change parents’ lives.

“Parents of young children felt ignored, but this will restore their faith in democracy so we thank Minster’s for hearing our cry and bridging the gap for mothers from the end of maternity leave so that they are supported to be able to work.

“It is imperative that the right investment is made to properly fund the roll out of these free childcare hours. We need to ensure that there is a clear and remunerated strategy to attract more educators into the sector, to retain those workers and to offer progression opportunities.

“Without a workforce plan providers will continue to be forced to close, and increasing ratios will add pressure to an underpaid workforce. The CBI estimates that to do what the government is planning costs £8.9 billion not £4 billion, so we need to see the detail as to how this money is being distributed.

“Free childcare from 9 months is brilliant, but only if there are childcare settings to be able to access this care, without the correct funding and enough childcare staff there won’t be.

“We feel really positive about the future though, and many of the parents we work with feel the same.”

STAKEHOLDER REACTION: CROSS CUTTING

Michael R. Bloomberg, Founder, Bloomberg LP and Bloomberg Philanthropiessaid:“I am a very big believer in the future of the UK’s economy, including for the financial services sector.

“Whatever the daily headlines, the UK has an enormous amount going for it and even more potential. Bloomberg continues to make major investments here and we remain optimistic that the U.K.’s high-tech, high-skilled economy is well-positioned for long-term growth.”

Matthew Fell, Interim Director-General, CBI said:“This Budget is a strong second act in the Chancellor’s plan for stability and growth.

“The CBI called for action on people and productivity and the government has delivered support for both. Measures to help households and businesses will secure the growth we need to boost living standards for all.

“Full capital expensing will keep the UK at the top table for attracting investment and puts us on an essential path to a more productive economy.

“Boosting childcare provision is a big win for businesses struggling to recruit and retain, and parents balancing care and career needs.

“Alongside support for occupational health to help people stay in work, it shows the Chancellor is listening to business on reducing economic inactivity and easing a tight labour market.

“New investment zones focused on economic clusters will drive growth across the country and increased support for quantum is a further step towards making the UK the science and technology superpower it aspires to be.

“Giving the go-ahead to carbon capture and nuclear are important steps that will keep the UK’s green growth story on track. With our closest rivals raising their game on green growth, moving further and faster in the months ahead is key.”

Kate Nicholls, Chief Executive, UKHospitality said:“With hospitality businesses continuing to struggle with vacancies running at 56% higher than pre-pandemic levels, the measures announced today are significant in incentivising people back into work and hopefully alleviating crippling labour shortages. The wider economic forecasts also give us encouragement that consumer confidence and spending are in for an upturn, albeit over time.

“The significant reforms to childcare and the measures to help the over 50s re-enter the workforce are both areas on which UKHospitality has been calling for action and we’re pleased the Chancellor has recognised the help it can offer tackling the enormous vacancies in hospitality.

“Maintaining current levels of energy support to consumers, freezing fuel duty and inflation reducing will help hard-pressed households and increase disposable income, which will be a huge boost for venues in desperate need of trade.

“This will be particularly needed as the sector is still set to see huge energy price increases when current support ends in April, which unfortunately was not addressed. It remains the case that we need to see urgent action on the market failures identified by Ofgem in its non-domestic review update yesterday. The current timeline of further action by the summer is not good enough.

“The reduction in draught duty is positive and we hope this will incentivise more visits to our pubs, restaurants and hotel bars. Addressing draught duty is a good start and I would urge the Government to consider rolling out this type of tax cut across the wider drinks market.

“With duty primarily paid by suppliers, such as breweries, it’s essential that any benefit is passed through to venues to help deliver the Government’s objective of reducing inflation and growing the economy.”

STAKEHOLDER REACTION: EMPLOYMENT

Dr Vishal Sharma, Chair, British Medical Association (BMA) Pensions Committee and Chair of the Consultants Committee said: “Today’s announcement is an incredibly important step forward and the result of year after year of lobbying and campaigning for changes to pension taxation by the BMA.

“The scrapping of the lifetime allowance will be potentially transformative for the NHS as [the majority of] senior doctors will no longer be forced to retire early and can continue to work within the NHS, providing vital patient care.

“The rise in the annual allowance will mean far fewer doctors will receive large punitive pension tax bills and will significantly reduce the perverse incentive to reduce hours due to pension tax. It’s also very welcome the Government has committed to addressing the anomaly of ignoring any negative pension growth and rectifying this will ensure NHS staff can appropriately utilise their full annual allowance.”

STAKEHOLDER REACTION: ENTERPRISE

Steve Bates OBE, CEO, The BioIndustry Association (BIA)said:“This is a huge boost for biotech companies across the UK developing new medicines and improving healthcare for patients.

“Our research-intensive industry is a key growth area for Britain’s economy. The Chancellor is rightly focusing UK taxpayer support to enable life science entrepreneurs to crowd in more private investment, help keep the UK at the cutting-edge of international science, and create new high-value jobs across the UK.”

A GSK spokesperson said:“The UK has a big opportunity in life sciences, to improve patient care and health outcomes, and support economic growth. Today’s Budget recognises this and includes important measures to help realise this opportunity.

“We welcome the new model and funding for the MHRA to accelerate access to innovative treatments and vaccines for patients and improve the attractiveness of the UK for investment in life sciences research. Giving the MHRA the resources and tools to become a leading global regulator is a key part in capitalising on the UK’s potential in life sciences.

“We also welcome the new scheme on R&D tax credits targeted towards the most research intensive SMEs – this should have a positive impact on the wider UK life science ecosystem.”

Tony Hickson, Chief Business Officer, Cancer Research UK and Cancer Research Horizons said:“The government’s decision to revisit the R&D tax credits for SMEs in the Budget is a shot in the arm to oncology start-ups across the UK.

“At a time when they are facing tough economic challenges, early stage companies need this vital support to accelerate discoveries from the lab to the clinic.

“Spin-out companies play a vital role in translating Cancer Research UK-funded research from the lab into life-saving treatments. Today’s decision by the Chancellor is a vote of confidence in the UK’s outstanding life sciences start-up community, creating the opportunities needed to develop new tests, medicines and advances in healthcare for cancer patients.”

Kerry Baldwin, Founder, Managing Partner IQ Capital said: “The Chancellor’s focus on economic growth, science and innovation are the right priorities and venture has a central role to play in building the economy of the future.

“The announcements of the Long term Investment For Technology and Science (‘LIFTS’) and the 10-year extension and further support to British Patient Capital are positive and central to the UK becoming a science and technology superpower.

“The new regime that will allow innovative SMEs to claim greater R&D tax relief is also welcome, especially for R&D intensive companies creating the next wave of scientific breakthroughs in deeptech and life sciences.”

Julian Bellamy, Managing Director, ITV Studios said:“The UK is a world leader in film and TV and the package of measures announced by the government today, particularly the increase in the expenditure credit and the maintenance of the qualifying HETV expenditure threshold at £1m, will help enable the sector to continue to thrive.

“We’re very grateful that the government responded to the concerns of the sector.”

Kate Varah, Executive Director, the National Theatre said: “We are thrilled that the Government has made the vital decision to maintain the higher rate of Theatre Tax Relief.

“In a period where the sector is navigating ongoing financial headwinds, it means the National Theatre and our colleagues in theatres across the UK can continue to make world-class productions of real ambition that delight audiences, provide jobs, stimulate economic growth and cement the UK as a global leader in culture.”

Adrian Wootton OBE, Chief Executive, the British Film Commission said:“Today’s announcement is a real recognition from the Government of the growth and opportunity our UK Film and High-end TV industry presents.

“The UK’s tax reliefs have directly influenced many productions’ decisions to base themselves in the UK, contributing billions of pounds to the economy and hundreds of thousands of jobs across the UK’s nations and regions.

“With increasingly intense international competition, we’re delighted to welcome this package of measures, futureproofing the UK’s film, High-end TV and animation tax credits and our position as a leading global production hub.”

STAKEHOLDER REACTION: COST OF LIVING

Peter Tutton, Head of Policy, StepChange Debt Charity said:“Today’s budget set out vital support targeted at the millions of households facing real financial difficulty following more than a year of this gruelling cost of living squeeze.

“The extension of the Energy Price Guarantee, the end to extra pre-payment meter fees and the extra childcare support announced will make a real difference to struggling households.”

Jack Cousens, Head of Roads Policy, the AA said: “We are pleased the Chancellor has listened to the AA and frozen fuel duty. Not only will this save drivers ‘heavy duty’ pain at the pump, but will help keep the price of goods and services down as they are mainly transported by road.

“Crippling road fuel costs are also a major driver of inflation.”

Maria Booker, Head of Policy, Fair By Design said:“We’re delighted to see the Government ending the prepayment poverty premium. For too long people on prepayment meters have been paying too much for energy.

“Over 4 million people are charged an extra £45 to access energy, an essential service. This is especially shocking in the context of rising energy bills and the cost of living crisis. The extra costs are particularly unfair as many low income consumers use prepayment meters as it helps them budget using cash.”

STAKEHOLDER REACTION: ALCOHOL DUTY

Dr Katherine Severi, Chief Executive, Institute of Alcohol Studies said:“Cuts and freezes to alcohol duty have cost the public purse more than £8 billion over the past 10 years. Today’s announcement by the Chancellor that most alcohol duties will rise by inflation will raise revenue for vital public services.

“We welcome this decision. With alcohol deaths at their highest level on record, now is more important than ever to focus on improving health by tackling cheap alcohol. It’s high time the alcohol industry started paying its way towards the cost of alcohol harm. We urge the Government to continue to prioritise public health by keeping alcohol duty in line with inflation going forward.”

Nik Antona, Chairman, CAMRA said:“The Chancellor has made a welcome move to increase the draught duty rate discount to 11p, which will help pubs compete with the likes of supermarket alcohol.

“However, the lower tax rate is not coming until August, and we must hope that as many pubs as possible will be able to keep their doors open until then. With many parts of the licensed trade struggling to make ends meet, and consumers tightening their belts, hikes in general duty rates are the last thing breweries need, so it’s right that general duty rates have been frozen until the new system is introduced.”

STAKEHOLDER REACTION: LEVELLING UP

Lord Jim O’Neill, Vice-Chair, the Northern Powerhouse Partnership said:“Nearly a decade on from the devolution deal between Greater Manchester and the then Chancellor George Osborne, which helped kickstart the entire Northern Powerhouse project, this feels like a return to the spirit of that period and a new era for metro mayors and local government.

“Single pot settlements and business rate retention will give mayors greater independence and flexibility, allowing them to plan strategically for the long-term. We must open up a clear pathway for other mayoral areas to secure similar powers in the future.

“It will also lay the foundation for us to go further through fiscal devolution and hand more tax powers to accountable local leaders to tackle the productivity gap that has been holding back the North for decades.”

Andy Burnham, Mayor of Greater Manchester said:“This is the seventh devolution deal Greater Manchester has agreed with the government and it is by some way the deepest. This Deal takes devolution in the city-region further and faster than ever before, giving us more ability to improve the lives of people who live and work here.

“I have always been a passionate believer in the power of devolution, and I’ve been in the privileged position of being able to exercise those powers and make a positive difference to people’s lives.

“We’ve worked hard to secure this Deal and have achieved a significant breakthrough by gaining greater control over post-16 technical education, setting us firmly on the path to become the UK’s first technical education city-region; new levers and responsibilities to achieve fully integrated public transport including rail through the Bee Network by 2030; new responsibilities over housing that will allow us to crack down on rogue landlords and control over £150m brownfield funding; and a single block grant that will allow us to go further and faster in growing our economy, reducing inequalities and providing opportunities for all.

“With more power comes the need for great accountability and I welcome the strengthened arrangements announced in the Deal.

“While we didn’t get everything we wanted from the Deal, we will continue to engage with government on those areas in the future. For now, our focus will be on getting ready to take on the new powers and be held to account on the decisions we will be making on behalf of the people of Greater Manchester. Today is a new era for English devolution.”

Andy Street, Mayor of the West Midlands and Chair of the West Midlands Combined Authority (WMCA) said:“This announcement is a major step forward for the West Midlands with significant new powers and funding secured.

“We’re deepening devolution by building on previous deals and further empowering local leadership with the financial autonomy and decision making authority that they are best placed to deploy. No one in Whitehall can understand the West Midlands better than local leaders, and so there is no doubt in my mind that we should be able to shape our own future – which is exactly what this new deal will allow us to do.

“I recently called for an end to the ‘begging bowl culture’ which confined us to regularly submitting bids for various pots of money in competition with other regions. I’m pleased to see that this new devolution deal goes some way to addressing that – giving us guaranteed devolved funding to spend how we choose, akin to what Government departments have currently, and doing away with Whitehall micromanagement.

“Since 2017, we’ve demonstrated a solid track record in building more homes whilst protecting the green belt, improving peoples’ skills to help them find quality work, increasing transport investment sevenfold and tackling the climate emergency. This is why the Government is trusting us and granting us greater responsibility – and accountability – to deliver even more.

“Today is a milestone day for the West Midlands, and I am delighted we have been able to work together as a team to get this Deeper Devolution Deal over the line.”

A ‘missed opportunity’ for meaningful action

Swinney says Spring Budget falls short on vital lifelines

SCOTLAND’s Deputy First Minister John Swinney has described the UK Government’s Spring Budget statement as “another missed opportunity” to help households, businesses and public services through the cost of living crisis.

He said Chancellor of the Exchequer Jeremy Hunt had failed to deploy the full range of powers available to him to mitigate the impact of soaring energy prices and high inflation.

While welcoming a number of individual measures such as the extension of the energy price guarantee – and with a typical household’s monthly energy bills set to rise by almost half from March to April – Mr Swinney said substantive actions such as restoring the Universal Credit uplift were notably absent.

He also called for the UK Government to inflation-proof the Scottish Government’s budget so it can better co-ordinate spending across Scotland.

Mr Swinney said: “This UK Budget is another missed opportunity to take meaningful action to lift families out of poverty, invest in our public services and help businesses so that our economy can grow.

“Instead, the UK Government should have taken more substantive action to increase the Scottish Government’s budget so we can better align spending and deliver for people and organisations right across Scotland.

“While reversal of the planned increase in the energy price guarantee is welcome, with the end of the energy bills support payments, typical household monthly bills will still rise by more than half from March to April, at a time when wholesale energy costs are falling.

“Rising interest rates combined with reduced support means some people are expected to experience a larger fall in living standards this coming year than they have over the last 12 months.

“An uplift on Universal Credit and extending this to legacy benefits would have made a meaningful difference to households struggling to make ends meet.

“The limited additional money for the Scottish Government’s Budget is welcome but will not go far enough and in the long-term our capital funding will fall in real-terms. Without extra funding, we will have to find money from within the Scottish Budget to invest in public services, provide fair pay rises and help people with the cost of living.

“The Scottish Government is doing what it can with its limited powers to ensure people receive the help they need, but the UK Government’s could have done far more to ease the burden affecting so many, demonstrating yet again why Scotland needs the powers of independence.”

TUC: Budget 2023 – was that it?

Today’s budget saw the Chancellor speak about a high-wage and high-skills economy but do nothing to deliver it (writes TUC’s GEOFF TILY). The UK is still in the longest pay squeeze for more than 200 years. And our public services are still run-down and understaffed.

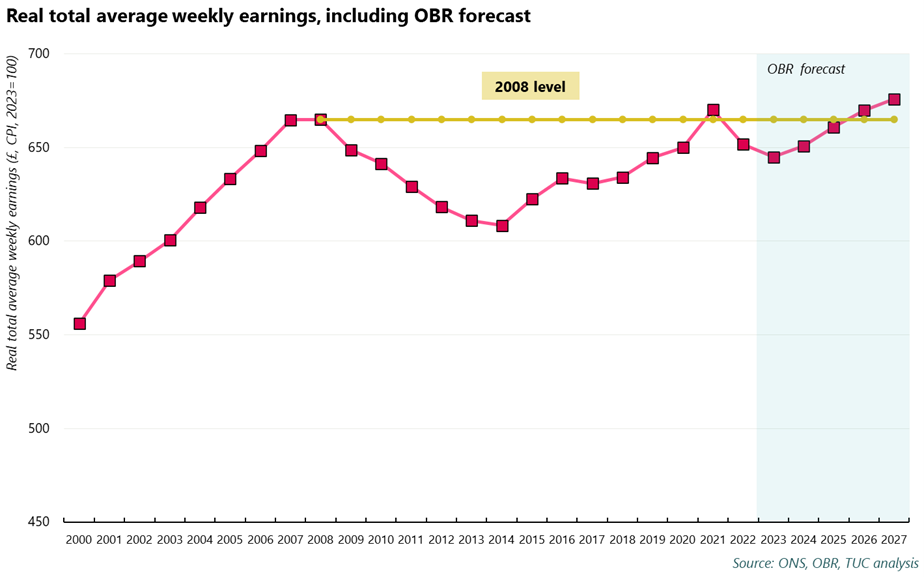

There was no plan to get wages rising across the economy. Real wages will not return to 2008 levels until 2026. And the elephant in the room was the lack of funding for our public services and the pay rises needed to recruit and retain nurses, carers and teachers.

The Chancellor should have announced measures to boost secure jobs, pay and skills. He should have provided a fully-funded workforce plan across our public services to recruit and retain key workers. And he should have set out an investment plan to rebuild our services – from fixing school buildings that are falling apart to restoring public health services. Apart from some long overdue steps forward on childcare, workers across the economy will have looked at this Budget and thought ‘was that it?’

Pay crisis

Appealing to a “high wage high skills economy”, the Conservatives continue to preside over the longest pay crisis in modern history. On current forecasts real pay will fall by 1.0 per cent in 2023, before beginning to grow again in 2024. But even with this growth, real pay will not return to its 2008 level until 2026 – an 18-year pay squeeze that could outlast the government that has spent the past thirteen years taking no action to address it.

This pay squeeze has hit workers’ pockets hard. If real pay had grown by the pre-2008 rate since 2008, workers would’ve been £233 per week better off in 2022 than they were. This gap is set to widen to £304 per week by 2027.

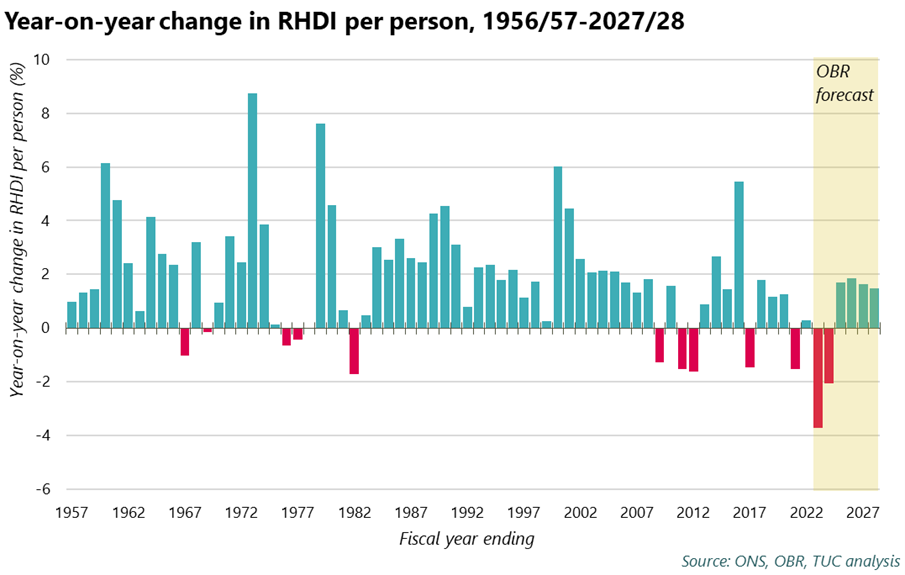

Beyond pay, the OBR forecasts real household disposable income (RHDI) per person, a measure of living standards, to fall by six per cent between 2021/22 and 2023/24. This is the steepest two-year decline since records began in the 1950s.

Before 2010, RHDI per person had only fallen in five of the 54 years since records began. Between 2010 and 2025, it’s set to fall six times.

Unending growth failure

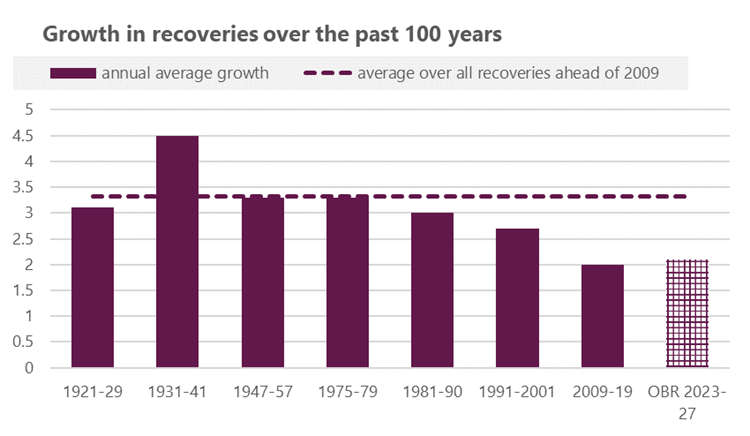

According to today’s OBR forecast, the Chancellor’s ‘plan for growth’ will deliver growth over the next five years that is only only 0.1 percentage point higher than growth between 2009 and 2019 – widely acknowledged as a decade of stagnation. Even if the forecast is delivered, the conservatives will have presided over the two worst recoveries in a century.

The forecast benefits from reduced concerns about recession. But it’s early days on this – the backdrop to his speech is a steep 3.8% decline in the stock exchange today – reacting to newly exposed dysfunction in the financial sector.

And this poor performance will have real consequences for workers. Unemployment will rise from 1.3 million this year to 1.5 million throughout the rest of the forecast.

Failing to deliver

In our Budget statement we asked the Chancellor to invest in public services and the workers that deliver them, and to put workers before wealth.

We asked the chancellor to boost pay across the economy, but astonishingly he did nothing to address the public sector pay crisis.

There was nothing to boost get us on a path to a a £15 minimum wage as soon as possible, or to set up the fair pay agreements we know we need to drive up fair pay across the economy.

We wanted a plan for strong public services and fair taxation:

Battered by inflation and recruitment crises, the chancellor did not mention public services. He offered none of the new funding desperately needed to recruit the nurses, carers and teachers that our public services rely on.

The Chancellor declined to extend the windfall tax on firms profiting from the gas price crisis, even though Big Oil firms fully doubled their profits last year. At the same time, many employers – from small business to big paper mills – have already faced closure due to spiking energy prices. But the Government has declined to extend its energy bills support package for employers.

Long overdue announcements on childcare follow years of union campaigning. But without improved conditions for childcare workers, recruitments and retention challenges could make delivery impossible.

We wanted workers (not the wealthy) protected from hardship

Pressure from unions and broader civil society has worked – the Government agreed to keep the Energy Bills Guarantee at £2,500 for the average household for a further three months, after which energy prices are expected to fall below this level. The Government also finally ended the unfair premium paid on energy by households on pre-payment meters.

But there is nothing in this budget – and in the Government’s existing commitments – to restrict bills sky-rocketing again. No new funding for upgrades to our leaky, draughty homes. And despite announcements to support nuclear energy and carbon capture and storage, there is nothing to expand the supply of clean energy in the next few years.

In spite of the severity of the cost-of-living crisis and the dramatic weakening of provisions over a decade of austerity, the chancellor did nothing on social security protections (beyond the childcare support in universal credit). Instead he further ramped up the already harsh sanction regime for those looking for work and on low earnings.

The work capability assessment will not be missed. But given the government’s track record, we cannot be sure that the new proposals for disabled people will be any better.

Remarkably, however, to fix a quirk in our system of tax relief on pension contributions that pushes some senior doctors into early retirement, the Chancellor scrapped limits on how much individuals can save for retirement tax free over a lifetime.

This indiscriminate measure, together with increases to annual limits, is projected to hand around £4 billion to the wealthiest savers over the next five years. These tax breaks will make it easier for the rich to use pensions as a vehicle for passing on wealth without paying inheritance tax, but do nothing to help most workers save for retirement. With a quarter of over-50s unlikely to achieve even a minimum retirement income, extra incentives should have targeted low earners.

We wanted a plan for sustainable growth that creates decent jobs

The most expensive line in the budget is the announcement of 100% expensing of qualifying capital investment for the next three years. This is predicted by the OBR to cost an average of £9.1 billion per year – over £27 billion in total. The measure means that companies will be able to deduct 100% of qualifying capital investment against their tax bill in the year of investment.

Measure to encourage UK businesses to raise their stubbornly low rates of investment are certainly needed. However, the question with this proposal is whether it will encourage additionality in business investment – or will simply hand public money to companies for investment that would have taken place anyway. Given the huge predicted costs to the scheme, this question is critical to whether it can be judged a success.

The OBR notes that the super-deduction, which this new measure replaces, raised business investment by less than originally expected, saying: “we overestimated its dynamic benefits”. Given the temporary nature of the new measure, the OBR expects it to bring forward investment that is currently planned and to have a smaller peak impact on investment than its predecessor super-deduction.

The measure must be judged by the additionality it creates in terms of levels of business investment and whether this is a sustainable, rather than temporary, effect.

Rather than simply splurging money, the government should reform how business is regulated to encourage long-term, sustainable growth. We need corporate governance reform to encourage companies to prioritise sustainable, long-term investment and decent jobs over short-term shareholder returns.

This means reforming directors’ duties to remove the priority given to shareholder interests and requiring that worker directors comprise one third of the board at large UK companies. These reforms would encourage sustainable business models based on long-term investment and decent work, and would help to ensure that government investment incentives are well used by businesses, with the benefits shared with those who work for them.

And the UK’s manufacturing and process industries were sorely lacking any mention in the Budget. Indeed, when the Chancellor outlined his ambition for the use if Levelling Up investments, the example given as a success was Canary Wharf: hardly hopeful for people who work in real economy jobs in held-back regions now.

The headline commitment to increase defence spending lacked any reference to jobs this spending could generate – meaning any industrial benefit is likely to be offshored once again.

And while the Government did confirm its intention to invest into Carbon Capture, Use, and Storage, this does little to secure the future of the rest of the UK’s heavy industries. Industrial strategy – and a proper strategy to navigate the climate transition, protecting jobs and livelihoods along the way – is still lacking.

‘Was that it?‘ – a Budget with no ambition, more of the same at best, and basically ignoring the most pressing problems facing the UK.

Commenting on the Budget, Jonathan Rolande, spokesman for the National Association of Property Buyers said: “If you were hoping the Budget might make it easier to move home – it hasn’t. Jeremy Hunt has left the UK property market to sort itself out, taking no steps to guide it in any direction whatsoever. The ‘baked-in’ unfairness continues.

“Right now not enough homes are being built, mortgages are up, rents are up and rentals are becoming more scarce. It is almost impossible to rent and save a deposit. There is a growing inequality between those with property (or well-off parents) and those without.

“Many feel they have no hope of ever owning their own home with the benefits and stability that brings

“Mr Hunt has, perhaps for financial reasons or for political expediency taken the much longer-term view. Enabling young parents to return to work will feed through into increased borrowing ability. Increasing pension thresholds will allow the Bank of Mum and Dad to offer higher loans and gifts to their children.

“For the short to medium term, opportunities to level the playing field have been missed. He could have rebalanced Stamp Duty to free up property stock, penalised developers who sit on land waiting for price growth, and offered tax breaks for landlords who insulate their tenant’s homes or offer long-term lets. None are especially expensive and each would have an immediate and positive impact on property buyers and society as a whole.

Mr Rolande added: “The impact of the housing crisis is at the heart of many of the issues that vex the government right now. A lack of homes makes people less tolerant of immigration. Poorly insulated homes are bad for the environment and increase inflation. Disenfranchised younger people feel they have a lesser role to play in society. And many put off having children because they can’t afford the right home, and others cannot pursue dreams of a better job because they can’t afford to live in an area where pay and conditions are better.

That’s why it is all the more surprising that a Conservative has not taken the opportunity to create more homeowners, something generally thought to make people more likely to vote blue.

For me, this Budget will be more about what wasn’t done, than what was. Those who were hoping for good news on housing, will now have to wait another long year to find out what crumbs of comfort might be thrown their way.”

Individuals earning over £300,000 are the secret winners of Chancellor Hunt’s budget

Nimesh Shah, CEO at leading tax and advisory firm Blick Rothenberg said, “The secret winners from Jeremy Hunt’s Budget are individuals earning over £300,000.

“Whilst all the pension headlines are around abolishing the lifetime allowance, hidden away in the detail of Jeremy Hunt’s Budget is an increase to the minimum tapered allowance to £10,000, up from £4,000 – this is the minimum level of tax relievable pension contributions.

“The £6,000 increase will be worth an additional £2,700 of tax relief to someone earning over £360,000. Quite perversely, a minority of very high earners will be some of the biggest winners from today’s Budget announcements.”

Chancellor sets out next stage of the Government’s plan to halve inflation, grow the economy and reduce debt.

Building on the stability he gained from Autumn Statement, Jeremy Hunt will set out next steps to drive economic growth across the UK.

Plan will help ease the cost of living, remove barriers into work to boost incomes, drive business investment, and support new, high-growth industries of the future.

Chancellor of the Exchequer Jeremy Hunt will unveil the next phase of the Government’s plan to halve inflation, grow the economy and reduce debt in his Spring Budget today.

In his first Budget speech as Chancellor, Jeremy Hunt is expected to build on the stability gained at the Autumn Statement, with new measures to support families and businesses with the cost of living, before setting out an agenda to grow the UK economy.

The Chancellor of the Exchequer, Jeremy Hunt is expected to say:“In the Autumn we took difficult decisions to deliver stability and sound money. Today, we deliver the next part of our plan: a Budget for growth.

“Not just growth from emerging out of a downturn. But long term, sustainable, healthy growth that pays for our NHS and schools, finds good jobs for young people, provides a safety net for older people … all whilst making our country one of the most prosperous in the world.

“Today I deliver that by removing the obstacles that stop businesses investing; tackling the labour shortages that stop them recruiting; breaking down the barriers that stop people working and harnessing British ingenuity to make us a science and tech superpower.”

The Government is already protecting struggling families with one-off payments worth £94 billion. After a decade of reforms, people on low incomes can now earn £1,000 a month without paying tax or national insurance thanks to rises in tax thresholds. This has helped to lift two million people out of absolute poverty, after housing costs, including 400,000 pensioners and 500,000 children.

The Chancellor is expected to announce fairness reforms to energy bills, bringing the bills of families on prepayment meters in line with average direct debit energy bill under the Energy Price Guarantee. This will enable four million families to save £45 a year on their energy bills from July.

He will also announce his plan to go even further with and ambition to get hundreds of thousands more people into work. Support will focus on disabled people and those with long-term health conditions, parents, the over 50s, and people on Universal Credit. The changes are also expected to encourage benefit claimants to move into work or increase their hours with increased sanctions enforcement and Work Coach support, and childcare costs on Universal Credit to be paid up front.

The Chancellor is also expected to reject the narrative of decline, champion the successes the UK has achieved over the past decade, with a promise to build on the country’s competitive advantages to spread wealth and opportunity everywhere.

UK BUDGET MUST REVERSE TORY COST OF LIVING CRISIS

TOMMY SHEPPARD MP AND DEIDRE BROCK MP: SLASH ENERGY BILLS AND PUT MONEY BACK IN PEOPLE’S POCKETS

The SNP has said “the number one priority for the UK budget must be to put money back into people’s pockets” – warning the Tories can’t continue to hammer household incomes.

Ahead of today’s budget, Tommy Sheppard MP and Deidre Brock MP have urged Jeremy Hunt to deliver a comprehensive package to boost household incomes and economic growth. The MPs for Edinburgh East and Edinburgh North & Leith have challenged the Chancellor to deliver the SNP’s five-point plan:

Saving families £1400 on energy bills – by cutting the Energy Price Guarantee to £2000 and maintaining the £400 Energy Bill Support Scheme to the summer.

Raising public sector pay and benefits by CPI – putting money into the pockets of millions of workers and delivering Barnett consequentials for Scottish spending.

Scrapping Tory plans to raise the pension age to 68 and reinstating the Triple Lock – so no one must struggle in old age.

Re-joining the European Single Market – to boost economic growth and halt the multi-billion pound long-term damage being caused by Brexit.

Investing in green growth – by competing with EU and US subsidies to attract green investment.

In addition to the headroom identified by the IFS, and the billions of pounds saved as a result of the falling wholesale price of gas, the SNP is calling for the Chancellor to scrap non-dom tax status, tax share buy backs, and expand the windfall tax, which would raise billions more to fund cost of living support for ordinary households.

Commenting, Edinburgh East MP, Tommy Sheppard said: “The number one priority for the UK budget must be to put money back into people’s pockets – and reverse this Tory-made cost of living crisis.

“Scotland is a wealthy, energy-rich country but families are being fleeced by Westminster. By refusing to act, the Tories are showing why Scotland needs independence, so we can escape Westminster control, re-join the EU, and build a fair and prosperous economy.

“Families are sick to the back teeth of being ripped off by the Tory government. Instead of hammering household incomes, the Chancellor must save families £1,400 by slashing energy bills and deliver a comprehensive package of support.

“The SNP’s five-point plan would reduce bills, raise incomes and boost economic growth, at a time when many families are struggling to get by. With energy companies making record profits and the wholesale price of gas falling, there is no excuse for failing to act.”

Edinburgh North & Leith MP, Deidre Brock, added: “The SNP Scottish Government is doing everything it can with limited fiscal powers, including delivering the Scottish Child Payment, higher energy bill support, and higher public sector pay.

“The UK government must finally step up to the plate and use its reserved powers to introduce a Real Living Wage and raise public sector pay and benefits by CPI. In doing so, it would raise the incomes of millions of workers and deliver Barnett consequentials which would benefit Edinburgh and Scotland.

“This UK Budget is all about choices. Instead of making families in Edinburgh pay for Westminster failure, the Tories must fund support by scrapping non-dom tax status, expanding the windfall tax and taxing share buy backs, which would raise billions.

“And if we are serious about delivering economic growth and reversing decline, the UK government must re-join the European single market and properly invest in green energy.

“Scotland is suffering the consequences of Westminster control. The Tories trashed the economy with Brexit, austerity cuts and thirteen years of mismanagement. And with the pro-Brexit Labour Party becoming a pound-shop Tory tribute act, it’s clear independence is the only way for Scotland to secure the real change we need.”

Budget predictions – Bank of Scotland

Chris Lawrie, area director for Scotland at Bank of Scotland, said: “Business confidence in Scotland rose in recent months and, after business rates were frozen in a bid to help smaller businesses in the Scottish Budget, firms will be looking to the Chancellor to continue supporting long-term, sustainable growth and encourage higher levels of productivity.

“Growing the economy is key and the Budget is an opportunity to bring further stability and encourage investment in future growth. The Chancellor could show that he can help meet these ambitions by increasing capital allowances and providing the greater certainty and support businesses need to invest in a more high-tech, low-carbon economy.”

CHANCELLOR’S “reset” to clean up the UK’s domestic energy supply and secure long term energy security, while delivering up to 50,000 highly skilled jobs is expected next week

£20 billion will transform carbon capture in Britain, helping create up to 50,000 highly skilled jobs.